![]()

MIRA

INFORM REPORT

|

Report Date : |

27.06.2007 |

IDENTIFICATION DETAILS

|

Name : |

MEDICAPS LIMITED |

|

|

|

|

Registered Office : |

|

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.03.2006 |

|

|

|

|

Date of Incorporation : |

06.08.1983 |

|

|

|

|

Com. Reg. No.: |

10-2231 |

|

|

|

|

CIN No. : |

L24232MP1983PLC002231 |

|

|

|

|

TAN No.: [Tax

Deduction & Collection Account No.] |

BPLM01282B |

|

|

|

|

Legal Form : |

Public Limited Liability Company. Company’s shares are listed on the stock Exchanges. |

|

|

|

|

Line of Business : |

Manufacturing of Capsules to attain Zero – Defect in Production and to fully normalize operations. |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Maximum Credit Limit : |

USD 1000000 |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

Regular |

|

|

|

|

Litigation : |

Clear |

|

|

|

|

Comments : |

Subject is a well – established company having satisfactory track. Trade relations are fair. General financial position is satisfactory. Payments are usually correct and as per commitments. The company can be considered normal for business dealings at usual trade terms and conditions. |

LOCATIONS

|

Registered Office : |

|

|

Tel. No.: |

91-7292-2407445/2407446/253596 |

|

Fax No.: |

91-7292-407387 |

|

E-Mail : |

|

|

Website : |

|

|

|

|

|

Corporate Office : |

401, Chetal Center, 12/2, R. N. T. Marg, |

|

Tel. No.: |

91-731-24046321/2514062 |

|

Fax No.: |

91-731-2582269 |

|

E-Mail : |

DIRECTORS

|

Name : |

Mr. R.C. Mittal |

|

Designation : |

Chairman & Managing Director |

|

|

|

|

Name : |

Mr. Alok k. Garg |

|

Designation : |

Executive Director |

|

|

|

|

Name : |

Mrs. Trapti Gupta |

|

Designation : |

Director |

|

|

|

|

Name : |

Mrs. Kusum Mittal |

|

Designation : |

Director |

|

|

|

|

Name : |

Dr. S.K. Sharma |

|

Designation : |

Director |

|

|

|

|

Name : |

Dr. J.P. Srivastava |

|

Designation : |

Director |

|

|

|

|

Name : |

Dr. Shamsher Singh |

|

Designation : |

Director |

|

|

|

|

Name : |

Dr. Vishwanath B. Malkar |

|

Designation : |

Director |

|

|

|

|

Name : |

Mr. Ganesh Pawar |

|

Designation : |

Company Secretary |

|

|

|

|

Name : |

Dr. Vinay G. Nayak |

|

Designation : |

Director |

|

|

|

|

Name : |

Shri Ashok R. Pitaliya |

|

Designation : |

Manager – Accounts |

|

|

|

KEY EXECUTIVES

|

Name : |

D.K. Jain & Company |

|

Designation : |

Company Secretaries |

|

Address : |

4th floor, |

MAJOR SHAREHOLDERS / SHAREHOLDING PATTERN

|

Names of Shareholders |

No. of Shares |

Percentage of

Holding |

|

v Promoters Holding |

|

|

|

Indian Promoters |

1429800 |

45.864 |

|

Persons Acting in

Concert |

760 |

0.024 |

|

Sub Total |

1430560 |

45.888 |

|

v

Non Promoters

Holding |

|

|

|

Mutual Funds and UTI |

1400 |

0.045 |

|

Banks, Financial

Institutions, Companies

(Central/State Government/ Non-Government. Institutions) |

7300 |

0.234 |

|

Sub Total |

8700 |

0.279 |

|

v

Others |

|

|

|

Private Corporate Bodies |

146644 |

4.704 |

|

Indian Public |

1490458 |

47.810 |

|

NRI/OCBs |

41127 |

1.319 |

|

Sub Total |

1678229 |

53.833 |

|

|

|

|

|

Grand Total |

3117489 |

100.000 |

|

|

|

|

BUSINESS DETAILS

|

Line of Business : |

Manufacturing of Capsules to attain Zero – Defect in Production and to fully normalize operations. |

|

|

|

|

Products : |

Products

Description: Hard Gelatin Capsule Shells I.P. Item Code : 9602 0030 |

|

|

|

PRODUCTION STATUS

|

Particulars |

|

Unit |

Installed

Capacity |

Actual

Production |

|

|

|

|

|

|

|

Hard Gelatin Capsule Shells I.P. |

|

Nos in mins |

32,500 |

31,742 |

GENERAL INFORMATION

|

Customers: |

v

US

Vitamins v

SOL

Pharmaceuticals v

Dr

Reddy's Laboratories v

Lupin Laboratories v

Aristo Pharmaceuticals |

|

|

|

|

Bankers : |

v

IDBI Bank Limited. v

IndusInd Bank Limited. v

State-Bank of v ICICI Bank v HSBC Limited v Citibank N.A. |

|

|

|

|

Banking

Relations : |

Satisfactory |

|

|

|

|

Auditors : |

|

|

Name : |

Rawka Agrawal

& Company Chartered Accountants, |

|

Address : |

403, Arcade

Silver 56, 1, New Palasia, |

|

|

|

|

Associates/Subsidiaries : |

The Medi-Caps Group

Companies include: 1. Medi-Caps

Institute of Technology and Management (MITM) 2. Medi-Caps Finance Limited 3. International

Institute of Foreign Trade and Research

(IIFTR) 4. Medpak India

Limited 5. Trapti

Investments (P) Limited 6. Mittal

Enterprises 7. Akshit Finance (P) Limited |

CAPITAL STRUCTURE

Authorized Capital :

|

No. of Shares |

Type |

Value |

Amount |

|

|

|

|

|

|

40,00,000 |

Equity Shares |

Rs. 10/- Each |

Rs. 40.000 Millions |

|

|

|

|

|

|

|

|

|

|

Issued, Subscribed & Paid-up Capital :

|

No. of Shares |

Type |

Value |

Amount |

|

|

|

|

|

|

36,68,580 |

Equity Shares |

Rs. 10/- Each |

Rs. 36.685 Millions |

|

Subscribed |

|

|

|

|

31,17,489 |

Equity Shares |

Rs. 10/- Each |

Rs. 31.174 Millions |

|

Add: |

Forfeited Shares amount originally Paid Up |

|

Rs. 2.755 Millions |

|

|

Total |

|

Rs. 33.930

Millions |

FINANCIAL DATA

[all figures are

in Rupees Millions]

ABRIDGED BALANCE

SHEET

|

SOURCES OF FUNDS |

31.03.2006 |

31.03.2005 |

31.03.2004 |

|

|

|

SHAREHOLDERS FUNDS |

|

|

|

|

|

|

1] Share Capital |

33.930 |

33.930 |

33.930 |

|

|

|

2] Share Application Money |

0.000 |

0.000 |

0.000 |

|

|

|

3] Reserves & Surplus |

268.132 |

210.638 |

176.408 |

|

|

|

4] (Accumulated Losses) |

0.000 |

0.000 |

0.000 |

|

|

|

NETWORTH |

302.062 |

244.568 |

210.338 |

|

|

|

LOAN FUNDS |

|

|

|

|

|

|

1] Secured Loans |

1.551 |

0.000 |

0.000 |

|

|

|

2] Unsecured Loans |

0.000 |

4.255 |

5.921 |

|

|

|

TOTAL BORROWING |

1.551 |

4.255 |

5.921 |

|

|

|

DEFERRED TAX LIABILITIES |

10.305 |

11.645 |

12.410 |

|

|

|

|

|

|

|

|

|

|

TOTAL |

313.918 |

260.468 |

228.669 |

|

|

|

|

|

|

|

|

|

|

APPLICATION OF FUNDS |

|

|

|

|

|

|

|

|

|

|

|

|

|

FIXED ASSETS [Net Block] |

55.663 |

61.827 |

67.469 |

|

|

|

Capital work-in-progress |

0.000 |

0.000 |

0.006 |

|

|

|

|

|

|

|

|

|

|

INVESTMENT |

196.313 |

122.513 |

109.127 |

|

|

|

DEFERREX TAX ASSETS |

0.000 |

0.000 |

0.000 |

|

|

|

|

|

|

|

|

|

|

CURRENT ASSETS, LOANS & ADVANCES |

|

|

|

|

|

|

|

Inventories |

25.742 |

28.161

|

19.904 |

|

|

|

Sundry Debtors |

43.269 |

37.851

|

36.401 |

|

|

|

Cash & Bank Balances |

8.233 |

15.355

|

5.434 |

|

|

|

Other Current Assets |

0.000 |

0.000

|

0.000 |

|

|

|

Loans & Advances |

29.364 |

33.144

|

39.565 |

|

|

Total

Current Assets |

106.608

|

114.511

|

101.304 |

|

|

|

Less : CURRENT

LIABILITIES & PROVISIONS |

|

|

|

|

|

|

|

Current Liabilities |

26.875 |

22.335

|

29.436 |

|

|

|

Provisions |

18.357 |

17.182

|

21.499 |

|

|

Total

Current Liabilities |

45.232

|

39.517

|

50.935 |

|

|

|

Net Current Assets |

61.376

|

74.994

|

50.369 |

|

|

|

|

|

|

|

|

|

|

MISCELLANEOUS EXPENSES |

0.566 |

1.133 |

1.698 |

|

|

|

|

|

|

|

|

|

|

TOTAL |

313.918 |

260.468 |

228.669 |

|

|

PROFIT & LOSS

ACCOUNT

|

PARTICULARS |

31.03.2006 |

31.03.2005 |

31.03.2004 |

|

Sales Turnover (Including Other income ) |

240.335 |

240.000 |

247.263 |

|

|

|

|

|

|

Profit/(Loss) Before Tax |

75.195 |

51.218 |

55.621 |

|

Provision for Taxation |

11.853 |

11.085 |

14.064 |

|

Profit/(Loss) After Tax |

63.342 |

40.133 |

41.557 |

|

|

|

|

|

|

Export Value |

29.518 |

36.943 |

30.701 |

|

|

|

|

|

|

Import Value |

1.794 |

1.361 |

1.041 |

|

|

|

|

|

|

Expenditures : |

0.000 |

0.000 |

|

|

Cost of Goods Sold |

0.000 |

0.000 |

|

|

Manufacturing Expenses |

37.847 |

43.489 |

|

|

Administrative Expenses |

0.000 |

0.000 |

|

|

Raw Material Consumed |

53.538 |

57.352 |

|

|

Purchases made for re-sale |

0.000 |

0.000 |

|

|

Consumption of stores and spares parts |

0.000 |

0.000 |

|

|

Increase/(Decrease) in Finished Goods |

0.000 |

0.000 |

191.642 |

|

Salaries, Wages, Bonus, etc. |

25.154 |

25.122 |

|

|

Excise Duty |

19.441 |

24.579 |

|

|

Payment to Auditors |

0.000 |

0.000 |

|

|

Interest |

0.007 |

0.000 |

|

|

Right Issue Expenses |

0.566 |

0.566 |

|

|

Expenses of Previous Year |

0.139 |

0.603 |

|

|

Depreciation & Amortization |

7.699 |

7.869 |

|

|

Other Expenditure |

20.745 |

29.199 |

|

|

Total Expenditure |

165.136 |

188.779 |

191.642 |

SUMMERIZED RESULTS

|

PARTICULARS |

|

|

2007 (Full Year) |

|

Sales Turnover |

|

|

184.100 |

|

Other Income |

|

|

60.500 |

|

Total Income |

|

|

244.600 |

|

Total Expenditure |

|

|

144.600 |

|

Operating Profit |

|

|

100.000 |

|

Interest |

|

|

0.400 |

|

Gross Profit |

|

|

99.600 |

|

Depreciation |

|

|

8.100 |

|

Tax |

|

|

10.700 |

|

Reported PAT |

|

|

80.800 |

|

Dividend (%) |

|

|

0.000 |

KEY RATIOS

|

PARTICULARS |

31.03.2006 |

31.03.2005 |

31.03.2004 |

|

Debt Equity Ratio |

0.01 |

0.02 |

0.03 |

|

Long Term Debt Equity

Ratio |

0.01 |

0.02 |

0.03 |

|

Current Ratio |

2.07 |

1.88 |

1.68 |

|

TURNOVER RATIOS |

|

|

|

|

Fixed Assets |

1.24 |

1.32 |

1.51 |

|

Inventory |

7.22 |

8.54 |

11.56 |

|

Debtors |

4.79 |

5.53 |

6.27 |

|

Interest Cover

Ratio |

0.00 |

0.00 |

0.00 |

|

Operating Profit

Margin (%) |

22.97 |

23.62 |

27.71 |

|

Profit Before

Interest and Tax Margin (%) |

19.01 |

19.78 |

24.39 |

|

Cash Profit

Margin (%) |

20.25 |

19.43 |

21.54 |

|

Adjusted Net

Profit Margin (%) |

16.29 |

15.59 |

18.21 |

|

Return on Capital

Employed (%) |

13.56 |

17.80 |

28.65 |

|

Return on Net

Worth (%) |

11.71 |

14.26 |

21.92 |

STOCK PRICES

|

Face Value |

Rs. 10.00 |

|

High |

Rs. 69.50 |

|

Low |

Rs. 67.30 |

LOCAL AGENCY FURTHER INFORMATION

Fixed Assets

Ø

Free

Ø

Building

Ø

Plant & Machinery

Ø

Furniture & Fixture

Ø

Vehicles

Ø

Computers

History:

Medi-caps was incorporated

by S L Mittal in Aug.'83 as a private limited company and was converted into a public

limited company in Mar.'86. Pharmaceutical companies procure empty hard gelatin

capsules from Medi-caps for dosage medicines meant for oral administration. The

company is the second-largest manufacturer of empty hard gelatin capsules in

It takes several years for a company manufacturing capsules to attain

zero-defect in production and to fully normalize operations. Medi-caps can

claim to have achieved this. In Apr.'95, the company offered 0.611Millions

rights shares at a premium of Rs 116 to part-finance the Rs 91.9- Millions expansion of its manufacturing facilities

(from 2000 mln pa to 3440 mln pa) by installing four high-speed automatic

capsule-making machines.

The company's manufacturing unit is located in Pithampur, Madhya Pradesh..

At present, it has 40 clients. The other group company of Medi-caps is

Medi-caps Finance which is engaged in finance related activities. In 1993, R C

Mittal received the Glory of India International award.

In 1995-96, the company enhanced the capacity of empty hard gelatin

capsules by 250.0 Millions the company received ISO 9002 Certification during

1998-99. It developed six sizes of the Hard Gelatin Capsules in 2002-03. The

company is closely working on commissioning of 13th Machine with 100% atomization.

During 2002-03 the company established the export market in countries like

REVIEW OF

OPERATIONS:

During the under review Company could achieve a total income of

Rs.246.017 millions in comparison of previous year Rs.228.250 millions. Decline

in manufacturing turnover is purely due to various Government polices. For

example introduction of VAT, Excise on MRP for finished products etc. Due to

these issues major consumers of our product have cut down their production due

to which there was low demand.

The financial health of the country has shown significant growth

in all the sectors, and the company could able to earn Rs.46.821 millions

(previous year Rs.20.499 millions) this income includes dividend of Rs.10.087

millions and profit on sale of mutual funds Rs.32.192 millions. Due to strong

financial planning your company has maximized its value of investments and also

foresee the positive trends in the coming year. The overall profit for the year

is recorded to Rs.63.343 millions in comparison of previous year Rs.40.078

millions The Company has grown substantially the profitability despite of fall

in turnover.

MANAGEMENT DISCUSSION AND ANALYSIS REPORT:

Industry structure and developments:

The pharmaceuticals industry is a knowledge driven industry and is

heavily dependent on Research and Development of new products and growth.

However, basic research is a time consuming and expensive process and is thus

dominated by the huge local and global multinationals. Indian companies have

entered into the area and the results have been encouraging.

In the global pharmaceuticals market, western markets are growing largely

due to the introduction of the new molecules at the highest prices. A

well-established reimbursement and the insurance system imply that the per

capita drug expenditure is abnormally high in the western countries.

The Indian pharmaceuticals industry is highly fragmented, but has

grown rapidly due to the friendly patent regime and the low cost manufacturing

structure. The country production of the bulk drugs and the formulations grew

at CAGR of 18% over the past ten years

SWOT

ANALYSIS FOR THE COMPANY:

·

Strengths:

·

Strong Research & Development.* Integrated supply

chain.* Ability to deliver cost saving.* High quality of manpower resources at

a lower cost.* Centralized manufacturing activities at Pithampur Plant.* Zero

Debt Company.* Strong financial planning.

·

Weaknesses:

·

Scarcity of Technical Expertise.* Controlling of process

parameters is very critical.* Dependency on formulation Companies.* Frequent

fluctuation in market demand.* Very sensitive process of manufacturing.

·

Opportunities:

* In export there is a very good demand of gelatin

capsules and

* Due to improved capital market, there are good possibility

to invest the surplus funds in good securities and mutual funds.

·

Threats:

·

·

Aggressive price competition from local and multinational

player

·

Fast technology change in the manufacturing line of the

Company.

·

Frequent change in Govt. policy for pharmaceutical

industries.

·

Developed countries are very rigid in procuring capsules

from out of countries.

·

Competitions from the new entrants in the SEZ area, which

are enjoying duty exemption benefits.

Outlook:

While we cannot predict a further performance, we believe

considerable opportunities will exist for sustained and profitable growth, not

only in the developing countries but also in the developed western countries.

The Company is in continuous process to launch new variety of capsules and

variants to meet out the demands in the coming year and also to expand its

marketing reach in other countries for growth in the export as well as domestic

turnover. The company with its continued focus on exports stands to gain a lot

from the emerging scenario:

Marketing and Export:

In domestic market your Company had added many multinational

companies in its client lists with improved quality of products as well as

services. Due to that, company is forced to reduce the export basket.

ISO: 9001:2000 CERTIFICATION:

As you are aware that your Company is ISO: 9001:2000

complied companies which is the latest version of ISO series and this will give

further strength to the quality as well as international recognition and will

contribute to the export business of the company as it has done in the past

years.

As per website Details:

About Us:

Medi-Caps Limited flagship company of Medi-Caps Group, is one of the

largest manufacturer of empty hard gelatin capsules in terms of manufacturing

capacity as well as market capitalization in India, incorporated in 1986,

Medi-Caps Limited entered the highly competitive market with a team of

dedicated professionals, duly supported by competent individuals in every

aspect of operation.

At Medi-Caps Limited a philosophy of growth has been consistently upheld

with good business practices. Clear focus, excellent infrastructure, a powerful

quality policy and a well defined management information system have helped the

company to achieve consistent growth.

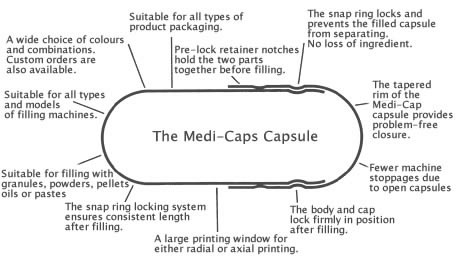

Their product range comprises of six sizes ranging from 00,0el, 0, 1el,

1,2,3,4 in more than 1000 shades, the same is increasing as rapidly as Pharma

Industry itself.

Today they offer printing features that are best in the industry. Medi-Caps

Limited has pioneered many advanced features in product development such as

“Pearlz Capsules” (Metallic Colored) as well as Python Printing & Li-Fill

Caps.

Medi-Caps Limited continuously strives to offer its customers excellent

product, technical advice, and a through professional service that makes their

product tailor made for their customers both in

Their professional goals and corporate personality have blended so well that

today Medi-Caps Limited name has become synonymous with the best in the

Industry.

Company

They implicitly believe that the corporate responsibility extends beyond

the ambit of a company's facilities and offices.

And that the true corporate citizenship must include common cause with

the society.

With this belief, Medi-Caps encourage funds and develop numerous

education and human capital initiatives.

These initiatives are now recognized in

Their mission is to offer product as well as services of the highest

professional standards in order to maintain their role as the customer's vendor

of first choice.”

Professional

Excellence

At Medi-Caps Ltd.

a philosophy of growth has been consistently upheld with good business

practices. Clear focus, excellent infrastructure, a powerful quality policy and

a well defined management information system have helped the company to achieve

constant success.

A team of dedicated

professionals is ably supported by competent colleagues in every area ranging

from manufacturing, through quality assurance, administration and management,

to sale.

Regular

interaction with vendors, dealer, customers, employees and financial

institutions, has helped to built a clear path to success.

PRODUCT INFORMATION

They manufacture Empty Hard Gelatin Capsules in sizes

00,0el,0,1el,1,2,3,4 elongated , fortified with more than thousand shades which

is growing as rapidly as pharma industries.

QUALITY

EXCELLENCE

A firm believer in the philosophy of Total Quality

Control Management, the company has evolved the

culture of systematic production that eliminates errors

in every stage of production.

Capsule production being a continuous process, representative samples

are regularly tested for physical defect, length, dome, double, wall thickness,

moisture content, colour shades, weight variation and other relevant

parameters.

The group's activities span manufacturing of Hard Gelatin Capsule

Shells, Education, Industrial Packaging & related products, Finance, Real

Estate and are a renowned name in central

The Flagship Company

Medi-Caps Limited has emerged as

CMT REPORT (Corruption, Money Laundering & Terrorism]

The Public Notice information has been collected from various sources

including but not limited to: The Courts,

1] INFORMATION ON

DESIGNATED PARTY

No records exist designating subject or any of its beneficial owners,

controlling shareholders or senior officers as terrorist or terrorist

organization or whom notice had been received that all financial transactions

involving their assets have been blocked or convicted, found guilty or against

whom a judgement or order had been entered in a proceedings for violating

money-laundering, anti-corruption or bribery or international economic or

anti-terrorism sanction laws or whose assets were seized, blocked, frozen or

ordered forfeited for violation of money laundering or international

anti-terrorism laws.

2] Court Declaration :

No records exist to suggest that subject is

or was the subject of any formal or informal allegations, prosecutions or other

official proceeding for making any prohibited payments or other improper

payments to government officials for engaging in prohibited transactions or

with designated parties.

3] Asset Declaration :

No records exist to suggest that the property or assets of the subject

are derived from criminal conduct or a prohibited transaction.

4] Record on Financial

Crime :

Charges or conviction registered

against subject: None

5] Records on Violation of

Anti-Corruption Laws :

Charges or

investigation registered against subject: None

6] Records on Int’l

Anti-Money Laundering Laws/Standards :

Charges or

investigation registered against subject: None

7] Criminal Records

No

available information exist that suggest that subject or any of its principals

have been formally charged or convicted by a competent governmental authority

for any financial crime or under any formal investigation by a competent

government authority for any violation of anti-corruption laws or international

anti-money laundering laws or standard.

8] Affiliation with

Government :

No record

exists to suggest that any director or indirect owners, controlling shareholders,

director, officer or employee of the company is a government official or a

family member or close business associate of a Government official.

9] Compensation Package :

Our market

survey revealed that the amount of compensation sought by the subject is fair

and reasonable and comparable to compensation paid to others for similar

services.

10] Press Report :

No press reports / filings exists on

the subject.

CORPORATE GOVERNANCE

MIRA INFORM as part of its Due Diligence do provide comments on Corporate

Governance to identify management and governance. These factors often have been

predictive and in some cases have created vulnerabilities to credit

deterioration.

Our Governance Assessment focuses principally on the interactions

between a company’s management, its Board of Directors, Shareholders and other

financial stakeholders.

CONTRAVENTION

Subject is not known to have contravened any existing local laws,

regulations or policies that prohibit, restrict or otherwise affect the terms

and conditions that could be included in the agreement with the subject.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.41.01 |

|

|

1 |

Rs.81.74 |

|

Euro |

1 |

Rs.55.04 |

SCORE & RATING EXPLANATIONS

|

SCORE FACTORS |

RANGE |

POINTS |

|

HISTORY |

1~10 |

6 |

|

PAID-UP CAPITAL |

1~10 |

6 |

|

OPERATING SCALE |

1~10 |

6 |

|

FINANCIAL CONDITION |

|

|

|

--BUSINESS SCALE |

1~10 |

6 |

|

--PROFITABILIRY |

1~10 |

6 |

|

--LIQUIDITY |

1~10 |

6 |

|

--LEVERAGE |

1~10 |

6 |

|

--RESERVES |

1~10 |

6 |

|

--CREDIT LINES |

1~10 |

6 |

|

--MARGINS |

-5~5 |

- |

|

DEMERIT POINTS |

|

|

|

--BANK CHARGES |

YES/NO |

YES |

|

--LITIGATION |

YES/NO |

NO |

|

--OTHER ADVERSE INFORMATION |

YES/NO |

NO |

|

MERIT POINTS |

|

|

|

--SOLE DISTRIBUTORSHIP |

YES/NO |

NO |

|

--EXPORT ACTIVITIES |

YES/NO |

YES |

|

--AFFILIATION |

YES/NO |

YES |

|

--LISTED |

YES/NO |

YES |

|

--OTHER MERIT FACTORS |

YES/NO |

YES |

|

TOTAL |

|

54 |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit consideration.

Capability to overcome financial difficulties seems comparatively below

average/normal. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|