![]()

MIRA

INFORM REPORT

|

Report Date : |

01.07.2008 |

IDENTIFICATION

DETAILS

|

Name : |

EUROPERFIL SA |

|

|

|

|

Registered Office : |

Avenida De

La Gran Via, 179, Cp 08908, L Hospitalet De

Llobregat Barcelona |

|

|

|

|

Country : |

Spain |

|

|

|

|

Financials (as on) : |

31.12.2006 |

|

|

|

|

Date of Incorporation : |

|

|

|

|

|

Legal Form : |

Sociedad Anonima |

|

|

|

|

Line of Business : |

First

Processing of Iron and Steel and Prod of Non-Esc Ferro-Alloys |

RATING &

COMMENTS

|

MIRA’s Rating : |

A |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

Maximum Credit Limit : |

1.500.000,00 € |

|

|

|

|

Status : |

Good |

|

|

|

|

Payment Behaviour : |

Regular |

|

|

|

|

Litigation : |

Clear |

FINANCIAL

REPORT

EUROPERFIL SA

TAX NUMBER: A58346305

EXECUTIVE SUMMARY

Identification

Current Business Name: EUROPERFIL SA

Commercial Name: EUROPERFIL, S.A.

Other names: YES

Current Address: AVENIDA DE

LA GRAN VIA, 179, CP 08908, L HOSPITALET DE

LLOBREGAT BARCELONA

Branches: 1

Telephone number: 932316333 Fax: 932616338

URL: www.europerfil.es Corporate e-mail: administracio@europerfil.es

Commercial Risk

Credit Appraisal:

1.500.000,00 €

Legal Actions: NO

Financial Information

Latest Balance sheet sales (2006): 54.600.132,78 € (Registro Mercantil)

Result: 2.087.898,22 €

Total Assets:

44.256.799,82 €

Social Capital: 2.404.000,00 €

Employees: 89

Commercial Information

Constitution Date: 31/03/1987

Business activity: First

processing of iron & steel & prod of non-esc ferro-alloys

NACE Code: 2730

International Operations: Importa y

exporta

Corporate Structure

Presidente:

Credit Appraisal

Maximum Credit (from 0 a 6,000,000 €):

1.500.000,00 €

Rating Evolution

Financial Situation

Fiscal year2006

|

Treasury |

Excelente |

|

Indebtedness |

Medio |

|

Profitability |

Media |

|

Balance |

Excelente |

Performance

|

Legal Actions |

Nulas o irrelevantes |

|

Business

Trajectory |

Excelente |

INCIDENTS

Summary

LEGAL ACTIONS: No legal

incidences registered

CLAIM FILED AGAINST THE ADMINISTRATION: No administrative

claims registered

AFFECTED BY:

3 Company / Companies in Insolvency Proceedings.

FINANCIAL ELEMENTS AND SECTORIAL

COMPARATIVE

FINANCIAL ELEMENTS

Figures given in €

|

|

2004 (12) |

2005 (12) |

2006 (12) |

% ASSETS |

|

|

|

|

|

|

BALANCE SHEET ANALYSIS |

|

|

|

|

|

|

|

|

|

|

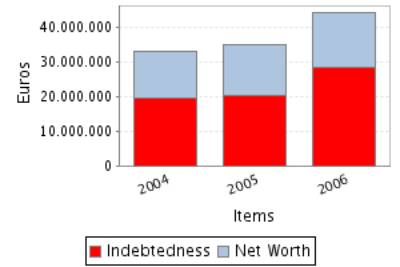

OWN FUNDS |

13.724.526,82 |

14.643.501,21 |

15.644.977,95 |

35,35 |

|

|

|

|

|

|

DEBT |

19.539.507,33 |

20.520.111,33 |

28.611.821,87 |

64,65 |

|

|

|

|

|

|

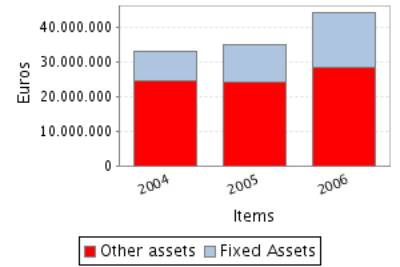

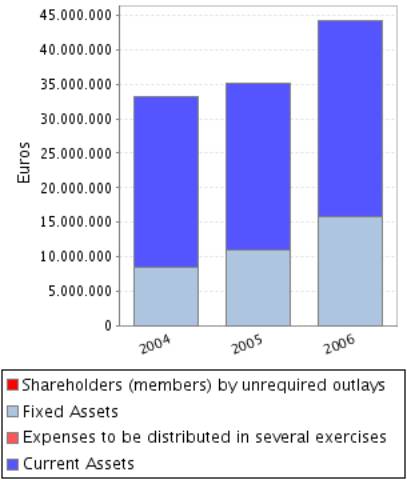

FIXED ASSETS |

8.551.314,22 |

11.064.372,23 |

15.765.429,05 |

35,62 |

|

|

|

|

|

|

TOTAL ASSETS |

33.264.034,15 |

35.163.612,54 |

44.256.799,82 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2004 (12) |

2005 (12) |

2006 (12) |

% SALES |

|

|

|

|

|

|

PROFIT AND LOSS ACCOUNT ANALYSIS |

|

|

|

|

|

|

|

|

|

|

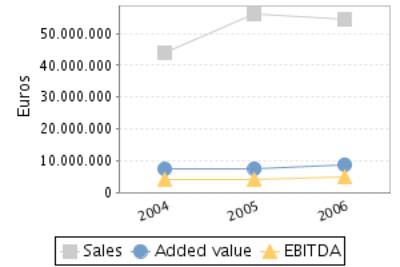

SALES |

43.998.339,40 |

56.024.570,23 |

54.600.132,78 |

|

|

|

|

|

|

|

ADDED VALUE |

7.339.145,18 |

7.502.240,39 |

8.776.661,69 |

16,07 |

|

|

|

|

|

|

EBITDA |

4.204.525,25 |

4.128.659,62 |

4.912.113,33 |

9,00 |

|

|

|

|

|

|

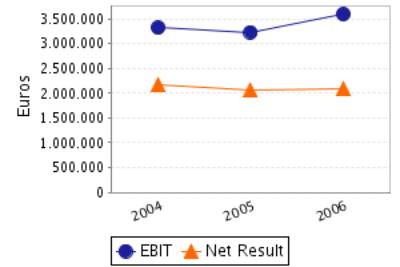

EBIT |

3.324.681,10 |

3.235.200,36 |

3.596.230,89 |

6,59 |

|

|

|

|

|

|

NET RESULT |

2.168.207,35 |

2.059.666,39 |

2.087.898,22 |

3,82 |

|

|

|

|

|

Balance Sheets Items Analysis

Balance Sheet

Comments

Total assets of the company grew 5,71% between 2004 and 2005.

This growth is a consequence of the fixed assets increase of 29,39%.

This growth has been financed, on a wider scale, with a Shareholders’

equity increase of 6,70% and in a smaller proportion with an debt increase of

5,02%.

Total assets of the company grew 25,86% between 2005 and 2006.

This growth is a consequence of the fixed assets increase of 42,49%.

This growth has been mainly financed with a debt increase of 39,43%.

Nevertheless the net worth increased 6,84%.

Profit and Loss Account Analysis

Profit and Loss

Account Comments

The company’s sales figure grew 27,33% between 2004 and 2005.

The company’s EBIT decreased in 2,69% between 2004 and 2005.

This evolution implies a reduction in the company’s operating

profitability.

The result of these variations is a decrease of the company’s Economic

Profitability of 7,95% in the analysed period, being this profitability of

9,20% in the year 2005.

The company’s Net Result decreased in 5,01% between 2004 and 2005.

This evolution, compared to the EBIT’s performance, implies that the

financial and extraordinary activities have had a negative effect in the

company’s Financial Profitability.

The result of these variations is a reduction of the company’s

profitability of 10,97% in the analysed period, being equal to 14,07% in the

year 2005.

The company’s sales figure decreased in 2,54% between 2005 and 2006.

The company’s EBIT grew 11,16% between 2005 and 2006.

This evolution implies an increase in the company’s operating

profitability.

The result of these variations is a decrease of the company’s Economic

Profitability of 11,68% in the analysed period, being this profitability of

8,13% in the year 2006.

The company’s Net Result grew 1,37% between 2005 and 2006.

This evolution, compared to the EBIT’s performance, implies that the

financial and extraordinary activities have had a negative effect in the

company’s Financial Profitability.

The result of these variations is a reduction of the company’s

profitability of 5,12% in the analysed period, being equal to 13,35% in the

year 2006.

ANNUAL FINANCIAL REPORT

ADDITIONAL DATA

Source: annual financial report 2006

Results Distribution

Figures given in €

|

DISTRIBUTION BASE |

DISTRIBUTION TO |

||

|

Profit and Loss |

2.087.898,22 |

Retained earnings |

0,00 |

|

Carry Over |

0,00 |

Voluntary Reserve |

1.043.949,10 |

|

Voluntary reserves |

0,00 |

Prior years losses |

0,00 |

|

Reserves |

0,00 |

Carry Over |

0,00 |

|

Other concepts |

0,00 |

Other funds |

0,00 |

|

Total of Amounts to be distributed |

2.087.898,22 |

Dividends |

1.043.949,12 |

|

|

|

Other Applications |

0,00 |

Auditing

Auditors’ opinion: FAVORABLE

Auditor: SANTACANA AUDITORES S.A.

COMPARATIVE SECTOR ANALYSIS

Values table

Figures expressed in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

BALANCE SHEET

ANALYSIS: % on the total assets |

|

|

|

|

|

|

|

|

|

|

OWN FUNDS |

35,35 |

47,93 |

-12,58 |

-26,25 |

|

|

|

|

|

|

DEBT |

64,65 |

52,07 |

12,58 |

24,17 |

|

|

|

|

|

|

FIXED ASSETS |

35,62 |

44,97 |

-9,35 |

-20,79 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

PROFIT AND LOSS

ACCOUNT ANALYSIS: % on the total operating income |

|

|

|

|

|

|

|

|

|

|

SALES |

98,35 |

97,88 |

0,48 |

0,49 |

|

|

|

|

|

|

ADDED VALUE |

15,81 |

17,53 |

-1,72 |

-9,79 |

|

|

|

|

|

|

EBIT |

6,48 |

5,14 |

1,34 |

25,96 |

|

|

|

|

|

|

NET RESULT |

3,76 |

2,82 |

0,94 |

33,18 |

|

|

|

|

|

Sector Composition

Compared sector (NACE): 273

Number of companies: 14

Size (Sales Figure) : > 40.000.000,00

Euros

Comments on the

sectorial comparative

Compared to its sector the assets of the companies show an inferior

proportion of fixed assets. Specifically the difference with the sector average

is -9,35% , which means a relative difference of -20,79% .

In liabilities composition the company appeals on a wider scale to self

financing, being the proportion of net worth of 12,58% inferior, which means a

relative difference of 26,25% 12,58% more than the sector, which means a

difference of 24,17% .

The proportion that the sales mean to the company’s total ordinary

income is 98,35%, 0,48% higher than in the sector, which means a relative

difference of 0,49% .

The company’s EBIT was positive and was 6,48% with regard to the total

ordinary income, 1,34% higher than in the sector, which means a relative

difference of 25,96% .

The company’s capacity to generate operating income is higher than the

one of the sector as its ratio EBIT/Sales is higher (ES Company versus ES

Sector).

The company’s net result was positive and equal to 3,76% with regard to

the total ordinary income, 0,94% higher than in the sector, which means a

relative difference of 33,18% .

The financial and extraordinary results and the tax impact have had a

less negative impact on the Net result in the company than in the sector; as a

consequence, the company shows a better Net Result/EBIT ratio (REBEmpresa vs.

REBSector).

ADDRESSES

Current Legal Seat Address:

AVENIDA DE LA GRAN VIA, 179

08908 L HOSPITALET DE LLOBREGAT BARCELONA

Previous Seat Address:

CALLE NICARAGUA, 46

08029

BARCELONA

Characteristics

of the current address

Type of premises: oficina

Property: en alquiler

Local Situation: secundaria

Branches

|

STREET |

POSTAL CODE |

TOWN |

PROVINCE |

|

POLIGONO DE CERVERA AV VALL D ARAN SN |

25200 |

CERVERA |

Lérida |

1 branches registered

CORPORATE STRUCTURE

ADMINISTRATIVE LINKS

Main Board members,

Directors and Auditor ![]()

|

POSITION |

SURNAMES AND

NAME |

APPOINTMENT DATE |

|

|

PRESIDENTE |

SANS CASTELLS JOAN |

20/09/2007 |

|

|

CONSEJERO |

MILLERON PIERRE FRANCOIS |

02/09/2002 |

|

|

CONSEJERO |

GUY AMEDRO |

15/07/2004 |

|

|

CONSEJERO |

GUY RENE AMEDRO |

20/09/2007 |

|

|

CONSEJERO |

PHILIPPE BONNAVE |

20/09/2007 |

|

|

CONSEJERO |

STEPHANE CLAUDE FERON |

20/09/2007 |

|

|

SECRETARIO |

VAZQUEZ DE SOLA GALINDO FRANCISCO |

22/01/2004 |

|

|

AUDITOR |

APPOINTMENT DATE |

||

|

MOORE STEPHENS & SANTACANA AUDITORES Y CONSULTORES |

01/02/2008 |

||

Functional Managers

|

POSITION |

SURNAMES AND

NAME |

|

Director general |

MARTORELL ENRIC |

|

Director financiero |

MARCO ANTONIO |

|

Director de rrhh |

ROJANO SANCHEZ FERNANDO |

|

Director comercial |

GARGANTILLA ALFREDO |

FINANCIAL LINKS

|

|

BUSINESS NAME |

CIF / COUNTRY |

% |

SOURCE |

DATA INF. |

|

|

ACIEROID SA. |

ESPAÑA |

50,00 |

F.PROPIAS |

05/05/2008 |

|

|

ARCELOR CONSTRUCTION FRANCE |

FRANCIA |

50,00 |

F.PROPIAS |

05/05/2008 |

You can obtain business information of a foreign company at the

pageD&B International

CREDIT INFORMATION

Constitution Date: 31/03/1987

Business activity

Activity: First processing

of iron & steel & prod of non-esc ferro-alloys

NACE Code: 2730

NACE Activity: Other first processing of iron and steel and

production of non-ECSC ferro-alloys

Business: COMERCIALIZACION DE PERFILES DE ACERO Y DEMAS

ARTICULOS METALICOS PARA LA CONSTRUCCION Y, EN GENERAL, TODA CLASE DE ARTICULOS

METALICOS PARA LA CONSTRUCCION.

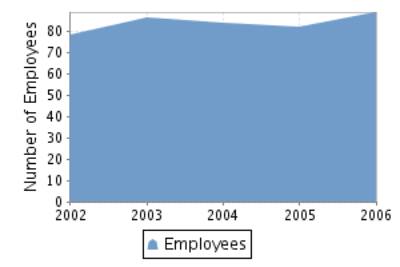

Employees

Number of total employees: 89 (2008)

Number of fixed employees: 100,00%

Number of temporary employees: 0,00%

Employees evolution

COMMERCIAL OPERATIONS

SUPPLIERS

|

BUSINESS NAME |

INTERNATIONAL |

|

KONTI STEEL |

SI |

|

ACIEROID SA

UNIPERSONAL |

NO |

|

BOUYGUES

CONSTRUCCION |

NO |

|

UGINE IBERICA |

NO |

|

TAC METAL

FORMING |

NO |

|

GONVARRI

INDUSTRIAL |

NO |

|

ACERALIA

TRANSFORMADOS SA |

NO |

|

ACME CATALUNYA

SA |

NO |

|

ARCELOR

CONSTRUCCION ESPAÑA SL |

NO |

|

ARCELOR

DISTRIBUCION MEDITERRANEO SL |

NO |

21 proveedores

SALES

Collection (estimated):

Exports to: Portugal

National Distribution: 100%

CLIENTS

|

BUSINESS NAME |

INTERNATIONAL |

|

ACERALIA

CONSTRUCCION OBRAS SL |

NO |

|

BCE SA |

SI |

|

ACERALIA

TRANSFORMADOS SA |

NO |

|

HAIRONVILLE

PORTUGAL |

NO |

|

ACME CATALUNYA

SA |

NO |

|

TAC METAL

FORMING |

NO |

|

ACIEROID SA

UNIPERSONAL |

NO |

|

DV CONST UTE

SABADELL |

NO |

|

OMNITRADE

ESPAGNE |

NO |

|

POLYTUIL SFH |

NO |

18 clientes

Banks

|

ENTITY |

BRANCH |

ADDRESS |

TOWN OR CITY |

PROVINCE |

|

BANCO BILBAO VIZCAYA ARGENTARIA, S.A. |

1000 |

PL. DE CATALUÑA, 5 |

080190001 |

Barcelona |

|

BNP PARIBAS ESPAÑA, S.A. |

0405 |

AVENIDA DIAGONAL, 682 4. PLANTA |

080190001 |

Barcelona |

|

BANCO DE SABADELL, S.A. |

0014 |

AV BARCELONA 000021 |

081840001 |

Barcelona |

|

CAIXA D’ESTALVIS DE TERRASSA |

0039 |

AVDA. DE BARCELONA, 86 |

081840001 |

Barcelona |

|

BANCO SANTANDER, S.A. |

|

|

L HOSPITALET DE LLOBREGAT |

|

5 bank entities registered

Brands, Signs and Commercial

Names

Brand name: NILHO (Valid)

Type: MIXTA Date: 07/03/2007

Brand name: ARTIC (Valid)

Type: MIXTA Date: 07/03/2007

Brand name: EUROBASE (Valid)

Type: DENOMINATIVA Date: 09/07/1996

Brand name: EUROBAC (Valid)

Type: DENOMINATIVA Date: 09/07/1996

Brand name: EUROMODUL (Valid)

Type: DENOMINATIVA Date: 09/07/1996

LEGAL STRUCTURE

Constitution Data

Register Date: 31/03/1987

Current Legal Form: SOCIEDAD ANONIMA

Current Capital:

2.404.000,00 €

Legal Aspects

Obligation to fill in Financial

Statements: YES

Chamber census: YES (2006)

Listed on a Stock Exchange: NO

B.O.R.M.E.(Official Companies

Registry Gazette)

Registered Proceedings

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Nombramientos |

01/02/2008 |

53578 |

Barcelona |

|

Nombramientos |

20/09/2007 |

479558 |

Barcelona |

|

Nombramientos |

20/09/2007 |

478435 |

Barcelona |

|

Nombramientos |

20/09/2007 |

478434 |

Barcelona |

Other Proceedings published

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Depósito de cuentas (2006) Individual |

10/12/2007 |

1148099 |

Barcelona |

Press articles

07/03/2007 SEGRE (INFORMACIÓN FINANCIERA)

EUROPERFIL, EMPRESA LIDER EN EL SECTOR DE CUBIERTAS METALICAS PARA LA

CONSTRUCCION, PREVE TRIPLICAR SU FACTURACION EN LOS PROXIMOS CINCO AÑOS,

PASANDO DE LOS 60 MM. DE EUROS DE 2006 A LOS 180 MM. EN 2011. LA SDAD.

DUPLICARA SU INVERSION DE 7 MM. DE EUROS HECHA EN 2006 A LOS 14 MM. EN 2008

DESTINADOS A LA AMPLIACION HASTA 50.000 METROS CUADRADOS DE LA PLANTA DE

CERVERA. LOS BENEFICIOS DEL PASADO AÑO ASCENDIERON A 3 MM. DE EUROS. EUROPERFIL

CREARA EN MEDIO AÑO 20 NUEVOS PUESTOS DE TRABAJO, HASTA SUMAR 80 TRABAJADORES

EN CERVERA.

06/01/2007 SEGRE (INFORMACIÓN FINANCIERA)

LA EMPRESA ACIEROID, ESPECIALIZADA EN SOLUCIONES CONSTRUCTIVAS, HA

INVERTIDO 8 MM. DE EUROS EN LA AMPLIACION DE SUS FABRICAS DE EUROPERFIL DE

CERVERA (LLEIDA) Y SESEÑA (TOLEDO), LO QUE LE PERMITIRA INCREMENTAR LA

PRODUCCION EN UN 12% Y SU PLANTILLA CON 25 EMPLEADOS. EN CONCRETO, ACIEROID HA

DESTINADO 7 MM. DE EUROS A SU FABRICA DE CERVERA, PLANTA QUE GANARA 5.400

TONELADAS DE CAPACIDAD PRODUCTIVA, MIENTRAS QUE LA TOLEDANA DOBLARA SU

PRODUCCION. LA FABRICA DE LLEIDA PASARA DE LOS 7.000 METROS CUADRADOS INICIALES

A 29.000 Y SU PLANTILLA CRECERA DE 60 A 85 TRABAJADORES. POR SU PARTE, LA

PLANTA DE SESEÑA PASARA DE 3.000 A 5.000 METROS CUADRADOS.

FINANCIAL INFORMATION

The information on the last account contained in this report is

extracted from the Mercantile Register file of the legal address of the Company

and dated 08/11/2007.

BALANCE SHEET

Assets

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

A) ACCIONISTAS (SOCIOS) POR DESEMBOLSOS NO

EXIGIDOS |

|

|

|

|

B) INMOVILIZADO |

8.551.314,22 |

11.064.372,23 |

15.765.429,05 |

|

I. Gastos de establecimiento |

|

|

|

|

II. Inmovilizaciones inmateriales |

|

|

407.290,00 |

|

Gastos de investigación y desarrollo |

|

|

407.290,00 |

|

Concesiones, patentes, licencias, marcas y similares |

|

|

|

|

Fondo de comercio |

|

|

|

|

Derechos de traspaso |

|

|

|

|

Aplicaciones informáticas |

|

|

|

|

Derechos s/bienes en régimen de arrendamiento financiero |

|

|

|

|

Anticipos |

|

|

|

|

Provisiones |

|

|

|

|

Amortizaciones |

|

|

|

|

III. Inmovilizaciones materiales |

8.516.573,74 |

11.029.631,75 |

15.347.439,05 |

|

Terrenos y construcciones |

3.880.793,70 |

6.802.301,08 |

6.802.301,08 |

|

Instalaciones técnicas y maquinaria |

11.214.294,41 |

11.690.852,08 |

11.897.358,04 |

|

Otras instalaciones, utillaje y mobiliario |

1.614.816,84 |

1.722.140,69 |

1.782.927,19 |

|

Anticipos e inmovilizaciones materiales en curso |

60.600,00 |

99.550,00 |

5.195.011,63 |

|

Otro inmovilizado |

529.798,24 |

591.963,49 |

661.134,02 |

|

Provisiones |

|

|

|

|

Amortizaciones |

-8.783.729,45 |

-9.877.175,59 |

-10.991.292,91 |

|

IV. Inmovilizaciones financieras |

34.740,48 |

34.740,48 |

10.700,00 |

|

Participaciones en empresas del grupo |

|

|

|

|

Créditos a empresas del grupo |

|

|

|

|

Participaciones en empresas asociadas |

|

|

|

|

Créditos a empresas asociadas |

|

|

|

|

Cartera de valores a largo plazo |

|

|

|

|

Otros créditos |

|

|

|

|

Depósitos y fianzas constituidos a largo plazo |

34.740,48 |

34.740,48 |

10.700,00 |

|

Provisiones |

|

|

|

|

Administraciones Públicas a largo plazo |

|

|

|

|

V. Acciones propias |

|

|

|

|

VI. Deudores por operaciones de tráfico a largo

plazo |

|

|

|

|

C) GASTOS A DISTRIBUIR EN VARIOS EJERCICIOS |

|

|

|

|

D) ACTIVO CIRCULANTE |

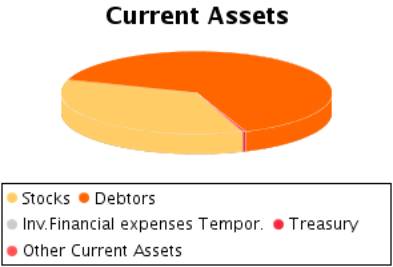

24.712.719,93 |

24.099.240,31 |

28.491.370,77 |

|

I. Accionistas por desembolsos exigidos |

|

|

|

|

II. Existencias |

9.418.267,00 |

7.553.515,00 |

10.137.759,00 |

|

Comerciales |

|

|

|

|

Materias primas y otros aprovisionamientos |

8.542.288,00 |

6.467.972,00 |

8.534.680,00 |

|

Productos en curso y semiterminados |

|

|

|

|

Productos terminados |

875.979,00 |

1.085.543,00 |

1.603.079,00 |

|

Subproductos residuos y materiales recuperados |

|

|

|

|

Anticipos |

|

|

|

|

Provisiones |

|

|

|

|

III. Deudores |

15.039.905,31 |

16.323.384,79 |

18.254.656,70 |

|

Clientes por ventas y prestaciones de servicios |

11.091.313,16 |

13.182.209,88 |

14.197.073,33 |

|

Empresas del grupo, deudores |

4.453.517,43 |

3.219.520,44 |

4.342.495,91 |

|

Empresas asociadas, deudores |

|

|

|

|

Deudores varios |

|

|

|

|

Personal |

42.599,63 |

42.531,26 |

41.036,12 |

|

Administraciones Públicas |

15.635,63 |

489.813,74 |

269.344,41 |

|

Provisiones |

-563.160,54 |

-610.690,53 |

-595.293,07 |

|

IV. Inversiones financieras temporales |

|

|

|

|

Participaciones en empresas del grupo |

|

|

|

|

Créditos a empresas del grupo |

|

|

|

|

Participaciones en empresas asociadas |

|

|

|

|

Créditos a empresas asociadas |

|

|

|

|

Cartera de valores a corto plazo |

|

|

|

|

Otros créditos |

|

|

|

|

Depósitos y fianzas constituidos a corto plazo |

|

|

|

|

Provisiones |

|

|

|

|

V. Acciones propias a corto plazo |

|

|

|

|

VI. Tesorería |

239.114,37 |

222.340,52 |

98.955,07 |

|

VII. Ajustes por periodificación |

15.433,25 |

|

|

|

TOTAL ACTIVO (A + B + C + D) |

33.264.034,15 |

35.163.612,54 |

44.256.799,82 |

Assets composition

Liabilities

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

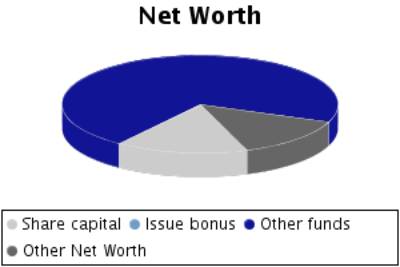

A) FONDOS PROPIOS |

13.387.686,29 |

14.363.249,00 |

15.421.314,02 |

|

I. Capital suscrito |

2.404.000,00 |

2.404.000,00 |

2.404.000,00 |

|

II. Prima de emisión |

|

|

|

|

III. Reserva de revalorización |

|

|

|

|

IV. Reservas |

8.815.478,94 |

9.899.582,61 |

10.929.415,80 |

|

Reserva legal |

480.809,68 |

480.809,68 |

480.809,68 |

|

Reservas para acciones propias |

|

|

|

|

Reservas para acciones de la sociedad dominante |

|

|

|

|

Reservas estatutarias |

|

|

|

|

Otras reservas |

8.334.620,84 |

9.418.724,51 |

10.448.557,70 |

|

Diferencias por ajuste del capital a euros |

48,42 |

48,42 |

48,42 |

|

V. Resultados de ejercicios anteriores |

|

|

|

|

Remanente |

|

|

|

|

Resultados negativos de ejercicios anteriores |

|

|

|

|

Aportaciones de

socios para compensación de pérdidas |

|

|

|

|

VI. Pérdidas y

Ganancias (beneficio o pérdida) |

2.168.207,35 |

2.059.666,39 |

2.087.898,22 |

|

VII. Dividendo a

cuenta entregado en el ejercicio |

|

|

|

|

VIII. Acciones

propias para reducción de capital |

|

|

|

|

B) INGRESOS A

DISTRIBUIR EN VARIOS EJERCICIOS |

336.840,53 |

280.252,21 |

223.663,93 |

|

Subvenciones de

capital |

336.840,53 |

280.252,21 |

223.663,93 |

|

Diferencias

positivas de cambio |

|

|

|

|

Otros ingresos a

distribuir en varios ejercicios |

|

|

|

|

Ingresos

fiscales a distribuir en varios ejercicios |

|

|

|

|

C) PROVISIONES

PARA RIESGOS Y GASTOS |

288.290,88 |

|

|

|

Provisiones para

pensiones y obligaciones similares |

|

|

|

|

Provisiones para impuestos |

|

|

|

|

Otras provisiones |

288.290,88 |

|

|

|

Fondo de reversión |

|

|

|

|

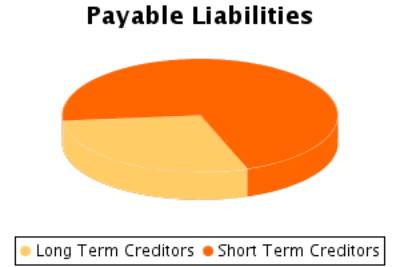

D) ACREEDORES A LARGO PLAZO |

|

|

8.300.929,12 |

|

I. Emisiones de obligaciones y otros valores

negociables |

|

|

|

|

Obligaciones no convertibles |

|

|

|

|

Obligaciones convertibles |

|

|

|

|

Otras deudas

representadas en valores negociables |

|

|

|

|

II. Deudas con

entidades de crédito |

|

|

8.300.929,12 |

|

Deudas a largo

plazo con entidades de crédito |

|

|

8.300.929,12 |

|

Acreedores por

arrendamiento financiero a largo plazo |

|

|

|

|

III. Deudas con

empresas del grupo y asociadas |

|

|

|

|

Deudas con

empresas del grupo |

|

|

|

|

Deudas con

empresas asociadas |

|

|

|

|

IV. Otros

acreedores |

|

|

|

|

Deudas

representadas por efectos a pagar |

|

|

|

|

Otras deudas |

|

|

|

|

Fianzas y

depósitos recibidos a largo plazo |

|

|

|

|

Administraciones

Públicas a largo plazo |

|

|

|

|

V. Desembolsos

pendientes sobre acciones no exigidos |

|

|

|

|

De empresas del

grupo |

|

|

|

|

De empresas

asociadas |

|

|

|

|

De otras

empresas |

|

|

|

|

VI. Acreedores por operaciones de tráfico a largo

plazo |

|

|

|

|

E) ACREEDORES A CORTO PLAZO |

19.251.216,45 |

20.520.111,33 |

20.310.892,75 |

|

I. Emisiones de obligaciones y otros valores

negociables |

|

|

|

|

Obligaciones no convertibles |

|

|

|

|

Obligaciones convertibles |

|

|

|

|

Otras deudas representadas en valores negociables |

|

|

|

|

Intereses de obligaciones y otros valores |

|

|

|

|

II. Deudas con entidades de crédito |

2.574.676,19 |

2.257.276,66 |

5.634.906,40 |

|

Préstamos y otras deudas |

2.564.550,75 |

2.235.244,17 |

5.564.841,06 |

|

Deudas por intereses |

10.125,44 |

22.032,49 |

70.065,34 |

|

Acreedores por arrendamiento financiero a corto plazo |

|

|

|

|

III. Deudas con empresas del grupo y asociadas a

corto plazo |

4.481.483,71 |

3.944.395,68 |

349.035,59 |

|

Deudas con empresas del grupo |

4.481.483,71 |

3.944.395,68 |

349.035,59 |

|

Deudas con empresas asociadas |

|

|

|

|

IV. Acreedores comerciales |

10.497.867,96 |

9.641.564,50 |

10.521.194,78 |

|

Anticipos recibidos por pedidos |

130.348,98 |

69.705,36 |

390.528,42 |

|

Deudas por compras o prestaciones de servicios |

10.367.518,98 |

9.571.859,14 |

10.130.666,36 |

|

Deudas representadas por efectos a pagar |

|

|

|

|

V. Otras deudas no comerciales |

1.420.932,87 |

4.457.935,82 |

3.517.021,13 |

|

Administraciones Públicas |

859.254,05 |

705.106,91 |

979.540,69 |

|

Deudas representadas por efectos a pagar |

|

|

|

|

Otras deudas |

306.443,78 |

3.507.521,15 |

2.383.832,67 |

|

Remuneraciones pendientes de pago |

255.235,04 |

245.307,76 |

153.647,77 |

|

Fianzas y depósitos recibidos a corto plazo |

|

|

|

|

VI. Provisiones para operaciones de tráfico |

|

|

|

|

VII. Ajustes por periodificación |

276.255,72 |

218.938,67 |

288.734,85 |

|

F) PROVISIONES PARA RIESGOS Y GASTOS A CORTO

PLAZO |

|

|

|

|

TOTAL PASIVO (A + B + C + D + E + F) |

33.264.034,15 |

35.163.612,54 |

44.256.799,82 |

Liabilities

Composition

PROFIT AND LOSS ACCOUNT

Itams of the Profit

and Loss Account

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

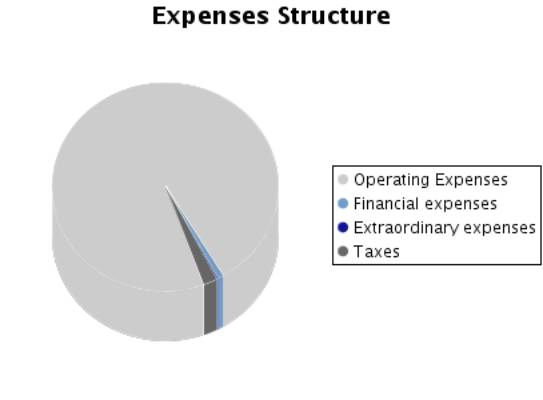

A) GASTOS (A.1 a A.16) |

42.191.676,56 |

54.480.522,97 |

54.031.021,17 |

|

A.1. Reducción de existencias de productos

terminados y en curso de fabricación |

7.720,00 |

|

|

|

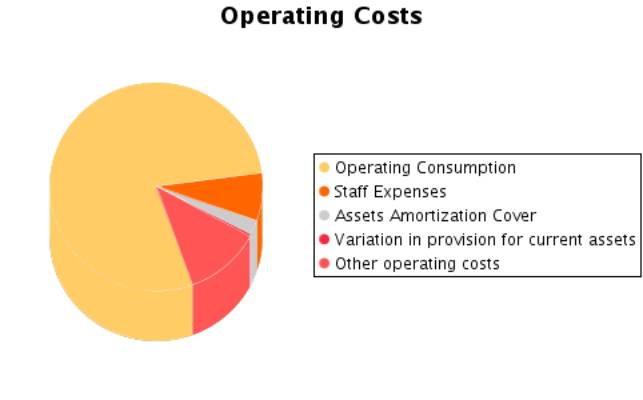

A.2. Aprovisionamientos |

31.868.987,55 |

43.355.934,46 |

41.253.869,32 |

|

Consumo de mercaderías |

|

|

|

|

Consumo de materias primas y otras materias consumibles |

30.920.977,46 |

42.292.396,74 |

40.061.037,17 |

|

Otros gastos externos |

948.010,09 |

1.063.537,72 |

1.192.832,15 |

|

A.3. Gastos de personal |

3.134.619,93 |

3.373.580,77 |

3.864.548,36 |

|

Sueldos, salarios y asimilados |

2.368.187,29 |

2.481.630,94 |

2.817.745,27 |

|

Cargas sociales |

766.432,64 |

891.949,83 |

1.046.803,09 |

|

A.4. Dotaciones para amortizaciones de

inmovilizado |

1.074.952,02 |

1.093.446,14 |

1.153.795,47 |

|

A.5. Variación de las provisiones de tráfico |

-195.107,87 |

-199.986,88 |

162.086,97 |

|

Variación de provisiones de existencias |

|

|

|

|

Variación de provisiones y pérdidas de créditos incobrables |

84.005,71 |

88.304,00 |

162.086,97 |

|

Variación de otras provisiones de tráfico |

-279.113,58 |

-288.290,88 |

|

|

A.6. Otros gastos de explotación |

5.051.788,56 |

5.602.938,02 |

6.000.457,42 |

|

Servicios exteriores |

5.036.784,54 |

5.543.662,50 |

5.955.518,15 |

|

Tributos |

15.004,02 |

59.275,52 |

44.939,27 |

|

Otros gastos de gestión corriente |

|

|

|

|

Dotación al fondo de reversión |

|

|

|

|

A.I. BENEFICIOS DE EXPLOTACION

(B.1+B.2+B.3+B.4-A.1-A.2-A.3-A.4-A.5-A.6) |

3.324.681,10 |

3.235.200,36 |

3.596.230,89 |

|

A.7. Gastos financieros y gastos asimilados |

220.878,91 |

250.470,60 |

441.970,46 |

|

Por deudas con empresas del grupo |

|

|

|

|

Por deudas con empresas asociadas |

|

|

|

|

Por otras deudas Por deudas con terceros y gastos asimilados |

220.878,91 |

250.470,60 |

441.970,46 |

|

Pérdidas de inversiones financieras |

|

|

|

|

A.8. Variación de las provisiones de inversiones

financieras |

|

|

|

|

A.9. Diferencias negativas de cambio |

|

|

|

|

A.II. RESULTADOS FINANCIEROS POSITIVOS

(B.5+B.6+B.7+B.8-A.7-A.8-A.9) |

|

|

|

|

A.III. BENEFICIOS DE LAS ACTIVIDADES ORDINARIAS

(A.I+A.II-B.I-B.II) |

3.133.456,49 |

3.007.217,93 |

3.180.603,11 |

|

A.10. Variación de las provisiones de

inmovilizado inmaterial, material y cartera de control |

|

|

|

|

A.11. Pérdidas procedentes del inmovilizado

inmaterial, material y cartera de control |

|

|

64.349,35 |

|

A.12. Pérdidas por operaciones con acciones y

obligaciones propias |

|

|

|

|

A.13. Gastos extraordinarios |

|

61.049,25 |

|

|

A.14. Gastos y pérdidas de otros ejercicios |

|

|

|

|

A.IV. RESULTADOS EXTRAORDINARIOS POSITIVOS

(B.9+B.10+B.11+B.12+B.13-A.10-A.11-A.12-A.13-A.14) |

62.588,32 |

|

|

|

A.V. BENEFICIOS ANTES DE IMPUESTOS

(A.II+A.IV-B.III-B.IV.) |

3.196.044,81 |

3.002.757,00 |

3.177.842,04 |

|

A.15. Impuesto sobre Sociedades |

1.027.837,46 |

943.090,61 |

1.089.943,82 |

|

A.16. Otros impuestos |

|

|

|

|

A.VI. RESULTADO DEL EJERCICIO (BENEFICIOS)

(A.V-A.15-A.16) |

2.168.207,35 |

2.059.666,39 |

2.087.898,22 |

|

B) INGRESOS (B.1 a B.13) |

44.359.883,91 |

56.540.189,36 |

56.118.919,39 |

|

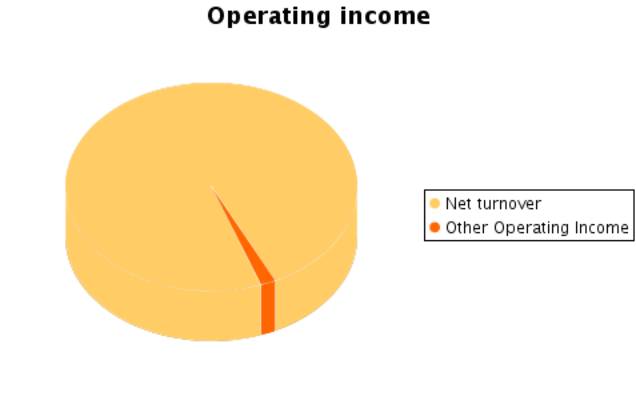

B.1. Importe neto de la cifra de negocios |

43.998.339,40 |

56.024.570,23 |

54.600.132,78 |

|

Ventas |

43.998.339,40 |

56.024.570,23 |

54.600.132,78 |

|

Prestaciones de servicios |

|

|

|

|

Devoluciones y “rappels” sobre ventas |

|

|

|

|

B.2. Aumento de existencias de productos

terminados y en curso de fabricación |

|

209.564,00 |

517.536,00 |

|

B.3. Trabajos efectuados por la empresa para el

inmovilizado |

|

|

240.761,49 |

|

B.4. Otros ingresos de explotación |

269.301,89 |

226.978,64 |

672.558,16 |

|

Ingresos accesorios y otros de gestión corriente |

269.301,89 |

226.978,64 |

672.558,16 |

|

Subvenciones |

|

|

|

|

Exceso de provisiones de riesgos y gastos |

|

|

|

|

B.I. PÉRDIDAS DE EXPLOTACIÓN

(A.1+A.2+A.3+A.4+A.5+A.6-B.1-B.2-B.3-B.4) |

|

|

|

|

B.5. Ingresos de participaciones en capital |

|

|

|

|

En empresas del grupo |

|

|

|

|

En empresas asociadas |

|

|

|

|

En empresas fuera del grupo |

|

|

|

|

B.6. Ingresos de otros valores negociables y de

créditos del activo inmovilizado |

|

|

|

|

De empresas del grupo |

|

|

|

|

De empresas asociadas |

|

|

|

|

De empresas fuera del grupo |

|

|

|

|

B.7. Otros intereses e ingresos asimilados |

29.654,30 |

22.488,17 |

26.342,68 |

|

De empresas del grupo |

|

|

|

|

De empresas asociadas |

|

|

|

|

Otros intereses |

29.654,30 |

22.488,17 |

26.342,68 |

|

Beneficios en inversiones financieras |

|

|

|

|

B.8. Diferencias positivas de cambio |

|

|

|

|

B.II. RESULTADOS FINANCIEROS NEGATIVOS

(A.7+A.8+A.9-B.5-B.6-B.7-B.8) |

191.224,61 |

227.982,43 |

415.627,78 |

|

B.III. PÉRDIDAS DE LAS ACTIVIDADES ORDINARIAS

(B.I+B.II-A.I-A.II) |

|

|

|

|

B.9. Beneficios en enajenación de inmovilizado

inmaterial, material y cartera de control |

6.000,00 |

|

|

|

B.10. Beneficios por operaciones con acciones y

obligaciones propias |

|

|

|

|

B.11. Subvenciones de capital transferidas al

resultado del ejercicio |

56.588,32 |

56.588,32 |

61.588,28 |

|

B.12. Ingresos extraordinarios |

|

|

|

|

B.13. Ingresos y beneficios de otros ejercicios |

|

|

|

|

B.IV. RESULTADOS EXTRAORDINARIOS NEGATIVOS

(A.10+A.11+A.12+A.13+A.14-B.9-B.10-B.11-B.12-B.13) |

|

4.460,93 |

2.761,07 |

|

B.V. PÉRDIDAS ANTES DE IMPUESTOS

(B.III+B.IV-A.III-A.IV) |

|

|

|

|

B.VI. RESULTADO DEL EJERCICIO (PERDIDAS)

(B.V+A.15+A.16) |

|

|

|

Composition of the

Profit and Loss Account

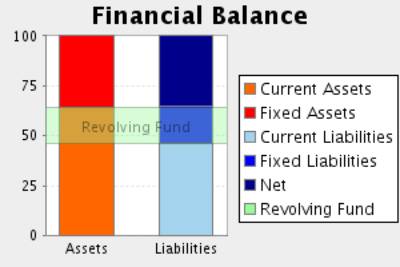

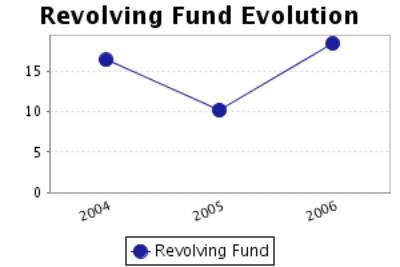

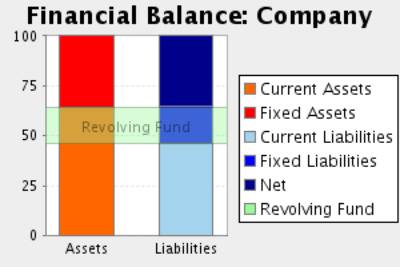

FINANCIAL BALANCE

Here the Main Capital Amounts of the company and the Revolving Fund

Evolution are analysed.

Financial Balance

Table

Figures given in €

|

|

31/12/2004 (12) |

% |

31/12/2005 (12) |

% |

31/12/2006 (12) |

% |

|

A) ACCIONISTAS (SOCIOS) POR DESEMBOLSOS NO EXIGIDOS |

|

|

|

|

|

|

|

B) INMOVILIZADO |

8.551.314,22 |

25,71 |

11.064.372,23 |

31,47 |

15.765.429,05 |

35,62 |

|

C) GASTOS A DISTRIBUIR EN VARIOS EJERCICIOS |

|

|

|

|

|

|

|

D) ACTIVO CIRCULANTE |

24.712.719,93 |

74,29 |

24.099.240,31 |

68,53 |

28.491.370,77 |

64,38 |

|

TOTAL ACTIVO (A

+ B + C + D) |

33.264.034,15 |

|

35.163.612,54 |

|

44.256.799,82 |

|

|

|

||||||

|

A) FONDOS

PROPIOS |

13.387.686,29 |

40,25 |

14.363.249,00 |

40,85 |

15.421.314,02 |

34,85 |

|

B) INGRESOS A

DISTRIBUIR EN VARIOS EJERCICIOS |

336.840,53 |

1,01 |

280.252,21 |

0,80 |

223.663,93 |

0,51 |

|

C) PROVISIONES

PARA RIESGOS Y GASTOS |

288.290,88 |

0,87 |

|

|

|

|

|

D) ACREEDORES A

LARGO PLAZO |

|

|

|

|

8.300.929,12 |

18,76 |

|

E) ACREEDORES A

CORTO PLAZO |

19.251.216,45 |

57,87 |

20.520.111,33 |

58,36 |

20.310.892,75 |

45,89 |

|

F) PROVISIONES

PARA RIESGOS Y GASTOS A CORTO PLAZO |

|

|

|

|

|

|

|

TOTAL PASIVO (A + B + C + D + E + F) |

33.264.034,15 |

|

35.163.612,54 |

|

44.256.799,82 |

|

Financial Balance

Composition

Comments on Financial

Balance

In the 2004, the assets of the company were formed in 25,71% of Fixed

Assets and in 74,29% of Current Assets.This assets were financed in 41,26% with

own capitals, and in 0,87% with long term debt and in 57,87% with current

liabilities.

The result of this financial structure is a positive turnover fund of

5.461.503,48 Euros, which is equivalent to 16,42% proportion of the

company’s total assets.

In the 2005, the assets of the company were formed in 31,47% of Fixed

Assets and in 68,53% of Current Assets.This assets were financed in 41,64% with

own capitals and in 58,36% with current liabilities.

The result of this financial structure is a positive turnover fund of

3.579.128,98 Euros, which is equivalent to 10,18% proportion of the

company’s total assets.

This measure has diminished with respect to the previous exercise in

34,47% having also diminished its proportion with respect to the total assets

of the company.

In the 2006, the assets of the company were formed in 35,62% of Fixed

Assets and in 64,38% of Current Assets.This assets were financed in 35,35% with

own capitals, and in 18,76% with long term debt and in 45,89% with current

liabilities.

The result of this financial structure is a positive turnover fund of

8.180.478,02 Euros, which is equivalent to 18,48% proportion of the

company’s total assets.

This measure has increased with respect to the previous exercise in

128,56% having also increased its proportion with respect to the total assets

of the company.

RATIOS

Main Ratios

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

STRUCTURAL RATIOS |

|

|

|

|

Fondo maniobra |

5.461.503,48 |

3.579.128,98 |

8.180.478,02 |

|

Necesidad fondo maniobra |

7.797.065,30 |

5.614.065,12 |

13.716.429,35 |

|

Endeudamiento (%) |

58,74 |

58,36 |

64,65 |

|

Fondos ajenos sobre fondos propios |

1,42 |

1,40 |

1,83 |

|

GENERAL ACTIVITY RATIO |

|

|

|

|

Crecimiento de la cifra de negocio (%) |

4,77 |

27,33 |

-2,54 |

|

Crecimiento valor añadido (%) |

-0,88 |

2,22 |

16,99 |

|

Cash flow |

3.048.051,50 |

2.953.125,65 |

3.403.780,66 |

|

Productividad de la mano de obra |

2,34 |

2,22 |

2,27 |

|

Rotación de activos |

1,32 |

1,59 |

1,23 |

|

Punto muerto |

32.389.941,56 |

42.365.051,07 |

42.003.431,23 |

|

Margen de seguridad del punto muerto (%) |

26,83 |

24,69 |

24,34 |

|

ACTIVITY RATIOS |

|

|

|

|

Periodo medio de pago |

119 |

80 |

93 |

|

Periodo medio de cobro |

123 |

105 |

120 |

|

Periodo de rotación de inventario |

77 |

49 |

67 |

|

SOLVENCY RATIOS |

|

|

|

|

Capacidad devolución |

0,16 |

0,14 |

0,12 |

|

Garantía de activo |

1,70 |

1,71 |

1,55 |

|

Proporción de deudas a corto plazo (%) |

98,52 |

100,00 |

70,99 |

|

Cobertura de intereses |

13,38 |

10,64 |

6,33 |

|

LIQUIDITY RATIOS |

|

|

|

|

Ratio corriente |

1,28 |

1,17 |

1,40 |

|

Liquidez inmediata |

0,01 |

0,01 |

0,00 |

|

Tesorería |

-2.335.561,82 |

-2.034.936,14 |

-5.535.951,33 |

|

Ventas sobre activo circulante |

641 |

837 |

690 |

Results Analysis

Ratios

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

Rentabilidad económica (%) |

10,00 |

9,20 |

8,13 |

|

Rentabilidad de explotación (%) |

7,56 |

5,78 |

6,59 |

|

Apalancamiento financiero |

2,28 |

2,23 |

2,50 |

|

Rentabilidad financiera (%) |

15,80 |

14,06 |

13,34 |

|

Rentabilidad general (%) |

4,93 |

3,68 |

3,82 |

Comments on the

Results Analysis Ratios

The economic profitability in the year2005 achieved a 9,20% positive

level, due to a 5,78% economic margin and to an assets turnover of1,59%.

The economic profitability in the year has reduced from 10,00% up to

9,20% of2005, even if it remains positive. Assets turnover increase whose index

has passed from 1,32 to 1,59, could not compensate operating profitability

reduction from7,56% to the current level of 5,78%.

Financial profitability on 2005 achieved a 14,06%.

The company’s financial structure has instigated its economic

profitability with an indebtedness level of 2,23.

The general profitability on 2005 achieved a 3,68%.

The economic profitability in the year2006 achieved a 8,13% positive

level, due to a 6,59% economic margin and to an assets turnover of1,23%.

The economic profitability in the year has reduced from 9,20% up to

8,13% of2006, even if it remains positive. The decrease in assets turnover from

1,59% to the current level of 1,23has provoked this drop, which has not been

compensated by the parallel increase of the economic margin from 6,59% to

5,78%.

Financial profitability on 2006 achieved a 13,34%.

The company’s financial structure has instigated its economic

profitability with an indebtedness level of 2,50.

The general profitability on 2006 achieved a 3,82%.

SECTORIAL ANÁLYSIS

Large Capital Amounts

and Financial Balance

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

A) ACCIONISTAS (SOCIOS) POR DESEMBOLSOS NO EXIGIDOS |

|

0,00 |

|

|

|

|

|

|

|

|

B) INMOVILIZADO |

35,62 |

44,97 |

-9,35 |

-20,79 |

|

|

|

|

|

|

C) GASTOS A DISTRIBUIR EN VARIOS EJERCICIOS |

|

1,15 |

|

|

|

|

|

|

|

|

D) ACTIVO CIRCULANTE |

64,38 |

53,88 |

10,50 |

19,48 |

|

|

|

|

|

|

TOTAL ACTIVO (A + B + C + D) |

100 |

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

A) FONDOS PROPIOS |

34,85 |

47,60 |

-12,75 |

-26,78 |

|

|

|

|

|

|

B) INGRESOS A

DISTRIBUIR EN VARIOS EJERCICIOS |

0,51 |

0,34 |

0,17 |

51,79 |

|

|

|

|

|

|

C) PROVISIONES

PARA RIESGOS Y GASTOS |

|

4,64 |

|

|

|

|

|

|

|

|

D) ACREEDORES A

LARGO PLAZO |

18,76 |

12,61 |

6,15 |

48,77 |

|

|

|

|

|

|

E) ACREEDORES A

CORTO PLAZO |

45,89 |

34,81 |

11,08 |

31,82 |

|

|

|

|

|

|

F) PROVISIONES

PARA RIESGOS Y GASTOS A CORTO PLAZO |

|

0,00 |

|

|

|

|

|

|

|

|

TOTAL PASIVO (A + B + C + D + E + F) |

100 |

100 |

|

|

|

|

|

|

|

Financial Balance

Composition

Comments to the

Sectorial Analysis

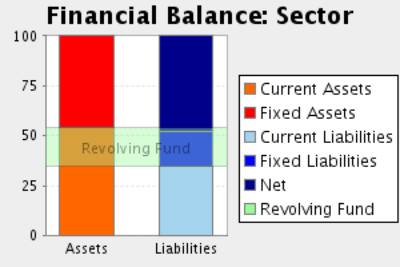

In the 2006, the assets of the company were formed in 35,62% of fixed

assets and in 64,38Current Assets % In the sector, the proportion of fixed

assets was of 46,12%, 22,76% superior, and the proportion of current assets was

of 53,88%, 19,48% inferior.

The assets were financed in the company in 35,35% with own capitals , in

18,76% with fixed liabilities and in 45,89% with current liabilities In the

sector, the self financing represented 47,93%, 26,25% superior. On the other

hand the long term debts represented in the sector an average of 17,26%

financing, with a relative difference of 8,72% in favour of the companyAnd,

short term liabilities represented in the sector an average of 34,81%

financing, with a relative difference of 31,82% in favour of the company

The result of this company’s financial structure is a turnover fund that

represents 18,48% of the total assets; in the sector, this same proportion is

19,07%, therefore, we can say that the company’s turnover fund is 3,09% smaller

than the sector one.

Analytical Account of

Results

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

Importe neto de la cifra de negocios |

98,35 |

97,88 |

0,47 |

0,48 |

|

Otros ingresos de explotación |

1,65 |

2,12 |

-0,47 |

-22,24 |

|

Valor de la Producción |

100,00 |

100,00 |

0,00 |

0,00 |

|

Consumos explotación |

73,38 |

70,14 |

3,24 |

4,62 |

|

Otros gastos explotación |

10,81 |

12,34 |

-1,53 |

-12,37 |

|

Valor Añadido |

15,81 |

17,53 |

-1,72 |

-9,79 |

|

Gastos de Personal |

6,96 |

9,05 |

-2,09 |

-23,07 |

|

Resultado Económico Bruto |

8,85 |

8,48 |

0,37 |

4,36 |

|

Dotaciones para amortizaciones de inmovilizado |

2,08 |

3,35 |

-1,27 |

-37,85 |

|

Variación de las provisiones de tráfico y pérdidas de crédito

incobrables |

0,29 |

-0,01 |

0,30 |

-2.736,36 |

|

Resultado Económico Neto |

6,48 |

5,14 |

1,34 |

26,00 |

|

Ingresos financieros |

0,05 |

1,34 |

-1,29 |

-96,28 |

|

Gastos financieros |

0,80 |

1,00 |

-0,19 |

-19,60 |

|

Variación de las provisiones de inv. financieras |

|

0,03 |

|

|

|

Resultado Actividades Ordinarias |

5,73 |

5,47 |

0,26 |

4,83 |

|

Ingresos extraordinarios |

0,11 |

0,38 |

-0,27 |

-71,20 |

|

Gastos extraordinarios |

0,12 |

1,22 |

-1,10 |

-90,13 |

|

Variación de las provisiones de inmovilizado inmaterial, material y

cartera de control |

|

0,06 |

|

|

|

Resultado Antes Impuestos |

5,72 |

4,57 |

1,15 |

25,22 |

|

Impuesto sobre sociedades |

1,96 |

1,74 |

0,22 |

12,39 |

|

Resultado Neto |

3,76 |

2,82 |

0,94 |

33,14 |

|

Dotaciones para amortizaciones de inmovilizado |

2,08 |

3,35 |

-1,27 |

-37,85 |

|

Variación de provisiones |

0,29 |

0,08 |

0,21 |

262,50 |

|

Autofinanciación Neta |

6,13 |

6,25 |

-0,12 |

-1,94 |

Main Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

STRUCTURAL RATIOS |

|

|

|

|

|

Fondo maniobra |

8.180.478,02 |

6.108,83 |

12.492,43 |

24.104,98 |

|

Necesidad fondo maniobra |

13.716.429,35 |

-17.618,96 |

1.535,44 |

11.982,12 |

|

Endeudamiento (%) |

64,65 |

33,71 |

59,20 |

68,65 |

|

Fondos ajenos sobre fondos propios |

1,83 |

0,51 |

1,45 |

2,19 |

|

GENERAL ACTIVITY RATIO |

|

|

|

|

|

Crecimiento de la cifra de negocio (%) |

-2,54 |

-14,54 |

0,97 |

8,53 |

|

Crecimiento valor añadido (%) |

16,99 |

-49,08 |

-30,44 |

-0,34 |

|

Cash flow |

3.403.780,66 |

2.049,18 |

5.725,49 |

10.268,28 |

|

Productividad de la mano de obra |

2,27 |

1,43 |

2,09 |

3,44 |

|

Rotación de activos |

1,23 |

0,91 |

1,68 |

2,03 |

|

Punto muerto |

42.003.431,23 |

40.921.583,19 |

80.970.663,09 |

165.781.342,66 |

|

Margen de seguridad del punto muerto (%) |

24,34 |

3,02 |

20,45 |

36,34 |

|

ACTIVITY RATIOS |

|

|

|

|

|

Periodo medio de pago |

93 |

37 |

70 |

96 |

|

Periodo medio de cobro |

120 |

81 |

93 |

107 |

|

Periodo de rotación de inventario |

67 |

34 |

50 |

70 |

|

SOLVENCY RATIOS |

|

|

|

|

|

Capacidad devolución |

0,12 |

0,05 |

0,13 |

0,30 |

|

Garantía de activo |

1,55 |

1,45 |

1,66 |

2,97 |

|

Proporción de deudas a corto plazo (%) |

70,99 |

65,50 |

87,86 |

98,56 |

|

Cobertura de intereses |

6,33 |

2,49 |

7,51 |

53,88 |

|

LIQUIDITY RATIOS |

|

|

|

|

|

Ratio corriente |

1,40 |

1,17 |

1,75 |

2,43 |

|

Liquidez inmediata |

0,00 |

0,01 |

0,10 |

0,69 |

|

Tesorería |

-5.535.951,33 |

-7.698,93 |

95,64 |

9.497,90 |

|

Ventas sobre activo circulante |

690 |

571 |

843 |

993 |

Results Analysis

Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

Rentabilidad económica (%) |

8,13 |

1,37 |

6,43 |

14,18 |

|

Rentabilidad de explotación (%) |

6,59 |

0,83 |

4,92 |

9,78 |

|

Apalancamiento financiero |

2,50 |

1,44 |

1,76 |

2,89 |

|

Rentabilidad financiera (%) |

13,34 |

0,46 |

10,93 |

20,49 |

|

Rentabilidad general (%) |

3,82 |

0,20 |

3,15 |

7,52 |

NOTES

ABOUT YOUR REQUEST:

The data of your request are correct.

In spite of investigations using every source available (public and

private), no additional details than those contained in this report

are available. .

FOREIGN EXCHANGE

RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.43.30 |

|

UK Pound |

1 |

Rs.86.13 |

|

Euro |

1 |

Rs.68.72 |

RATING

EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit

consideration. Capability to overcome financial difficulties seems

comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)