![]()

MIRA INFORM REPORT

|

Report Date : |

23.07.2008 |

IDENTIFICATION

DETAILS

|

Name : |

LEVANTINA Y ASOCIADOS DE MINERALES SOCIEDAD ANONIMA. |

|

|

|

|

Registered Office : |

Carretera Autovia 330, S/N - Apartado Correos 8, Cp 03660, Novelda Alicante |

|

|

|

|

Country : |

Spain |

|

|

|

|

Financials (as on) : |

31.12.2006 |

|

|

|

|

Date of Incorporation : |

|

|

|

|

|

Legal Form : |

Joint Stock Company |

|

|

|

|

Line of Business : |

RATING &

COMMENTS

|

MIRA’s Rating : |

A |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

Maximum Credit Limit : |

3.591.648,34 € |

|

|

|

|

Status : |

Good |

|

|

|

|

Payment Behaviour : |

Regular |

|

|

|

|

Litigation : |

Clear |

Name

LEVANTINA Y ASOCIADOS DE MINERALES SOCIEDAD ANONIMA.

TAX NUMBER: A84433515

EXECUTIVE SUMMARY

Identification

Current Business

Name: LEVANTINA Y ASOCIADOS DE MINERALES SOCIEDAD ANONIMA.

Other names: YES

Current

Address: CARRETERA AUTOVIA

330, S/N - APARTADO CORREOS 8, CP 03660, NOVELDA ALICANTE

Branches: 1

Telephone

number: 965606861 Fax: 965606892

URL: www.levantina.com

Corporate e-mail: info@levantina.com

Commercial Risk

Credit Appraisal: 3.591.648,34 €

RAI: NO

Legal

Actions: NO

Financial Information

Latest sales known (2007): 309.089.610,00 € (Estimated)

Latest Balance sheet sales (2006): 300.087.000,00 € (MERCANTILE REGISTER)

Result: -3.101.000 €

Total Assets: 616.664.000 €

Social Capital: 10.676.651,80 €

Employees: 2.500

Commercial Information

Constitution Date: 16/08/2005

Business activity: Natural stone

industries

NACE Code: 2670

International Operations: Imports and

Exports

Corporate Structure

President:

Participations: 43

Other Complementary Information

Latest proceeding published in BORME: 18/07/2008 Change

of statutes

Latest press article: 11/07/2008 EXPANSION

DE VALENCIA (SOCIAL INFORMATION)

Bank Entities: Yes

Credit Appraisal

Maximum Credit (from 0 a 6,000,000 €):

3.591.648,34 €

Rating Evolution

Financial Situation

Fiscal year2006

|

Treasury |

Excellent |

|

Indebtedness |

Important |

|

Profitability |

Unfavourable |

|

Balance |

Very good |

Performance

|

Legal Actions |

None or

Negligible |

|

Business Trajectory |

Excellent |

RAI

COMPANY NOT REGISTERED IN THE R.A.I.

This company is not registered in the Disputed Bills register (R.A.I.)

DATE AND TIME OF THE CONSULTATION: 22/07/2008

08:07:00

INCIDENTS

Summary

LEGAL ACTIONS: No legal incidences registered

CLAIM FILED AGAINST THE ADMINISTRATION: No administrative

claims registered

AFFECTED BY: No significant element.

FINANCIAL ELEMENTS AND SECTORIAL

COMPARATIVE

FINANCIAL ELEMENTS

Figures given in €

|

|

2005 (4) |

2006 (12) |

2007 |

|

|

BALANCE SHEET ANALYSIS |

|

|

|

|

|

OWN FUNDS |

60.120,00 |

66.897.000,00 |

|

|

|

DEBT |

|

549.767.000,00 |

|

|

|

FIXED ASSETS |

601,20 |

399.386.000,00 |

|

|

|

TOTAL ASSETS |

60.120,00 |

616.664.000,00 |

|

|

|

|

|

|

|

|

|

|

2005 (4) |

2006 (12) |

2007 |

|

|

PROFIT AND LOSS ACCOUNT ANALYSIS |

|

|

|

|

|

SALES |

|

300.087.000,00 |

309.089.610,00 |

|

|

ADDED VALUE |

|

99.854.000,00 |

|

|

|

EBITDA |

|

47.888.000,00 |

|

|

|

EBIT |

|

19.102.000,00 |

|

|

|

NET RESULT |

|

-3.101.000,00 |

|

|

ANNUAL FINANCIAL REPORT

ADDITIONAL DATA

Source: annual financial report 2006

Results Distribution

Figures given in €

|

DISTRIBUTION

BASE |

DISTRIBUTION TO |

||

|

Profit and Loss |

-3.100.827,48 |

Retained earnings |

0,00 |

|

Carry Over |

0,00 |

Voluntary Reserve |

0,00 |

|

Voluntary reserves |

0,00 |

Prior years losses |

-3.100.827,48 |

|

Reserves |

0,00 |

Carry Over |

0,00 |

|

Other concepts |

0,00 |

Other funds |

0,00 |

|

Total of Amounts to be distributed |

-3.100.827,48 |

Dividends |

0,00 |

|

|

|

Other Applications |

0,00 |

Auditing

Auditors’ opinion: FAVOURABLE WITH RESERVATIONS

Auditor: KPMG AUDITORES S.L.

Auditing exceptions:

COMO SE DETALLA EN LA NOTA 1 DE LA MEMORIA ADJUNTA, EL 1 DE MARZO DE

2006 LA SOCIEDAD FIRMO VARIOS CONTRATOS DE COMPRAVENTA DE ACCIONES DE DIVERSAS

SOCIEDADES, CUYA EJECUCION QUEDABA SUPEDITADA AL CUMPLIMIENTO DE DETERMINADAS

CONDICIONES SUBVERSIVAS EN ELLAS INCLUIDAS. LOS FIRMANTES DE DICHOS CONTRATOS

CONSIDERARON CUMPLIDOS EL 5 DE MAYO DE 2006 DICHAS CONDICIONES, LO QUE SE

DENOMINA COMO FECHA DE EJECUCION SEGUN LOS TERMINOS DESCRITOS EN LOS MISMOS, Y

PROCEDIERON EN DICHA FECHA A OTORGAR ESCRITURAS PUBLICAS DE COMPRAVENTA DE

ACCIONES Y A LLEVAR A CABO EL RESTO DE OPERACIONES NECESARIAS PARA CONSIDERAR

EJECUTADAS LAS COMPRAVENTAS. POSTERIORMENTE, CON FECHA 30 DE JUNIO DE 2006 LAS

JUNTAS GENERALES DE ACCIONISTAS / SOCIOS DE LA SOCIEDAD Y DE UNA PARTE DE LAS SOCIEDADES

QUE FUERON ADQUIRIDAS EL 5 DE MAYO APROBARON LA FUSION POR ABSORCION DE ESAS

SOCIEDADES, SIENDO INVEST EXPERIENCE 2005, S.A. (ACTUALMENTE LEVANTINA Y

ASOCIADOS DE MINERALES, S.A.) LA SOCIEDAD ABSORBENTE. LA SOCN

COMPARATIVE SECTOR ANALYSIS

Values table

Figures expressed in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

BALANCE SHEET ANALYSIS: % on the total

assets |

|

|

|

|

|

OWN FUNDS |

10,85 |

39,36 |

-28,51 |

-72,44 |

|

DEBT |

89,15 |

60,64 |

28,51 |

47,01 |

|

FIXED ASSETS |

64,77 |

41,06 |

23,71 |

57,75 |

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

PROFIT AND LOSS ACCOUNT ANALYSIS: % on the total

operating income |

|

|

|

|

|

SALES |

99.601,71 |

98,99 |

99.502,71 |

100.513,88 |

|

ADDED VALUE |

33.142,49 |

30,02 |

33.112,47 |

110.308,71 |

|

EBIT |

6.340,13 |

11,77 |

6.328,36 |

53.762,32 |

|

NET RESULT |

-1.029,25 |

7,56 |

-1.036,81 |

-13.719,84 |

Sector Composition

Compared sector (NACE): 267

Number of companies: 39

Size (Sales Figure) : > 7.000.000,00 Euros

Comments on the sectorial

comparative

Compared to its sector the assets of the companies show a greater

proportion of fixed assets. Specifically the difference with the sector average

is 23,71% , which means a relative difference of 57,75% .

In liabilities composition the company appeals on a wider scale to self

financing, being the proportion of net worth of 28,51% inferior, which means a

relative difference of 72,44% 28,51% more than the sector, which means a

difference of 47,01% .

The proportion that the sales mean to the company’s total ordinary

income is 99.601,71%, 99.502,71% higher than in the sector, which means a

relative difference of 100.513,88% .

The company’s EBIT was positive and was 6.340,13% with regard to the

total ordinary income, 6.328,36% higher than in the sector, which means a

relative difference of 53.762,32% .

The company’s capacity to generate operating income is equal to that of

the sector as its ratio EBIT/Sales is also equal.

The company’s net result was negative and equal to -1.029,25% with

regard to the total ordinary income, 1.036,81% less than the sector, which

means a relative difference of 13.719,84% .

ADDRESSES

Current Legal Seat Address:

CARRETERA AUTOVIA 330, S/N - APARTADO CORREOS 8

03660 NOVELDA ALICANTE

Previous Seat Address:

CARRETERA AUTOVIA 330 KM,

03660

NOVELDA ALICANTE

Characteristics of the current

address

Type of premises: store

Property: owned; with no official confirmation

Local Situation: main

Branches

|

STREET |

POSTAL CODE |

TOWN |

PROVINCE |

|

POLIGONO INDUSTRIAL GANDARAS DE BUDINO S/N |

36400 |

O PORRIÑO |

Pontevedra |

1 branches registered

CORPORATE STRUCTURE

ADMINISTRATIVE LINKS

Main Board members, Directors and Auditor ![]()

|

POSITION |

SURNAMES AND

NAME |

APPOINTMENT DATE |

|

|

PRESIDENT |

SPINNAKER HOLDINGS SARL |

04/03/2008 |

|

|

MANAGING DIRECTOR |

PINOS ZAMORA ANTONIO JOSE |

12/02/2008 |

|

|

CHIEF OFFICER |

CABERWOOD SARL |

30/06/2006 |

|

|

CHIEF OFFICER |

CHARTERHOUSE CORPORATE DIRECTORS LIMITED |

30/06/2006 |

|

|

CHIEF OFFICER |

SOCIEDAD GALLEGA DE ROCAS ORNAMENTALES S L |

10/01/2007 |

|

|

SECRETARY |

MERINO SANZ FEDERICO |

30/06/2006 |

|

|

AUDITOR |

APPOINTMENT DATE |

||

|

KPMG AUDITORES SL |

02/02/2007 |

||

Functional Managers

|

POSITION |

SURNAMES AND

NAME |

|

General Manager |

PINOS ZAMORA ANTONIO |

|

Financial Manager |

CUADRA LA FUENTE FRANCISCO |

|

Human Resources Manager |

COUTO VIVAS JORGE |

FINANCIAL LINKS

|

|

BUSINESS NAME |

CIF / COUNTRY |

% |

SOURCE |

DATA INF. |

|

|

ANTINEA INVERSIONES S.L. |

B53591418 |

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

GALLARDO GALLARDO ANTONIA |

|

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

MARCELINO MARTINEZ SL |

B36010098 |

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

HIDALGO MURILLO FERNANDA |

|

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

DIMORPHANDRA S.L. |

B53290961 |

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

SPINNAKER HOLDINGS SARL |

|

Indet. |

OWN SOURCES |

21/04/2008 |

|

|

BUSINESS NAME |

CIF / COUNTRY |

% |

SOURCE |

DATA INF. |

|

|

GRANINTER DEUTSCHLAND GMBH |

GERMANY |

100,00 |

OWN SOURCES |

21/04/2008 |

|

|

GRANINTER USA INC |

ESTADOS UNIDOS |

100,00 |

OWN SOURCES |

21/04/2008 |

|

|

BERMARMOL SA |

A81725350 |

100,00 |

OWN SOURCES |

21/04/2008 |

|

|

GRANITOS IBERLUSOS LDA |

PORTUGAL |

100,00 |

OWN SOURCES |

21/04/2008 |

|

|

GRANINTER INDIA PVT LTDA |

INDIA |

100,00 |

OWN SOURCES |

21/04/2008 |

|

|

LUSO LEVANTINA DISTRIBUGAO DE GRANITO |

PORTUGAL |

100,00 |

OWN SOURCES |

21/04/2008 |

You can obtain business information of a foreign company at the

pageD&B International

CREDIT INFORMATION

Constitution Date: 16/08/2005

Foundation Date: 01/01/2005

Founder / Origin: LA TITULAR ES LA FUNDADORA INICIAL DEL NEGOCIO

Business activity

Code: 1244000

Activity: Natural stone industries

NACE Code: 2670

NACE Activity: Cutting, shaping and finishing of stone

Business: LA EXPLOTACION, ADQUISICION Y ARRENDAMIENTO DE

CANTERAS, PERMISOS DE INVESTIGACION Y OTROS TERRENOS; LA EXPLOTACION DE

SERRERIAS Y TALLERES DE LABRA DE PIEDRAS NATURALES DE TODAS CLASES; LA

COMERCIALIZACION DE MARMOLES,

Employees

Number of total employees: 2.500 (2008)

Number of fixed employees: 75,50%

Number of temporary employees: 24,50%

COMMERCIAL OPERATIONS

SUPPLIERS

|

BUSINESS NAME |

INTERNATIONAL |

|

CASABLANCA

MARBLE & GRANITE SARL |

YES |

|

QUARZT STONE

PLUS SLU |

NO |

|

JOSE MARIA MAÑEZ

VERDU SA |

NO |

|

GRANINTER SA |

NO |

|

GRANITOS

IBEROLUSOS LDA |

YES |

|

GRANINTER

PRODUCCION SA |

NO |

|

CANTERAS VISEMAR

SLU |

NO |

|

CANTERAS

CORALITO SL |

NO |

|

GRANINTER INDIA

PVT LDA |

YES |

|

EXMINERA SL |

NO |

10 proveedores

CLIENTS

|

BUSINESS NAME |

INTERNATIONAL |

|

GANITOS

IBEROLUSOS LTDA |

YES |

|

QUARTZ STONE

PLUS SL |

NO |

|

GRANINTER POLSKA

SP ZOO |

YES |

|

GRANINTER USA |

YES |

|

CASABLANCA

MARBLE & STONE SARL |

YES |

|

LUSO LEVANTINA

DIST GTO LDA |

YES |

|

GRANINTER SA |

NO |

|

JOSE MARIA MAÑEZ

VERDU SA |

NO |

|

LEVANTINA DE

GRANITOS BRASIL LTDA |

YES |

9 clientes

Banks

|

ENTITY |

BRANCH |

ADDRESS |

TOWN OR CITY |

PROVINCE |

|

BANCO BILBAO VIZCAYA ARGENTARIA, S.A. |

|

|

NOVELDA |

|

|

BANCO DE SABADELL, S.A. |

|

|

|

|

|

BANCO DE VALENCIA, S.A. |

|

|

|

|

|

BANCO PASTOR, S.A. |

|

|

|

|

|

BANKINTER, S.A. |

|

|

|

|

8 bank entities registered

Brands, Signs and Commercial

Names

FORMER NAMES:

•

INVEST EXPERIENCE 2005 S.A.

LEGAL STRUCTURE

Constitution Data

Register Date: 16/08/2005

Register town: Madrid

Announcement number: 417053

Register Data:

Volume 21748, Book 0, Folio 73, Section 8, Sheet 387354

Legal form: JOINT STOCK COMPANY

Social Capital: 0 €

Current structure data

Current Legal Form: JOINT STOCK COMPANY

Current Capital: 10.676.651,80 €

Legal Aspects

Obligation to fill in Financial Statements: YES

Chamber census: YES (2006)

Listed on a Stock Exchange: NO

B.O.R.M.E.(Official Companies

Registry Gazette)

Registered Proceedings

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Change of statutes |

18/07/2008 |

351975 |

Alicante |

|

Change of statutes |

16/07/2008 |

348735 |

Alicante |

|

Resignations |

05/06/2008 |

279361 |

Alicante |

Other Proceedings published

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Fusion by absorption project |

11/06/2008 |

165034 |

Alicante |

|

Fusion by absorption project |

05/06/2008 |

160777 |

Valencia |

Press articles

11/07/2008 EXPANSION DE VALENCIA (SOCIAL INFORMATION)

DE LOS 195 TRABAJADORES A LOS QUE SE PLANTEO EL EXPEDIENTE DE REGULACION

DE EMPLEO EN LEVANTINA, 72 HAN PASADO A LOS CENTROS DEL GRUPO EN NOVELDA. LOS

123 RESTANTES FINALIZAN SUS CONTRATOS (10 DE ELLOS DE FORMA VOLUNTARIA).

11/07/2008 LA VOZ DE ALMERIA (BRANCHES INFORMATION)

LEVANTINA, EL PRODUCTOR DE PIEDRA VALENCIANO, HA ANUNCIADO LA APERTURA

DE UNA NUEVA DELEGACION EN ALMERIA. ESTA DECISION CONTRASTA CON EL PROYECTO DE CERRAR

DOS DE LAS FACTORIAS QUE POSEE EN NOVELDA (ALICANTE).

FINANCIAL INFORMATION

The information on the last account contained in this report is

extracted from the Mercantile Register file of the legal address of the Company

and dated 23/10/2007.

BALANCE SHEET

Assets

Figures given in €

|

|

31/12/2005 (4) |

31/12/2006 (12) |

|

A) DUE FROM SHAREHOLDERS FOR UNCALLED CAPITAL |

|

|

|

B) FIXED ASSETS |

601,20 |

399.386.000,00 |

|

I. Incorporation costs |

601,20 |

1.778.000,00 |

|

II. Intangible fixed assets |

|

119.982.000,00 |

|

III. Tangible fixed assets |

|

131.473.000,00 |

|

IV. Financial fixed assets |

|

141.854.000,00 |

|

V.Owners equity |

|

4.299.000,00 |

|

VI.Long term trade liabilities |

|

|

|

C) DEFERRED EXPENSES |

|

316.000,00 |

|

D) CURRENT ASSETS |

59.518,80 |

216.962.000,00 |

|

I. Shareholders by required outlays |

|

|

|

II. Stocks |

|

68.301.000,00 |

|

III. Debtors |

|

144.872.000,00 |

|

IV. Temporary financial investment |

|

533.000,00 |

|

V. Short-term own shares |

|

|

|

VI. Treasury |

59.518,80 |

2.358.000,00 |

|

VII. Periodification adjustments |

|

898.000,00 |

|

ASSETS (A + B + C + D) |

60.120,00 |

616.664.000,00 |

Assets composition

Liabilities

Figures given in €

|

|

31/12/2005 (4) |

31/12/2006 (12) |

|

A) SHAREHOLDERS EQUITY |

60.120,00 |

65.899.000,00 |

|

I. Share capital |

60.120,00 |

13.800.000,00 |

|

II. Issue bonus |

|

55.200.000,00 |

|

III.Revaluation reserve |

|

|

|

IV.Reserves |

|

|

|

Capital adjustments in Euros |

|

|

|

Sundry reserves |

|

|

|

V.Results from previous years |

|

|

|

VI.Profit and Losses |

|

-3.101.000,00 |

|

VII.Dividend paid during the year |

|

|

|

VIII.Own shares for capital reduction |

|

|

|

B) DEFERRED INCOME |

|

998.000,00 |

|

C) PROVISIONS FOR LIABILITIES AND EXPENSES |

|

1.400.000,00 |

|

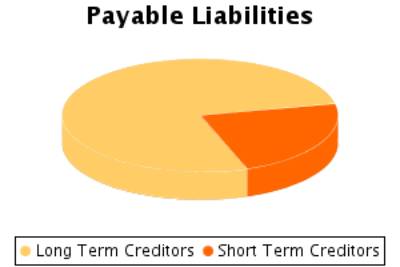

D) LONG TERM LIABILITIES |

|

424.069.000,00 |

|

E) SHORT TERM LIABILITIES |

|

124.298.000,00 |

|

F) SHORT TERM PROVISIONS FOR LIABILITIES AND

EXPENSES |

|

|

|

LIABILITIES (A + B + C + D + E + F) |

60.120,00 |

616.664.000,00 |

Liabilities Composition

PROFIT AND LOSS ACCOUNT

Itams of the Profit and Loss Account

Figures given in €

|

|

31/12/2005 (4) |

31/12/2006 (12) |

|

|

A) EXPENSES (A.1 a A.15) |

|

312.553.000,00 |

|

|

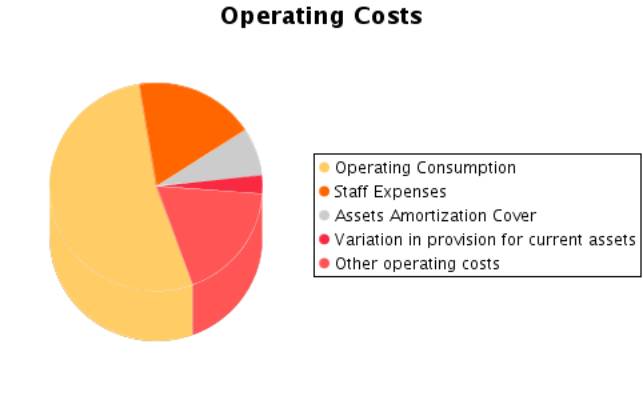

A.1.Operating costs |

|

149.517.000,00 |

|

|

A.2. Labour cost |

|

51.966.000,00 |

|

|

Wages |

|

40.158.000,00 |

|

|

Social security expenses |

|

11.808.000,00 |

|

|

A.3. Assets depreciation |

|

20.748.000,00 |

|

|

A.4. Variation in provision for current assets |

|

8.038.000,00 |

|

|

A.5. Other operating costs |

|

51.916.000,00 |

|

|

A.I. OPERATING RESULT (B.1-A.1-A.2-A.3-A.4-A.5) |

|

19.102.000,00 |

|

|

A.6.Financial expenses and similar |

|

19.541.000,00 |

|

|

Debts with related companies |

|

343.000,00 |

|

|

Debts with associated companies |

|

|

|

|

Other companies debts By debts with third parties and similar expenses |

|

19.189.000,00 |

|

|

Losses from financial investments |

|

9.000,00 |

|

|

A.7. Variation in financial investment provision |

|

100.000,00 |

|

|

A.8.Negative exchange difference |

|

2.801.000,00 |

|

|

A.II.POSITIVE FINANCIAL RESULTS

(B.2+B.3-A.6-A.7-A.8) |

|

|

|

|

A.III.PROFIT FROM ORDINARY ACTIVITIES (A.I+A.II-B.I-B.II) |

|

|

|

|

A.9. Variation in provision in fixed assets |

|

2.439.000,00 |

|

|

A.10. Losses in fixed assets |

|

342.000,00 |

|

|

A.11. Losses from own shares and bonds |

|

|

|

|

A.12. Extraordinary charges |

|

6.206.000,00 |

|

|

A.13.Other exercises’ expenses and losses |

|

2.182.000,00 |

|

|

A.IV.POSITIVE EXTRAORDINARY RESULT

(B.4+B.5+B.6+B.7+B.8-A.9-A.10-A.11-A.12-A.13) |

|

|

|

|

A.V.PROFIT BEFORE TAXES (A.III+A.IV-B.III-B.IV) |

|

|

|

|

A.14.Corporate Taxes |

|

-3.243.000,00 |

|

|

A.15. Other taxes |

|

|

|

|

A.VI.EXERCISE RESULT (PROFIT) (A.V-A.14-A.15) |

|

|

|

|

B) INCOMES (B.1 a B.8) |

|

309.452.000,00 |

|

|

B.1.Operating income |

|

301.287.000,00 |

|

|

Turnover |

|

300.087.000,00 |

|

|

Other operating income |

|

1.200.000,00 |

|

|

B.I.OPERATING LOSSES (A.1+A.2+A.3+A.4+A.5-B.1) |

|

|

|

|

B.2.Financial Income |

|

1.398.000,00 |

|

|

From affiliated companies |

|

433.000,00 |

|

|

From associated companies |

|

100.000,00 |

|

|

Other |

|

726.000,00 |

|

|

Gains from investments |

|

139.000,00 |

|

|

B.3. Positive change difference |

|

1.646.000,00 |

|

|

B.II. NEGATIVE FINANCIAL RESULTS

(A.6+A.7+A.8-B.2-B.3) |

|

19.398.000,00 |

|

|

B.III.LOSSES FROM ORDINARY ACTIVITIES (B.I+B.II-A.I-A.II) |

|

296.000,00 |

|

|

B.4.B.9. Gains from disposal of fixed assets |

|

4.240.000,00 |

|

|

B.5.Gains from dealing in own shares |

|

|

|

|

B.6. Paid in surplus |

|

204.000,00 |

|

|

B.7. Extraordinary income |

|

263.000,00 |

|

|

B.8.Other year’s income and profits |

|

414.000,00 |

|

|

B.IV.NEGATIVE EXTRAORDINARY LOSSES

(A.9+A.10+A.11+A.12+A.13-B.4-B.5-B.6-B.7-B.8) |

|

6.048.000,00 |

|

|

B.V.LOSS BEFORE TAXES (B.III+B.IV-A.III-A.IV) |

|

6.344.000,00 |

|

|

B.VI.EXERCISE RESULTS (LOSS) (B.V+A.14+A.15) |

|

3.101.000,00 |

|

Composition of the Profit and

Loss Account

FINANCIAL BALANCE

Here the Main Capital Amounts of the company and the Revolving Fund

Evolution are analysed.

Financial Balance Table

Figures given in €

|

|

31/12/2005 (4) |

% |

31/12/2006 (12) |

% |

|

A) DUE FROM SHAREHOLDERS FOR UNCALLED CAPITAL |

|

|

|

|

|

B) FIXED ASSETS |

601,20 |

1,00 |

399.386.000,00 |

64,77 |

|

C) DEFERRED EXPENSES |

|

|

316.000,00 |

0,05 |

|

D) CURRENT ASSETS |

59.518,80 |

99,00 |

216.962.000,00 |

35,18 |

|

ASSETS (A + B + C + D) |

60.120,00 |

|

616.664.000,00 |

|

|

|

|

|

|

|

|

A) SHAREHOLDERS EQUITY |

60.120,00 |

100,00 |

65.899.000,00 |

10,69 |

|

B) DEFERRED INCOME |

|

|

998.000,00 |

0,16 |

|

C) PROVISIONS FOR LIABILITIES AND EXPENSES |

|

|

1.400.000,00 |

0,23 |

|

D) LONG TERM LIABILITIES |

|

|

424.069.000,00 |

68,77 |

|

E) SHORT TERM LIABILITIES |

|

|

124.298.000,00 |

20,16 |

|

F) SHORT TERM PROVISIONS FOR LIABILITIES AND EXPENSES |

|

|

|

|

|

LIABILITIES (A + B + C + D + E + F) |

60.120,00 |

|

616.664.000,00 |

|

Financial Balance Composition

Comments on Financial Balance

In the 2005, the assets of the company were formed in 1,00% of Fixed

Assets and in 99,00% of Current Assets.This assets were financed in 100,00%

with own capitals% with long term debt% with current liabilities.

The result of this financial structure is a positive turnover fund of

59.518,80 Euros, which is equivalent to 99,00% proportion of the

company’s total assets.

In the 2006, the assets of the company were formed in 64,82% of Fixed

Assets and in 35,18% of Current Assets.This assets were financed in 10,85% with

own capitals, and in 69,00% with long term debt and in 20,16% with current

liabilities.

The result of this financial structure is a positive turnover fund of

92.664.000,00 Euros, which is equivalent to 15,03% proportion of the

company’s total assets.

RATIOS

Main Ratios

|

|

31/12/2005 (4) |

31/12/2006 (12) |

|

|

STRUCTURAL RATIOS |

|

|

|

|

Management fund |

59.518,80 |

92.664.000,00 |

|

|

Management Fund Requirement |

|

127.195.000,00 |

|

|

Indebtedness (%) |

|

89,15 |

|

|

External Funds on Net Worth |

|

8,22 |

|

|

GENERAL ACTIVITY RATIO |

|

|

|

|

Cash Flow |

|

28.224.000,00 |

|

|

Labour Productivity |

|

1,92 |

|

|

Assets turnover |

|

0,49 |

|

|

Breakdown Point |

|

263.366.566,00 |

|

|

Security Margin of the Breakdown Point (%) |

|

12,59 |

|

|

ACTIVITY RATIOS |

|

|

|

|

Average Payment Period |

|

114 |

|

|

Average Collection Period |

|

174 |

|

|

Inventory Turnover Period |

|

82 |

|

|

SOLVENCY RATIOS |

|

|

|

|

Payback Capacity |

|

0,05 |

|

|

Assets Guarantee |

|

1,12 |

|

|

Short Term Debts Proportion (%) |

|

22,61 |

|

|

Interest Coverage |

|

0,56 |

|

|

LIQUIDITY RATIOS |

|

|

|

|

Current Ratio |

|

1,74 |

|

|

Immediate liquidity |

|

0,02 |

|

|

Treasury |

|

-34.531.000,00 |

|

|

Sales on Current Assets |

|

498 |

|

Results Analysis Ratios

|

|

31/12/2005 (4) |

31/12/2006 (12) |

|

|

Economic profitability (%) |

|

3,10 |

|

|

Operating Profitability (%) |

|

6,36 |

|

|

Equity gearing |

|

-0,14 |

|

|

Financial profitability (%) |

|

-4,64 |

|

|

General Profitability (%) |

|

-1,03 |

|

SECTORIAL ANÁLYSIS

Large Capital Amounts and Financial Balance

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

ASSETS |

|

|

|

|

|

A) DUE FROM SHAREHOLDERS FOR UNCALLED CAPITAL |

|

0,00 |

|

|

|

B) FIXED ASSETS |

64,77 |

41,06 |

23,71 |

57,76 |

|

C) DEFERRED EXPENSES |

0,05 |

0,10 |

-0,05 |

-48,45 |

|

D) CURRENT ASSETS |

35,18 |

58,85 |

-23,67 |

-40,22 |

|

ASSETS (A + B + C + D) |

100 |

100 |

|

|

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

LIABILITIES |

|

|

|

|

|

A) SHAREHOLDERS EQUITY |

10,69 |

36,34 |

-25,65 |

-70,58 |

|

B) DEFERRED INCOME |

0,16 |

3,02 |

-2,86 |

-94,70 |

|

C) PROVISIONS FOR LIABILITIES AND EXPENSES |

0,23 |

0,20 |

0,04 |

17,95 |

|

D) LONG TERM LIABILITIES |

68,77 |

13,09 |

55,68 |

425,28 |

|

E) SHORT TERM LIABILITIES |

20,16 |

47,36 |

-27,20 |

-57,43 |

|

F) SHORT TERM PROVISIONS FOR LIABILITIES AND EXPENSES |

|

0,00 |

|

|

|

LIABILITIES (A + B + C + D + E + F) |

100 |

100 |

|

|

Financial Balance Composition

Comments to the Sectorial

Analysis

In the 2006, the assets of the company were formed in 64,82% of fixed

assets and in 35,18Current Assets % In the sector, the proportion of fixed

assets was of 41,15%, 57,51% inferior, and the proportion of current assets was

of 58,85%, 40,22% superior.

The assets were financed in the company in 10,85% with own capitals , in

69,00% with fixed liabilities and in 20,16% with current liabilities In the

sector, the self financing represented 39,36%, 72,43% superior. On the other

hand the long term debts represented in the sector an average of 13,29%

financing, with a relative difference of 419,30% in favour of the companyAnd,

short term liabilities represented in the sector an average of 47,36%

financing, with a relative difference of 57,43% favourable to the sector

The result of this company’s financial structure is a turnover fund that

represents 15,03% of the total assets; in the sector, this same proportion is

11,49%, therefore, we can say that the company’s turnover fund is 30,80% higher

than the one in of the sector.

Analytical Account of Results

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

Turnover |

99,60 |

98,99 |

0,61 |

0,61 |

|

Other operating income |

0,40 |

1,01 |

-0,61 |

-60,24 |

|

Production Value |

100,00 |

100,00 |

0,00 |

0,00 |

|

Operating expenses |

49,63 |

51,18 |

-1,55 |

-3,03 |

|

Other operation expenses |

17,23 |

18,80 |

-1,57 |

-8,35 |

|

Added value |

33,14 |

30,02 |

3,12 |

10,40 |

|

Labour cost |

17,25 |

12,88 |

4,37 |

33,97 |

|

Gross Economic Result |

15,89 |

17,14 |

-1,25 |

-7,30 |

|

Assets depreciation |

6,89 |

4,47 |

2,42 |

54,04 |

|

Variation in provision for current assets and bad debt losses |

2,67 |

0,90 |

1,77 |

197,66 |

|

Net Economic Result |

6,34 |

11,77 |

-5,43 |

-46,14 |

|

Financial income |

1,01 |

1,46 |

-0,45 |

-30,73 |

|

Financial Charges |

7,42 |

2,86 |

4,56 |

159,53 |

|

Variation in financial investment provision |

0,03 |

-0,01 |

0,04 |

-528,57 |

|

Ordinary Activities Result |

-0,10 |

10,38 |

-10,48 |

-100,96 |

|

Extraordinary income |

1,70 |

0,98 |

0,72 |

73,82 |

|

Extraordinary charges |

2,90 |

0,56 |

2,34 |

418,78 |

|

Variation in provision in fixed assets |

0,81 |

0,22 |

0,59 |

275,00 |

|

Results before Taxes |

-2,11 |

10,58 |

-12,69 |

-119,94 |

|

Corporate taxes |

-1,08 |

3,02 |

-4,10 |

-135,73 |

|

Net Result |

-1,03 |

7,56 |

-8,59 |

-113,63 |

|

Assets depreciation |

6,89 |

4,47 |

2,42 |

54,04 |

|

Change of Provisions |

3,51 |

1,11 |

2,40 |

217,07 |

|

Net Self-Financing |

9,37 |

13,14 |

-3,77 |

-28,67 |

Main Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

STRUCTURAL RATIOS |

|

|

|

|

|

Management fund |

92.664.000,00 |

-221,55 |

2.005,50 |

3.442,68 |

|

Management Fund Requirement |

127.195.000,00 |

-5.776,21 |

-1.177,42 |

735,00 |

|

Indebtedness (%) |

89,15 |

49,90 |

62,01 |

72,54 |

|

External Funds on Net Worth |

8,22 |

1,00 |

1,63 |

2,64 |

|

GENERAL ACTIVITY RATIO |

|

|

|

|

|

Cash Flow |

28.224.000,00 |

667,00 |

1.038,00 |

1.676,48 |

|

Labour Productivity |

1,92 |

1,58 |

1,99 |

2,46 |

|

Assets turnover |

0,49 |

0,80 |

0,93 |

1,24 |

|

Breakdown Point |

263.366.566,00 |

7.040.182,86 |

10.601.758,75 |

16.126.471,04 |

|

Security Margin of the Breakdown Point (%) |

12,59 |

8,93 |

12,94 |

19,60 |

|

ACTIVITY RATIOS |

|

|

|

|

|

Average Payment Period |

114 |

80 |

116 |

164 |

|

Average Collection Period |

174 |

120 |

140 |

162 |

|

Inventory Turnover Period |

82 |

28 |

61 |

81 |

|

SOLVENCY RATIOS |

|

|

|

|

|

Payback Capacity |

0,05 |

0,09 |

0,16 |

0,26 |

|

Assets Guarantee |

1,12 |

1,38 |

1,61 |

2,00 |

|

Short Term Debts Proportion (%) |

22,61 |

74,80 |

82,03 |

91,48 |

|

Interest Coverage |

0,56 |

2,30 |

5,10 |

15,33 |

|

LIQUIDITY RATIOS |

|

|

|

|

|

Current Ratio |

1,74 |

0,95 |

1,25 |

1,66 |

|

Immediate liquidity |

0,02 |

0,03 |

0,07 |

0,24 |

|

Treasury |

-34.531.000,00 |

-3.855,10 |

-1.373,98 |

484,73 |

|

Sales on Current Assets |

498 |

459 |

554 |

707 |

Results Analysis Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

Economic profitability (%) |

3,10 |

2,55 |

5,74 |

9,90 |

|

Operating Profitability (%) |

6,36 |

3,27 |

6,03 |

7,94 |

|

Equity gearing |

-0,14 |

1,24 |

1,80 |

3,10 |

|

Financial profitability (%) |

-4,64 |

4,27 |

8,98 |

17,68 |

|

General Profitability (%) |

-1,03 |

1,48 |

3,02 |

5,90 |

FOREIGN EXCHANGE

RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs. 41.96 |

|

UK Pound |

1 |

Rs. 83.78 |

|

Euro |

1 |

Rs. 65.82 |

RATING

EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit

consideration. Capability to overcome financial difficulties seems

comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)