![]()

MIRA

INFORM REPORT

|

Report Date : |

24.06.2008 |

IDENTIFICATION

DETAILS

|

Name : |

KIMROC S.L. |

|

|

|

|

Registered Office : |

Street Ourense, 59 27004 Lugo |

|

|

|

|

Country : |

Spain |

|

|

|

|

Financials (as on) : |

31.12.2006 |

|

|

|

|

Date of Incorporation : |

|

|

|

|

|

Legal Form : |

Limited Liability Company |

|

|

|

|

Line of Business : |

RATING &

COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Maximum Credit Limit : |

6.010,12 € |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

FINANCIAL REPORT

KIMROC S.L.

TAX NUMBER: B27243955

EXECUTIVE SUMMARY

Identification

Current Business Name: KIMROC S.L.

Other names: NO

Current Address: STREET OURENSE, 59, CP 27004 LUGO

Telephone number: 982231002 Fax: 986343986

URL: www.kimroc.com Corporate e-mail: francisco.jdematos@tormat.com

Commercial Risk

Credit Appraisal: 6.010,12 €

Legal Actions: NO

Financial Information

Latest Balance sheet sales (2006): 67.704,05 € (MERCANTILE REGISTER)

Result: 914,13 €

Total Assets: 67.544,16 €

Social Capital: 36.061,00 €

Employees: 1

Commercial Information

Constitution Date: 19/05/1999

Business activity: Retail sale

in specialized stores

NACE Code: 5248

International Operations: No business

relationships registered

Corporate Structure

Administrator:

DE MATOS

CARRASCO FRANCISCO JOSE

Other Complementary Information

Latest proceeding published in BORME: 14/08/2007 Registration

of accounts

Bank Entities: No

Credit Appraisal

Maximum Credit (from 0 a 6,000,000 €):

6.010,12 €

Rating Evolution

Financial Situation

Fiscal year2006

|

Treasury |

Excellent |

|

Indebtedness |

Nil |

|

Profitability |

Average |

|

Balance |

Excellent |

Performance

|

Legal Actions |

None or Negligible |

|

Business

Trajectory |

Excellent |

INCIDENTS

Summary

LEGAL ACTIONS: No legal

incidences registered

CLAIM FILED AGAINST THE ADMINISTRATION: No administrative

claims registered

AFFECTED BY: No significant

element.

FINANCIAL ELEMENTS AND SECTORIAL

COMPARATIVE

FINANCIAL ELEMENTS

Figures given in €

|

|

2004 (12) |

2005 (12) |

2006 (12) |

% ASSETS |

|

|

|

|

|

|

BALANCE SHEET

ANALYSIS |

|

|

|

|

|

|

|

|

|

|

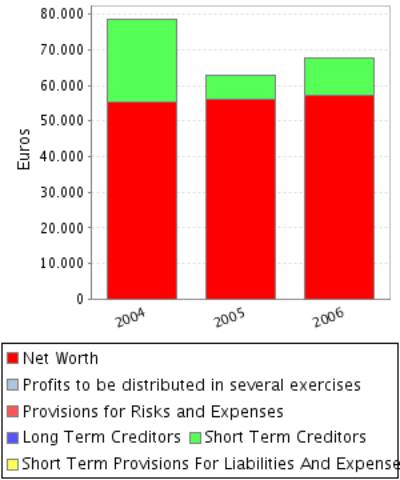

OWN FUNDS |

55.334,39 |

56.181,87 |

57.096,00 |

84,53 |

|

|

|

|

|

|

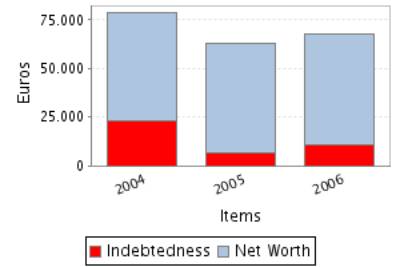

DEBT |

23.217,78 |

6.453,00 |

10.448,16 |

15,47 |

|

|

|

|

|

|

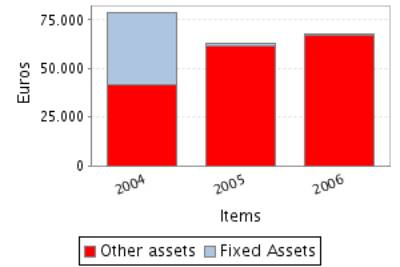

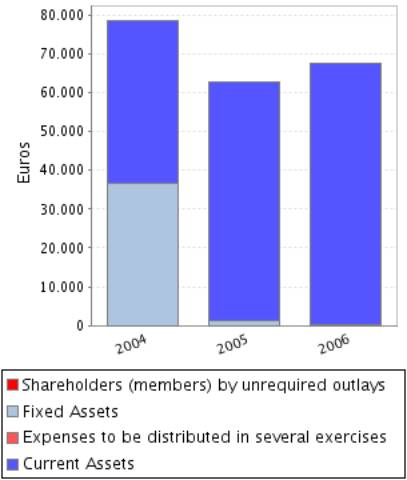

FIXED ASSETS |

36.803,67 |

1.106,67 |

276,67 |

0,41 |

|

|

|

|

|

|

TOTAL ASSETS |

78.552,17 |

62.634,87 |

67.544,16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2004 (12) |

2005 (12) |

2006 (12) |

% SALES |

|

|

|

|

|

|

PROFIT AND LOSS

ACCOUNT ANALYSIS |

|

|

|

|

|

|

|

|

|

|

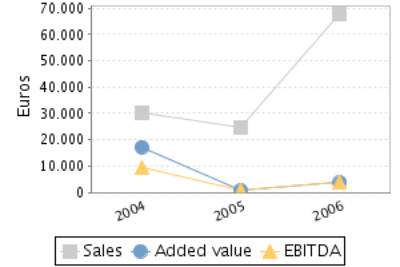

SALES |

30.283,60 |

24.800,00 |

67.704,05 |

|

|

|

|

|

|

|

ADDED VALUE |

17.218,83 |

708,81 |

3.680,27 |

5,44 |

|

|

|

|

|

|

EBITDA |

9.517,51 |

708,81 |

3.680,27 |

5,44 |

|

|

|

|

|

|

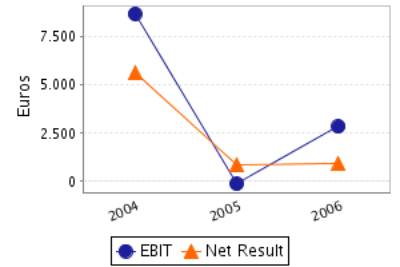

EBIT |

8.687,51 |

-121,19 |

2.850,27 |

4,21 |

|

|

|

|

|

|

NET RESULT |

5.639,47 |

847,21 |

914,13 |

1,35 |

|

|

|

|

|

Balance Sheets Items

Analysis

Balance Sheet

Comments

Total assets of the company decreased in 20,26% between 2004 and 2005.

This decrease has been greater in the fixed assets that reduced in

-96,99%.

Assets reduction contrasts with net worth growth of 1,53%. Therefore,

the company’s indebtedness has reduced in 72,21%.

Total assets of the company grew 7,84% between 2005 and 2006.

In spite of the assets’ growth, the fixed assets decreased 75,00%.

This growth has been mainly financed with a debt increase of 61,91%.

Nevertheless the net worth increased 1,63%.

Profit and Loss Account Analysis

Profit and Loss

Account Comments

The company’s sales figure decreased in 18,11% between 2004 and 2005.

The company’s EBIT decreased in 101,39% between 2004 and 2005.

This evolution implies a reduction in the company’s operating

profitability.

The result of these variations is a decrease of the company’s Economic

Profitability of 101,75% in the analysed period, being this profitability of

-0,19% in the year 2005.

The company’s Net Result decreased in 84,98% between 2004 and 2005.

This evolution, compared to the EBIT’s performance, implies that the

financial and extraordinary activities have had a positive effect in the

company’s Financial Profitability.

The result of these variations is a reduction of the company’s

profitability of 85,20% in the analysed period, being equal to 1,51% in the

year 2005.

The company’s sales figure grew 173,00% between 2005 and 2006.

The company’s EBIT grew 2.451,90% between 2005 and 2006.

This evolution implies an increase in the company’s operating

profitability.

The result of these variations is an increase of the company’s Economic

Profitability of 2.280,83% in the analysed period, being this profitability of

4,22% in the year 2006.

The company’s Net Result grew 7,90% between 2005 and 2006.

This evolution, compared to the EBIT’s performance, implies that the

financial and extraordinary activities have had a negative effect in the

company’s Financial Profitability.

The result of these variations is an increase of the company’s Economic

Profitability of 6,17% in the analysed period, being equal to 1,60% in the year

2006.

ANNUAL FINANCIAL REPORT

ADDITIONAL DATA

Source: annual financial report 2006

Results Distribution

Figures given in €

|

DISTRIBUTION

BASE |

DISTRIBUTION TO |

||

|

Profit and Loss |

914,13 |

Retained earnings |

91,41 |

|

Carry Over |

0,00 |

Voluntary Reserve |

822,72 |

|

Voluntary reserves |

0,00 |

Prior years losses |

0,00 |

|

Reserves |

0,00 |

Carry Over |

0,00 |

|

Other concepts |

0,00 |

Other funds |

0,00 |

|

Total of Amounts to be distributed |

914,13 |

Dividends |

0,00 |

|

|

|

Other Applications |

0,00 |

COMPARATIVE SECTOR ANALYSIS

Values table

Figures expressed in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

BALANCE SHEET ANALYSIS: % on the total

assets |

|

|

|

|

|

|

|

|

|

|

OWN FUNDS |

84,53 |

36,42 |

48,11 |

132,08 |

|

|

|

|

|

|

DEBT |

15,47 |

63,58 |

-48,11 |

-75,67 |

|

|

|

|

|

|

FIXED ASSETS |

0,41 |

34,52 |

-34,12 |

-98,81 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

PROFIT AND LOSS ACCOUNT ANALYSIS: % on the total

operating income |

|

|

|

|

|

|

|

|

|

|

SALES |

100,00 |

98,56 |

1,44 |

1,47 |

|

|

|

|

|

|

ADDED VALUE |

5,44 |

22,31 |

-16,88 |

-75,64 |

|

|

|

|

|

|

EBIT |

4,21 |

3,35 |

0,86 |

25,67 |

|

|

|

|

|

|

NET RESULT |

1,35 |

2,20 |

-0,85 |

-38,66 |

|

|

|

|

|

Sector Composition

Compared sector (NACE): 524

Number of companies: 14770

Size (Sales Figure) : 0 - 2.800.000,00

Euros

Comments on the

sectorial comparative

Compared to its sector the assets of the companies show an inferior

proportion of fixed assets. Specifically the difference with the sector average

is -34,12% , which means a relative difference of -98,81% .

In liabilities composition the company appeals on a wider scale to self

financing, being the proportion of net worth of 48,11% superior, which means a

relative difference of 132,08% . As a consequence, external financing sources

are less used by the company in 48,11% less than the sector, which means a

difference of 75,67% .

The proportion that the sales mean to the company’s total ordinary

income is 100,00%, 1,44% higher than in the sector, which means a relative

difference of 1,47% .

The company’s EBIT was positive and was 4,21% with regard to the total

ordinary income, 0,86% higher than in the sector, which means a relative

difference of 25,67% .

The company’s capacity to generate operating income is higher than the

one of the sector as its ratio EBIT/Sales is higher (ES Company versus ES

Sector).

The company’s net result was positive and equal to 1,35% with regard to

the total ordinary income, 0,85% less than the sector, which means a relative

difference of 38,66% .

The financial and extraordinary results and the tax impact have had a

negative impact on the Net result in the company with a worse behaviour than in

the sector; as a consequence, the company shows a worse Net Result/EBIT ratio

(REBEmpresa vs. REBSector).

ADDRESSES

Current Legal Seat Address:

STREET OURENSE, 59

27004

LUGO

CORPORATE STRUCTURE

ADMINISTRATIVE LINKS

Main Board members,

Directors and Auditor ![]()

|

POSITION |

SURNAMES AND

NAME |

APPOINTMENT DATE |

|

ADMINISTRATOR |

DE MATOS CARRASCO FRANCISCO JOSE |

20/02/2004 |

|

ADMINISTRATOR |

DE MATOS CARRASCO ANA MARIA |

20/02/2004 |

|

ADMINISTRATOR |

CARRASCO DONAIRE MANUELA |

20/02/2004 |

CREDIT INFORMATION

Constitution Date: 19/05/1999

Business activity

Activity: Retail sale in specialized stores

NACE Code: 5248

NACE Activity: Other retail sale

in specialized stores

Business: LA VENTA, ALQUILER

Y DISTRIBUCION DE PRODUCTOS RELATIVOS A LA MINERIA Y CONSTRUCCION.

Employees

Number of total employees: 1 (2004)

Number of fixed employees: 100,00%

Number of temporary employees: 0,00%

LEGAL STRUCTURE

Constitution Data

Register Date: 19/05/1999

Register town: Lugo

Announcement number: 402313

Legal form: LIMITED LIABILITY

COMPANY

Social Capital: 36.061 €

Current structure data

Current Legal Form: LIMITED LIABILITY

COMPANY

Current Capital: 36.061,00 €

Legal Aspects

Obligation to fill in Financial

Statements: YES

Chamber census: YES (2006)

Listed on a Stock Exchange: NO

B.O.R.M.E.(Official Companies

Registry Gazette)

Registered Proceedings

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Resignations |

20/02/2004 |

91697 |

Lugo |

Other Proceedings published

|

PROCEEDINGS |

DATE |

NOTICE NUM. |

TRADE REG. |

|

Registration of accounts (2006) Individual |

14/08/2007 |

277640 |

Lugo |

|

Registration of accounts (2005) Individual |

11/10/2006 |

710042 |

Lugo |

|

Registration of accounts (2004) Individual |

13/09/2005 |

383889 |

Lugo |

|

Registration of accounts (2003) Individual |

31/08/2004 |

286371 |

Lugo |

FINANCIAL INFORMATION

The information on the last account contained in this report is

extracted from the Mercantile Register file of the legal address of the Company

and dated 08/10/2007.

BALANCE SHEET

Assets

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

A) DUE FROM SHAREHOLDERS FOR UNCALLED CAPITAL |

|

|

|

|

B) FIXED ASSETS |

36.803,67 |

1.106,67 |

276,67 |

|

I. Incorporation costs |

|

|

|

|

II. Intangible fixed assets |

|

|

|

|

III. Tangible fixed assets |

1.936,67 |

1.106,67 |

276,67 |

|

IV. Financial fixed assets |

34.867,00 |

|

|

|

V.Owners equity |

|

|

|

|

VI.Long term trade liabilities |

|

|

|

|

C) DEFERRED EXPENSES |

|

|

|

|

D) CURRENT ASSETS |

41.748,50 |

61.528,20 |

67.267,49 |

|

I. Shareholders by required outlays |

|

|

|

|

II. Stocks |

3.410,20 |

1.297,32 |

2.301,87 |

|

III. Debtors |

22.073,52 |

39.450,47 |

46.195,40 |

|

IV. Temporary financial investment |

|

|

|

|

V. Short-term own shares |

|

|

|

|

VI. Treasury |

16.264,78 |

20.780,41 |

18.770,22 |

|

VII. Periodification adjustments |

|

|

|

|

ASSETS (A + B + C + D) |

78.552,17 |

62.634,87 |

67.544,16 |

Assets composition

Liabilities

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

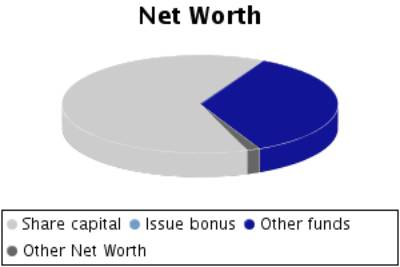

A) SHAREHOLDERS EQUITY |

55.334,39 |

56.181,87 |

57.096,00 |

|

I. Share capital |

36.060,73 |

36.061,00 |

36.061,00 |

|

II. Issue bonus |

|

|

|

|

III.Revaluation reserve |

|

|

|

|

IV.Reserves |

17.293,75 |

19.273,66 |

20.120,87 |

|

Capital adjustments in Euros |

|

|

|

|

Sundry reserves |

17.293,75 |

19.273,66 |

20.120,87 |

|

V.Results from previous years |

-3.659,56 |

|

|

|

VI.Profit and Losses |

5.639,47 |

847,21 |

914,13 |

|

VII.Dividend paid during the year |

|

|

|

|

VIII.Own shares for capital reduction |

|

|

|

|

B) DEFERRED INCOME |

|

|

|

|

C) PROVISIONS FOR LIABILITIES AND EXPENSES |

|

|

|

|

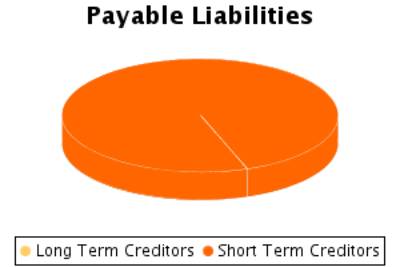

D) LONG TERM LIABILITIES |

|

|

|

|

E) SHORT TERM LIABILITIES |

23.217,78 |

6.453,00 |

10.448,16 |

|

F) SHORT TERM PROVISIONS FOR LIABILITIES AND

EXPENSES |

|

|

|

|

LIABILITIES (A + B + C + D + E + F) |

78.552,17 |

62.634,87 |

67.544,16 |

Liabilities

Composition

PROFIT AND LOSS ACCOUNT

Itams of the Profit

and Loss Account

Figures given in €

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

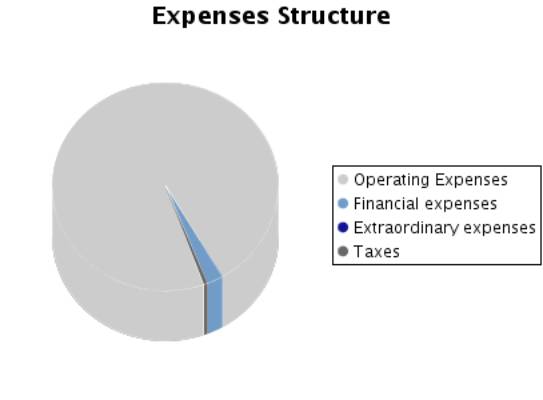

A) EXPENSES (A.1 a A.15) |

24.711,27 |

25.741,48 |

66.789,92 |

|

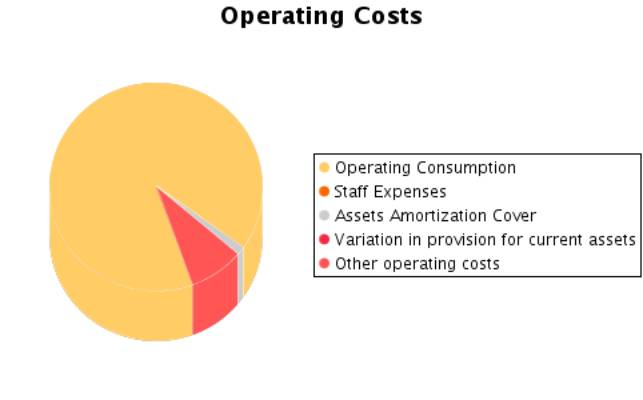

A.1.Operating costs |

5.964,30 |

19.552,88 |

58.626,75 |

|

A.2. Labour cost |

7.701,32 |

|

|

|

Wages |

5.000,00 |

|

|

|

Social security expenses |

2.701,32 |

|

|

|

A.3. Assets depreciation |

830,00 |

830,00 |

830,00 |

|

A.4. Variation in provision for current assets |

|

|

|

|

A.5. Other operating costs |

7.100,47 |

4.538,31 |

5.397,03 |

|

A.I. OPERATING RESULT (B.1-A.1-A.2-A.3-A.4-A.5) |

8.687,51 |

|

2.850,27 |

|

A.6.Financial expenses and similar |

2.266,65 |

457,20 |

1.544,37 |

|

Debts with related companies |

|

|

|

|

Debts with associated companies |

|

|

|

|

By debts with third parties and similar expenses |

2.266,65 |

457,20 |

1.544,37 |

|

Losses from financial investments |

|

|

|

|

A.7. Variation in financial investment provision |

|

|

|

|

A.8.Negative exchange difference |

|

|

|

|

A.II.POSITIVE FINANCIAL RESULTS

(B.2+B.3-A.6-A.7-A.8) |

|

1.331,49 |

|

|

A.III.PROFIT FROM ORDINARY ACTIVITIES

(A.I+A.II-B.I-B.II) |

6.488,00 |

1.210,30 |

1.305,90 |

|

A.9. Variation in provision in fixed assets |

|

|

|

|

A.10. Losses in fixed assets |

|

|

|

|

A.11. Losses from own shares and bonds |

|

|

|

|

A.12. Extraordinary charges |

|

|

|

|

A.13.Other exercises’ expenses and losses |

|

|

|

|

A.IV.POSITIVE EXTRAORDINARY RESULT (B.4+B.5+B.6+B.7+B.8-A.9-A.10-A.11-A.12-A.13) |

|

|

|

|

A.V.PROFIT BEFORE TAXES (A.III+A.IV-B.III-B.IV) |

6.488,00 |

1.210,30 |

1.305,90 |

|

A.14.Corporate Taxes |

848,53 |

363,09 |

391,77 |

|

A.15. Other taxes |

|

|

|

|

A.VI.EXERCISE RESULT (PROFIT) (A.V-A.14-A.15) |

5.639,47 |

847,21 |

914,13 |

|

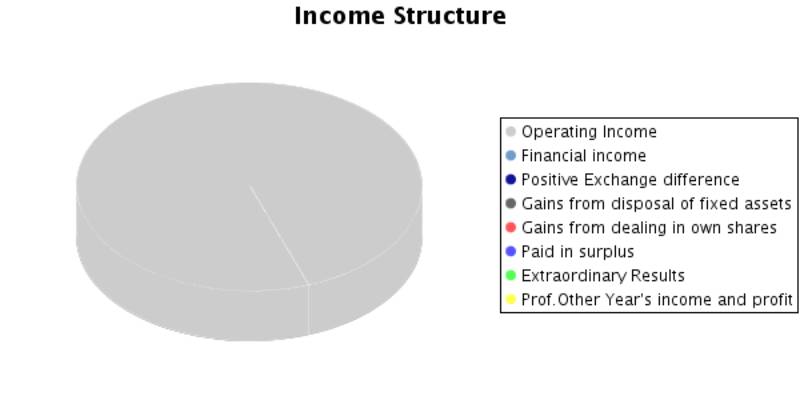

B) INCOMES (B.1 a B.8) |

30.350,74 |

26.588,69 |

67.704,05 |

|

B.1.Operating income |

30.283,60 |

24.800,00 |

67.704,05 |

|

Turnover |

30.283,60 |

24.800,00 |

67.704,05 |

|

Other operating income |

|

|

|

|

B.I.OPERATING LOSSES (A.1+A.2+A.3+A.4+A.5-B.1) |

|

121,19 |

|

|

B.2.Financial Income |

67,14 |

1.788,69 |

|

|

From affiliated companies |

|

|

|

|

From associated companies |

|

|

|

|

Other |

67,14 |

1.788,69 |

|

|

Gains from investments |

|

|

|

|

B.3. Positive change difference |

|

|

|

|

B.II. NEGATIVE FINANCIAL RESULTS

(A.6+A.7+A.8-B.2-B.3) |

2.199,51 |

|

1.544,37 |

|

B.III.LOSSES FROM ORDINARY ACTIVITIES

(B.I+B.II-A.I-A.II) |

|

|

|

|

B.4.B.9. Gains from disposal of fixed assets |

|

|

|

|

B.5.Gains from dealing in own shares |

|

|

|

|

B.6. Paid in surplus |

|

|

|

|

B.7. Extraordinary income |

|

|

|

|

B.8.Other year’s income and profits |

|

|

|

|

B.IV.NEGATIVE EXTRAORDINARY LOSSES

(A.9+A.10+A.11+A.12+A.13-B.4-B.5-B.6-B.7-B.8) |

|

|

|

|

B.V.LOSS BEFORE TAXES (B.III+B.IV-A.III-A.IV) |

|

|

|

|

B.VI.EXERCISE RESULTS (LOSS) (B.V+A.14+A.15) |

|

|

|

Composition of the

Profit and Loss Account

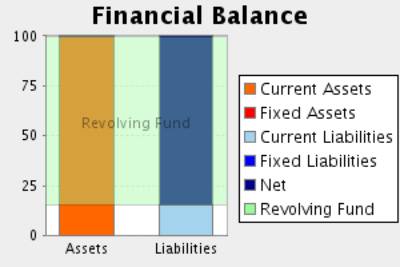

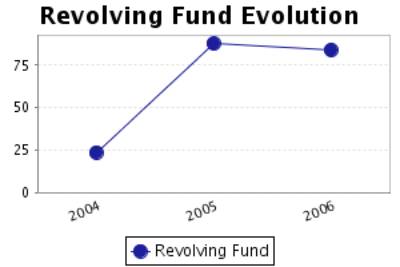

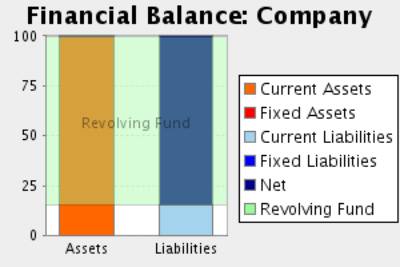

FINANCIAL BALANCE

Here the Main Capital Amounts of the company and the Revolving Fund

Evolution are analysed.

Financial Balance

Table

Figures given in €

|

|

31/12/2004 (12) |

% |

31/12/2005 (12) |

% |

31/12/2006 (12) |

% |

|

A) DUE FROM SHAREHOLDERS FOR UNCALLED CAPITAL |

|

|

|

|

|

|

|

B) FIXED ASSETS |

36.803,67 |

46,85 |

1.106,67 |

1,77 |

276,67 |

0,41 |

|

C) DEFERRED EXPENSES |

|

|

|

|

|

|

|

D) CURRENT ASSETS |

41.748,50 |

53,15 |

61.528,20 |

98,23 |

67.267,49 |

99,59 |

|

ASSETS (A + B + C + D) |

78.552,17 |

|

62.634,87 |

|

67.544,16 |

|

|

|

||||||

|

A) SHAREHOLDERS EQUITY |

55.334,39 |

70,44 |

56.181,87 |

89,70 |

57.096,00 |

84,53 |

|

B) DEFERRED INCOME |

|

|

|

|

|

|

|

C) PROVISIONS FOR LIABILITIES AND EXPENSES |

|

|

|

|

|

|

|

D) LONG TERM LIABILITIES |

|

|

|

|

|

|

|

E) SHORT TERM LIABILITIES |

23.217,78 |

29,56 |

6.453,00 |

10,30 |

10.448,16 |

15,47 |

|

F) SHORT TERM PROVISIONS FOR LIABILITIES AND EXPENSES |

|

|

|

|

|

|

|

LIABILITIES (A + B + C + D + E + F) |

78.552,17 |

|

62.634,87 |

|

67.544,16 |

|

Financial Balance

Composition

Comments on Financial

Balance

In the 2004, the assets of the company were formed in 46,85% of Fixed

Assets and in 53,15% of Current Assets.This assets were financed in 70,44% with

own capitals and in 29,56% with current liabilities.

The result of this financial structure is a positive turnover fund of

18.530,72 Euros, which is equivalent to 23,59% proportion of the

company’s total assets.

In the 2005, the assets of the company were formed in 1,77% of Fixed

Assets and in 98,23% of Current Assets.This assets were financed in 89,70% with

own capitals and in 10,30% with current liabilities.

The result of this financial structure is a positive turnover fund of

55.075,20 Euros, which is equivalent to 87,93% proportion of the

company’s total assets.

This measure has increased with respect to the previous exercise in

197,21% having also increased its proportion with respect to the total assets

of the company.

In the 2006, the assets of the company were formed in 0,41% of Fixed

Assets and in 99,59% of Current Assets.This assets were financed in 84,53% with

own capitals and in 15,47% with current liabilities.

The result of this financial structure is a positive turnover fund of

56.819,33 Euros, which is equivalent to 84,12% proportion of the company’s

total assets.

This measure has increased with respect to the previous exercise in

3,17% having, however, diminished its proportion with respect to the total

assets of the company.

RATIOS

Main Ratios

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

STRUCTURAL RATIOS |

|

|

|

|

Management fund |

18.530,72 |

55.075,20 |

56.819,33 |

|

Indebtedness (%) |

29,56 |

10,30 |

15,47 |

|

External Funds on Net Worth |

0,42 |

0,12 |

0,18 |

|

GENERAL ACTIVITY RATIO |

|

|

|

|

Turnover Increase (%) |

-73,76 |

-18,11 |

173,00 |

|

Added value growth (%) |

143,17 |

-95,88 |

419,22 |

|

Cash Flow |

6.469,47 |

1.677,21 |

1.744,13 |

|

Labour Productivity |

2,24 |

|

|

|

Assets turnover |

0,39 |

0,40 |

1,00 |

|

Breakdown Point |

19.465,48 |

25.372,79 |

46.445,00 |

|

Security Margin of the Breakdown Point (%) |

35,72 |

-2,31 |

31,40 |

|

ACTIVITY RATIOS |

|

|

|

|

Average Collection Period |

262 |

573 |

246 |

|

Inventory Turnover Period |

41 |

19 |

12 |

|

SOLVENCY RATIOS |

|

|

|

|

Payback Capacity |

0,28 |

0,26 |

0,17 |

|

Assets Guarantee |

3,38 |

9,71 |

6,46 |

|

Short Term Debts Proportion (%) |

100,00 |

100,00 |

100,00 |

|

Interest Coverage |

2,82 |

-0,24 |

1,13 |

|

LIQUIDITY RATIOS |

|

|

|

|

Current Ratio |

1,80 |

9,54 |

6,44 |

|

Immediate liquidity |

0,70 |

3,22 |

1,80 |

|

Sales on Current Assets |

261 |

145 |

362 |

Results Analysis

Ratios

|

|

31/12/2004 (12) |

31/12/2005 (12) |

31/12/2006 (12) |

|

Economic profitability (%) |

11,06 |

-0,19 |

4,22 |

|

Operating Profitability (%) |

28,69 |

-0,49 |

4,21 |

|

Equity gearing |

1,06 |

-11,13 |

0,54 |

|

Financial profitability (%) |

10,19 |

1,51 |

1,60 |

|

General Profitability (%) |

18,62 |

3,42 |

1,35 |

Comments on the

Results Analysis Ratios

The economic profitability in the year2005The economic profitability in

the year -0,19%, derived from a negative operating profitability of -0,49%.The

assets turnover was 0,40%.

The economic profitability in the year from a positive level of 11,06% to

its current negative level. This evolution is due to the obtaining of a

negative operating profitability of -0,49% in comparison with the current

positive value of 28,69%. Assets turnover has maintained stable in this period,

with an index of 0,40%.

Financial profitability on 2005 achieved a 1,51%.

The company’s financial structure has favoured its profitability with an

indebtedness level of -11,13.

The general profitability on 2005 achieved a 3,42%.

The economic profitability in the year2006 achieved a 4,22% positive

level, due to a 4,21% economic margin and to an assets turnover of1,00%.

The economic profitability in the year has passed from a negative level

of -0,19% to its positive current value. This evolution is due to the obtaining

of positive operating profitability of 4,21% in comparison with the previous

negative level of -0,49%. Assets turnover has maintained stable in this period,

with an index of 1,00%.

Financial profitability on 2006 achieved a 1,60%.

The company’s financial structure has limited its profitability with an

indebtedness level of 0,54.

The general profitability on 2006 achieved a 1,35%.

SECTORIAL ANÁLYSIS

Large Capital Amounts

and Financial Balance

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

A) DUE FROM

SHAREHOLDERS FOR UNCALLED CAPITAL |

|

0,09 |

|

|

|

|

|

|

|

|

B) FIXED ASSETS |

0,41 |

34,52 |

-34,12 |

-98,81 |

|

|

|

|

|

|

C) DEFERRED

EXPENSES |

|

0,44 |

|

|

|

|

|

|

|

|

D) CURRENT

ASSETS |

99,59 |

64,94 |

34,65 |

53,35 |

|

|

|

|

|

|

ASSETS (A + B +

C + D) |

100 |

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

A) SHAREHOLDERS

EQUITY |

84,53 |

36,15 |

48,38 |

133,85 |

|

|

|

|

|

|

B) DEFERRED INCOME |

|

0,28 |

|

|

|

|

|

|

|

|

C) PROVISIONS

FOR LIABILITIES AND EXPENSES |

|

0,08 |

|

|

|

|

|

|

|

|

D) LONG TERM

LIABILITIES |

|

16,22 |

|

|

|

|

|

|

|

|

E) SHORT TERM

LIABILITIES |

15,47 |

47,24 |

-31,77 |

-67,25 |

|

|

|

|

|

|

F) SHORT TERM

PROVISIONS FOR LIABILITIES AND EXPENSES |

|

0,03 |

|

|

|

|

|

|

|

|

LIABILITIES (A + B + C + D + E + F) |

100 |

100 |

|

|

|

|

|

|

|

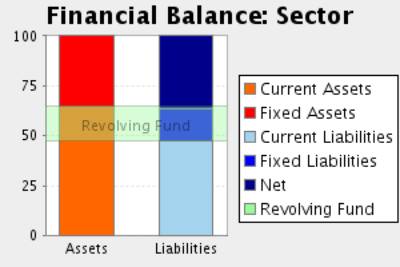

Financial Balance Composition

Comments to the

Sectorial Analysis

In the 2006, the assets of the company were formed in 0,41% of fixed

assets and in 99,59Current Assets % In the sector, the proportion of fixed

assets was of 35,06%, 98,83% superior, and the proportion of current assets was

of 64,94%, 53,35% inferior.

The assets were financed in the company in 84,53% with own capitals and

in 15,47% with current liabilities In the sector, the self financing

represented 36,42%, 132,08% inferior. On the other hand the long term debts

represented in the sector an average of 47,27% financing, with a relative

difference of 67,28% favourable to the sector

The result of this company’s financial structure is a turnover fund that

represents 84,12% of the total assets; in the sector, this same proportion is

17,67%, therefore, we can say that the company’s turnover fund is 376,06%

higher than the one in of the sector.

Analytical Account of Results

Figures given in %

|

|

COMPANY (2006) |

SECTOR |

DIFFERENCE |

DIFFERENCE RELATIVE |

|

Turnover |

100,00 |

98,56 |

1,44 |

1,47 |

|

Other operating income |

|

1,44 |

|

|

|

Production Value |

100,00 |

100,00 |

0,00 |

0,00 |

|

Operating expenses |

86,59 |

65,98 |

20,61 |

31,23 |

|

Other operation expenses |

7,97 |

11,71 |

-3,74 |

-31,92 |

|

Added value |

5,44 |

22,31 |

-16,87 |

-75,62 |

|

Labour cost |

|

16,94 |

|

|

|

Gross Economic Result |

5,44 |

5,38 |

0,06 |

1,19 |

|

Assets depreciation |

1,23 |

1,95 |

-0,72 |

-36,79 |

|

Variation in provision for current assets and bad debt losses |

|

0,08 |

|

|

|

Net Economic Result |

4,21 |

3,35 |

0,86 |

25,67 |

|

Financial income |

|

0,27 |

|

|

|

Financial Charges |

2,28 |

1,02 |

1,26 |

122,66 |

|

Variation in financial investment provision |

|

-0,01 |

|

|

|

Ordinary

Activities Result |

1,93 |

2,60 |

-0,68 |

-25,91 |

|

Extraordinary income |

|

0,65 |

|

|

|

Extraordinary charges |

|

0,18 |

|

|

|

Variation in provision in fixed assets |

|

0,00 |

|

|

|

Results before Taxes |

1,93 |

3,07 |

-1,14 |

-37,11 |

|

Corporate taxes |

0,58 |

0,87 |

-0,29 |

-33,18 |

|

Net Result |

1,35 |

2,20 |

-0,85 |

-38,66 |

|

Assets depreciation |

1,23 |

1,95 |

-0,72 |

-36,79 |

|

Change of Provisions |

|

0,08 |

|

|

|

Net Self-Financing |

2,58 |

4,22 |

-1,64 |

-38,89 |

Main Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

STRUCTURAL RATIOS |

|

|

|

|

|

Management fund |

56.819,33 |

2,39 |

38,76 |

122,00 |

|

Indebtedness (%) |

15,47 |

51,81 |

72,24 |

85,56 |

|

External Funds on Net Worth |

0,18 |

1,08 |

2,60 |

5,92 |

|

GENERAL ACTIVITY RATIO |

|

|

|

|

|

Turnover Increase (%) |

173,00 |

-7,40 |

2,02 |

12,48 |

|

Added value growth (%) |

419,22 |

-6,86 |

3,92 |

16,01 |

|

Cash Flow |

1.744,13 |

5,65 |

14,32 |

33,59 |

|

Assets turnover |

1,00 |

0,99 |

1,54 |

2,25 |

|

Breakdown Point |

46.445,00 |

212.942,14 |

423.543,09 |

825.409,54 |

|

Security Margin of the Breakdown Point (%) |

31,40 |

3,20 |

7,60 |

14,15 |

|

ACTIVITY RATIOS |

|

|

|

|

|

Average Collection Period |

246 |

4 |

25 |

69 |

|

Inventory Turnover Period |

12 |

31 |

75 |

147 |

|

SOLVENCY RATIOS |

|

|

|

|

|

Payback Capacity |

0,17 |

0,04 |

0,07 |

0,15 |

|

Assets Guarantee |

6,46 |

1,16 |

1,37 |

1,92 |

|

Short Term Debts Proportion (%) |

100,00 |

67,13 |

92,30 |

100,00 |

|

Interest Coverage |

1,13 |

1,28 |

3,91 |

12,88 |

|

LIQUIDITY RATIOS |

|

|

|

|

|

Current Ratio |

6,44 |

1,02 |

1,30 |

1,92 |

|

Immediate liquidity |

1,80 |

0,04 |

0,17 |

0,50 |

|

Sales on Current Assets |

362 |

525 |

811 |

1.192 |

Results Analysis

Ratios

|

|

COMPANY (2006) |

PTILE25 |

PTILE50 |

PTILE75 |

|

Economic profitability (%) |

4,22 |

1,59 |

3,77 |

7,18 |

|

Operating Profitability (%) |

4,21 |

1,04 |

2,50 |

4,84 |

|

Equity gearing |

0,54 |

1,42 |

2,40 |

4,58 |

|

Financial profitability (%) |

1,60 |

2,81 |

7,77 |

16,55 |

|

General Profitability (%) |

1,35 |

0,47 |

1,24 |

2,82 |

NOTES

BLOQUE DE INVESTIGACION:

- Tfno. movil de contacto: 609102020.

ABOUT YOUR REQUEST:

Contacted by telephone on the 982231002,

property of consultant’s office of the subject, which only confirms the registered address (

in Porriño, Pontevedra), and refuses to provide us with further information. In

spite of investigations using every source available (public and private), no

additional details than those contained in this report are available. .

ADDITIONA

RATING

EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit

consideration. Capability to overcome financial difficulties seems

comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)