![]()

MIRA

INFORM REPORT

|

Report Date : |

09.09.2008 |

IDENTIFICATION

DETAILS

|

Name : |

LUMWANA MINING CO LTD |

|

|

|

|

Registered Office : |

P O Box 110199, Solwezi |

|

|

|

|

Country : |

Zambia |

|

|

|

|

Financials (as on) : |

31.12.2007 |

|

|

|

|

Date of Incorporation : |

20.9.1992 |

|

|

|

|

Legal Form : |

Limited Liability Company, Limited by Shares |

|

|

|

|

Line of Business : |

Mining of Copper |

RATING &

COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Maximum Credit Limit : |

USD 250,000 |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

COMPANY REPORTED

LUMWANA MINING CO LTD

Principal Address

P O Box 110199, Solwezi, Zambia

Telephone: +260-21-8240023

Fax:+260-21-1257642

Email: None

Internet: None

Established

20/9/1992

Registration

No. Lusaka Zambia

Legal Form

Limited Liability

Company, Limited by shares

Stock Listing

Not Listed

Workforce

2007

600

Office & Factories

Head offices Anglo

American Building, 74 Independence Avenue, Cathedral Hill,

Branches Mwinilunga Road via Solwezi, Zambia

Company Profile

Paid in Capital ZMK. 100,000,000

Subscribed Capital ZMK. 100,000,000

Shareholders

Name Position Amount

Ratio

Mr. Craig Williams

CEO

Mr. Nathan

Chishimba Director

Mr. Michael

Klessens Director

Equinox Copper

Ventures Ltd Holding Co. 100.00%

Total 100.00%

Credit Opinion

Our proposed credit amount of USD 250,000 is recommendable

Affiliated Companies

Company (1) Chambishi Copper Smelter Limited

Management/ Directors

President/ CEO (1)

Name Mr. Craig Williams

Remarks Top

Decision Maker

President/ CEO (2)

Name Mr. Nathan Chishimba

Þ Top decision maker is the person who has the

ultimate authority or power to make important managerial decisions. He/She may

or may not be officially registered as a president or an executive director.

Business Activities

Mining of Copper

Terms of payment

Buying terms 30% in cash, 70% on credit

Selling terms 50% in cash, 50% on credit

Suppliers

Euclid,

Customers

Group company

Recent Sales

Attached

Exports

None

Export Ratio

0.0%

Import Ratio

60.0%

Domestic Market Share

20.0%

Banking relationship

Main Banks Stanbic Bank

Credit Check of Subject,

President & CEO (as of report date)

Payment Morale: In the documents at our disposal nothing adverse has been shown

so far.

CREDIT RATING: Financial situation is

average.

COMMENTS

Maximum credit we recommend is USD 250,000 outstanding at any one time.

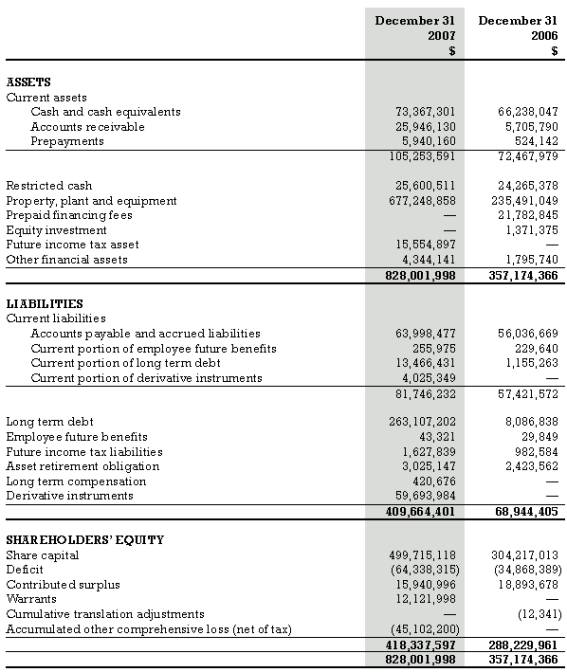

CONSOLIDATED BALANCE SHEET

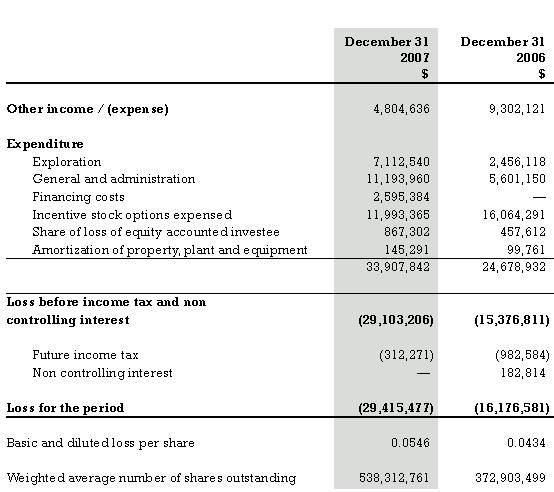

CONSOLIDATED INCOME STATEMENT

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.44.89 |

|

UK Pound |

1 |

Rs.78.86 |

|

Euro |

1 |

Rs.63.33 |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit

consideration. Capability to overcome financial difficulties seems

comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|

This score serves as a reference to

assess SC’s credit risk and to set the amount of credit to be extended. It is

calculated from a composite of weighted scores obtained from each of the major

sections of this report. The assessed factors and their relative weights (as

indicated through %) are as follows:

Financial condition (40%) Ownership background (20%) Payment

record (10%)

Credit history (10%) Market trend (10%) Operational

size (10%)