![]()

MIRA

INFORM REPORT

|

Report Date : |

10.09.2008 |

IDENTIFICATION

DETAILS

|

Name : |

BASS PREMIER CO |

|

|

|

|

Registered Office : |

63-66 Hatton Garden London Ec1n

8le |

|

|

|

|

Country : |

United Kingdom |

|

|

|

|

Legal Form : |

Partnership. |

|

|

|

|

Line of Business : |

Jewellery, Watch and Precious Stone |

RATING &

COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

name of the company

BASS PREMIER CO

Legal Events

Number of Court Judgments 0

Value of all Court Judgments 0

Number of Mortgages and Charges 0

Associations

Parent Company No

Number of Principals 2

Identification

Main Trading Address 63-66 HATTON GARDEN

LONDON

EC1N 8LE

UNITED KINGDOM

Telephone Number 020-7242-2278

Fax Number 020-7831-1555

ID Number 23-740-0411

Line of Business (SIC) JEWELLERY, WATCH

& PRECIOUS STONE WHLRS (5094)

Payment Information

Collects in excess

of 100 million payment experiences on European businesses each year. The

information shown below indicates how BASS PREMIER CO has been

paying its bills.

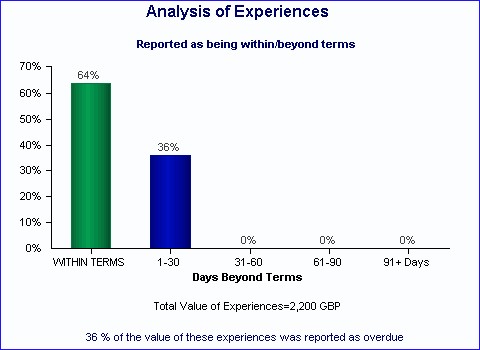

Average Days Beyond Terms 9

Paydex 74

Payment Experiences Summary

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

In some instances, payment beyond terms can be the result of

overlooked or disputed invoices |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

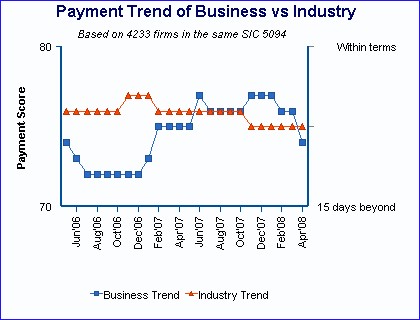

Payment Industry Comparison

|

|

|

|||||||||||||||||||||||||

|

|

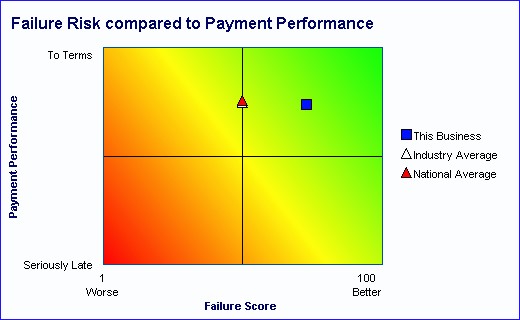

Risk of Failure

and Payment Performance - Industry Sector Comparison

Commentary

BASS PREMIER CO pays it's bills on average 9 days beyond terms.

This is 3 days longer than the national average of 6 days beyond terms.

When compared to similar businesses BASS PREMIER CO pays slower than the

industry average of 8 days beyond terms.

The failure score of 73 predicts

that the risk of failure within the next 12 months for BASS PREMIER CO is

better than average.

This compares to an industry average

Failure Score this month of 50 and a national average of 50.

|

Public Notice information is added to the Database and, if present, will appear in this section.

Number of registered charges: 0

|

To gain additional insight into the principal(s) of this business, conduct a consumer credit search.

Mr Andrew

Bassalian, Partner

No other current associations

Mr Alex Bassalian,

Partner

No other current associations

Legal Structure

Legal Form Partnership.

Business started as Old

established business

Operations

|

||||||||

|

|

||||||||

|

|

||||||||

|

||||||||

|

|

FOREIGN EXCHANGE

RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.45.12 |

|

UK Pound |

1 |

Rs.79.60 |

|

Euro |

1 |

Rs.63.83 |

RATING

EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Unfavourable & favourable factors carry similar weight in credit consideration.

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

NR |

In view of the lack of information, we have no basis upon which to

recommend credit dealings |

No Rating |

|

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a

composite of weighted scores obtained from each of the major sections of this

report. The assessed factors and their relative weights (as indicated through

%) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)