![]()

MIRA INFORM REPORT

|

Report Date : |

16.08.2011 |

IDENTIFICATION DETAILS

|

Name : |

GLASIMPORT KWINTSHEUL B.V. |

|

|

|

|

Registered Office : |

Bovendijk 35, 2295RV Kwintsheul |

|

|

|

|

Country : |

Netherlands |

|

|

|

|

Financials (as on) : |

31.12.2010 |

|

|

|

|

Date of Incorporation : |

13.05.1991 |

|

|

|

|

Com. Reg. No.: |

27231634 |

|

|

|

|

Legal Form : |

Limited Company |

|

|

|

|

Line of Business : |

Wholesale of flat glass |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Maximum Credit Limit : |

€ 50.000 |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment

Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31st, 2011

|

Country Name |

Previous Rating (31.12.2010) |

Current Rating (31.03.2011) |

|

Netherlands |

a2 |

a2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

CONTACT

INFORMATION

|

Company name |

Glasimport

Kwintsheul B.V. |

|

Tradename |

Glasimport Kwintsheul

B.V. |

|

Address |

Bovendijk 35 |

|

|

2295RV Kwintsheul |

|

|

Netherlands |

|

Mail address |

Postbus 4 |

|

|

2290AA Wateringen |

|

|

Netherlands |

|

Telephone number |

0174294340 |

|

Telefax number |

0174297120 |

|

E-mail address |

|

|

Website |

|

|

VAT number |

800922323 |

CREDIT LIMIT

Credit limit A credit of € 50.000 may be

granted Normal

COMPANY INFORMATION

Handelsregisternummer 27231634

Registered in Chamber of commerce

Den Haag

First registration 13-05-1991

Act of foundation 07-05-1991

Date of constitution 01-01-1991

Legal form Besloten Vennootschap (Limited

Company)

Place of constitution Kwintsheul

Capital EUR 90.756,04

Issued capital EUR 18.151,21

Paid up capital EUR 18.151,21

|

NACE-code |

Wholesale of flat glass

(51533) |

|

SBI-code |

Wholesale of flat glass

(46734) |

|

Formal objective |

Groothandel in alle

soorten vlakglas. (Wholesale all kinds

of flat glass) |

|

Employees |

Total: 11 |

|

|

|

Employees according to

CoC |

Chamber of commerce: 9 |

|

|

|

Bookyear |

2010 |

2009 |

2008 |

|

Number |

11 |

12 |

10 |

|

Change |

-8,33% |

20,00% |

0,00% |

COMPANY STRUCTURE

|

Shareholder |

Sagridt B.V. |

|

|

Van Leeuwenhoekstraat 7 |

|

|

2811DW REEUWJK |

|

|

Netherlands |

|

|

KvK: 24401804 |

|

|

Active since: 30-07-2007 |

|

|

Percentage: 100.00% |

|

Ultimate parent company |

Futink B.V. |

|

|

Van Leeuwenhoekstraat 7 |

|

|

2811DW REEUWIJK |

|

|

KvK: 29024887 |

|

Holding company |

Sagridt B.V. |

|

|

Van Leeuwenhoekstraat 7 |

|

|

2811DW REEUWJK |

|

|

KvK: 24401804 |

|

Affiliated companies |

Hogla B.V. |

|

|

Van Leeuwenhoekstraat 7 |

|

|

2811DW REEUWIJK |

|

|

KvK: 29024651 |

|

|

Vetrad B.V. |

|

|

Van Leeuwenhoekstraat 7 |

|

|

2811DW REEUWIJK |

|

|

KvK: 29040646 |

Bankers ABN Amro Bankers NV ING Bankers NV

Rabobank Netherlands

Real estate Lease

The real estate is checked at the

land registration office Object code: WAINRINGEN C 5470 Owner: G.I.K.BEHEER

B.V.

MANAGEMENT

Management Sagridt B.V.

Van

Leeuwenhoekstraat 7

2811DW

REEUWIJK

Netherlands

KvK:

24401804

Authorization:

Fully authorized

Position:

Manager

Date

appointed: 30-07-2007

J.L.E.

Knetemann

Johann

Lucien Edwin

Authorization:

Fully authorized

Position:

Manager

Date

appointed: 01-09-2007

Date

of birth: 03-09-1970

J.

Klemann - Joosten Joyce

Authorization:

Fully authorized

Position:

Proxy

Date

appointed: 14-01-2009

Date

of birth: 23-07-1959

R.G.

Nelissen Robertus Gerardus

Authorization:

Limited authorization (max: € 0)

Position:

Proxy

Date

appointed: 20-06-1991

Date

of birth: 24-09-1954

PAYMENT INFORMATION

Payment experiences Payments are regular

Payments Based on multiple payment experiences up to €

7.500

Quarter: 4 2010: 56 Average days

Quarter: 1 2011: 61 Average days

Quarter: 2 2011: 61 Average days

Quarter: 3 2011: 30 Average days

|

|

invoices |

current quarter |

2011 Q2 |

2011 Q1 |

2010 Q4 |

|

|

Total |

58 |

100% |

10.070 |

11.934 |

13.482 |

13.767 |

|

Within terms |

33 |

100,0% |

10.070 |

6.445 |

4.129 |

3.827 |

|

Delayed 0 - 30 |

21 |

0,0% |

|

4.489 |

8.978 |

9.940 |

|

Delayed 31 - 60 |

|

|

|

|

|

|

|

Delayed 61 - 90 |

|

|

|

|

|

|

|

Delayed 91 - 120 |

2 |

0,0% |

|

400 |

150 |

|

|

Delayed 120+ days |

2 |

0,0% |

|

600 |

225 |

|

FINANCIAL INFORMATION

Publication financial statement Annual

accounts 2008 are published on 24-07-2009

|

|

Annual accounts 2007 are

published on 25-07-2008 |

|

|

Type of publication |

Corporate |

|

|

Publication |

Steady |

|

|

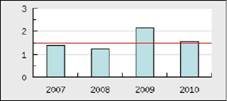

CORE FIGURES |

|

|

|

|

BOOKYEAR |

2010 |

2009 |

2008 |

|

Quick ratio |

0,60 |

1,63 |

0,80 |

|

Current ratio |

1,55 |

2,16 |

1,23 |

|

Nett workingcapital /

Balance total |

0,27 |

0,37 |

0,11 |

|

Capital and reserves /

Balance total |

0,45 |

0,55 |

0,35 |

|

Capital and reserves /

Fixed assets |

1,86 |

1,73 |

0,92 |

|

Solvency |

0,81 |

1,23 |

0,54 |

|

Nett workingcapital |

417.865 |

482.472 |

197.000 |

|

Capital and reserves |

694.633 |

726.848 |

604.000 |

|

Change capital and

reserves |

-4,43% |

20,34% |

39,81% |

|

change short term

liabilities |

82,09% |

-51,61% |

76,12% |

Annual accounts The company is obligated

to publish its annual accounts

Last annual accounts 2010

Tendency Changeable

Tendency

capital and reserves

Capital and reserves 2010 694.633

Total debt 2010 857.854

Current ratio 2010 1,55

Quick ratio 2010 0,60

Nett workingcapital 2010 417.865

Profitability Positive

Solvency Positive

Liquidity Positive

Current-

& Quickratio

BALANCE SHEET

|

BOOKYEAR |

2010 |

2009 |

2008 |

|

|

End of bookyear |

31-12-2010 |

31-12-2009 |

31-12-2008 |

|

|

Intangible assets |

20.000 |

|

3.000 |

|

|

Tangible assets |

178.768 |

166.376 |

203.000 |

|

|

Financial assets |

175.500 |

253.500 |

455.000 |

|

|

Fixed assets |

374.268 |

419.876 |

660.000 |

|

|

|

||||

|

Stocks and work in

progress |

723.444 |

217.768 |

371.000 |

|

|

Accounts receivable |

308.881 |

355.278 |

311.000 |

|

|

Liquid assets |

145.894 |

326.991 |

378.000 |

|

|

Current assets |

1.178.219 |

900.037 |

1.060.000 |

|

|

Total assets |

1.552.487 |

1.319.913 |

1.720.000 |

|

|

Capital and reserves |

694.633 |

726.848 |

604.000 |

|

|

other long term debts |

|

|

254.000 |

|

|

Long term liabilities |

97.500 |

175.500 |

254.000 |

|

|

Other short term debts |

|

|

863.000 |

|

|

Total short term debt |

760.354 |

417.565 |

863.000 |

|

|

Total debt |

857.854 |

593.065 |

1.116.000 |

|

|

Total Liabilities |

1.552.487 |

1.319.913 |

1.720.000 |

|

History

Management Since 14-01-2009 is Proxy Joyce Klemann-Joosten

appointed.

Company structure

Futink

B.V. (29024887)

Reeuwijk

Sagridt

B.V. (24401804)

Reeuwjk

Management Relation

Glasimport

Kwintsheul B.V. (27231634)

Kwintsheul

Subsidiary (100%)

Hogla

B.V. (29024651)

Reeuwijk

Subsidiary (100%)

Vetrad

B.V. (29040646)

Reeuwijk

Subsidiary (100%)

Lutimex

B.V. (29034442)

Reeuwijk

Subsidiary (100%)

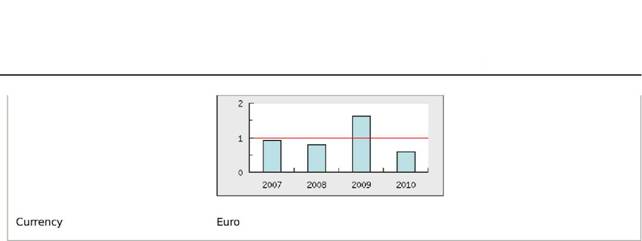

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.45.37 |

|

UK Pound |

1 |

Rs.73.53 |

|

Euro |

1 |

Rs.64.37 |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

---- |

NB |

New Business |

---- |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL) or

its officials.