![]()

MIRA INFORM

REPORT

|

Report Date : |

24.02.2011 |

IDENTIFICATION DETAILS

|

Name : |

FROCONSUR B.V. |

|

|

|

|

Registered Office : |

8911AX |

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.12.2009 |

|

|

|

|

Date of Incorporation : |

07.12.1986 |

|

|

|

|

Com. Reg. No.: |

01076844 |

|

|

|

|

Legal Form : |

Limited Company |

|

|

|

|

Line of Business : |

Wholesale of Fish |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Maximum Credit Limit : |

€ 100.000 |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment

Behaviour : |

Slow |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – June 30, 2010

|

Country Name |

Previous Rating (01.04.2010) |

Current Rating (30.06.2010) |

|

|

A1 |

A1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

CONTACTINFORMATION

|

Company name |

Froconsur B.V. |

|

Tradename |

Froconsur B.V. |

|

Address |

Willemskade 11 |

|

|

8911AX |

|

|

|

|

Mail address |

Postbus 3012 |

|

|

8901DA |

|

|

|

|

Telephone number |

0582160057 |

|

Telefax number |

0582160058 |

|

E-mail address |

|

|

Website |

CREDIT LIMIT

A credit of € 100.000 may be

granted

COMPANY INFORMATION

|

Handels Register Number |

01076844 |

|

Registered in |

Chamber of commerce

Noord-Netherlands |

|

First registration |

10-01-1997 |

|

Act of foundation |

19-12-1996 |

|

Date of constitution |

07-12-1989 |

|

Continuation date |

19-12-1996 |

|

Legal form |

Besloten Vennootschap (Limited Company) |

|

Place of constitution |

|

|

Capital |

EUR 226.890,11 |

|

Issued capital |

EUR 45.378,02 |

|

Paid up capital |

EUR 45.378,02 |

NACE-code Wholesale of fish (51382)

SBI-code Wholesale of fish (46382)

Formal

objective De im- en export van

levensmiddelen en diepvriesproducten.

Employees Total: 17

Bookyear 2011 2009 2008

Number 17 17 16

Change 0,00% 6,25% 33,33%

COMPANY STRUCTURE

Shareholder Froconsur Holding B.V.

Willemskade 11

8911AX

KvK: 01059154

Active since: 20-12-2007

Percentage: 100.00%

Holding company Froconsur Holding B.V.

Willemskade 11

8911AX

KvK: 01059154

Affiliated companies Froconsur Overseas B.V.

Oostergoweg 1

8911MA

KvK: 01069106

Latido Leeuwarden B.V.

Oostergoweg 1

8911MA

KvK: 01076845

Froconsur Logistics B.V.

Oostergoweg 1

8911MA

KvK: 01079666

Liability declaration Froconsur Holding B.V. (01059154)

Willemskade 11 8911AX

Bankers Rabobank

Hollandsche

Bankers-Unie NV

|

MANAGEMENT |

|

|

Management |

Froconsur Holding B.V. |

|

|

Willemskade 11 |

|

|

8911AX |

|

|

|

|

|

KvK: 01059154 |

|

|

Authorization: Fully authorized |

|

|

Position: Manager |

|

|

Date appointed: 19-12-1996 |

|

|

J.A. Boschma |

|

|

Josephina Annigjen |

|

|

Authorization: Limited

authorization |

|

|

Position: Proxy |

|

|

Date appointed: 01-01-2001 |

|

|

Date of birth: 31-03-1954 |

PAYMENT INFORMATION

Payment experiences Payments are slightly delayed

Payments Based on

multiple payment experiences up to € 50.000

Quarter: 22010: 132 Average days

Quarter: 3 2010: 43 Average days

Quarter: 4 2010: 53 Average days

Quarter: 1 2011: 53 Average days

|

|

invoices |

current quarter |

2010 Q4 |

2010 Q3 |

2010 Q2 |

|

|

Total |

48 |

100% |

98.889 |

99.313 |

88.719 |

28.122 |

|

Within terms |

24 |

35,4% |

34.963 |

34.203 |

53.204 |

28.122 |

|

Delayed 0 - 30 |

17 |

64,6% |

63.926 |

65.110 |

35.515 |

|

|

Delayed 31 - 60 |

|

|

|

|

|

|

|

Delayed 61 - 90 |

7 |

0,0% |

|

|

|

|

|

Delayed 91 - 120 |

|

|

|

|

|

|

FINANCIAL INFORMATION

Auditor PricewaterhouseCoopers

N.V.

Auditor's report

According to the auditor,

the annual account gives a faithful description of the size and composition of

the company.

Type of publication

Consolidated

Annual accounts van Froconsur Holding B.V.

Willemskade 11

8911AX

KvK: 01059154

Publication Publication according to

obligations by law

CORE FIGURES

|

BOOKYEAR |

2009 |

2008 |

2007 |

|

Quick ratio |

1,54 |

1,40 |

1,12 |

|

Current ratio |

1,69 |

1,65 |

1,42 |

|

Nett workingcapital / Balance |

0,40 |

0,39 |

0,29 |

|

total |

|

|

|

|

Capital and reserves / Balance |

0,40 |

0,39 |

0,29 |

|

total |

|

|

|

|

Capital and reserves / Fixed |

29,23 |

24,40 |

19,84 |

|

assets |

|

|

|

|

Solvency |

0,69 |

0,65 |

0,43 |

|

Nett workingcapital |

4.198.626 |

4.061.196 |

3.596.000 |

|

Capital and reserves |

4.209.782 |

4.049.623 |

3.610.000 |

|

Change capital and reserves |

3,95% |

12,18% |

-17,56% |

|

change short term liabilities |

-2,09% |

-26,95% |

-15,21% |

|

Operating profit |

522.818 |

906.426 |

869.000 |

|

Nett Turnover |

|

|

23.906.000 |

Annual accounts The published financial information

is the consolidated group information.

Last annual accounts 2009

Type of publication

consolidated

Turnover 2007:

23.906.000

2006: 34.027.000

2005: 36.642.000

Gross profit 2007:

2.334.000

2006: 2.471.000

2005: 3.583.000

Operating profit 2007: 869.000

2006: 586.000

2005: 809.000

Result after taxes 2007: -616.000

2006: 70.000

2005: 1.110.000

Tendency Constant

Tendency capital and

reserves

|

6M |

|

|

|

||||||

|

4M |

|

|

|

|

|

|

|

||

|

zn |

|

|

|

|

|

|

|

|

|

|

0 |

|

|

i |

|

i |

|

i |

|

i |

|

2006 |

2007 |

2008 |

2009 |

||||||

Capital and reserves 2009 4.209.782

Total debt 2009 6.204.914

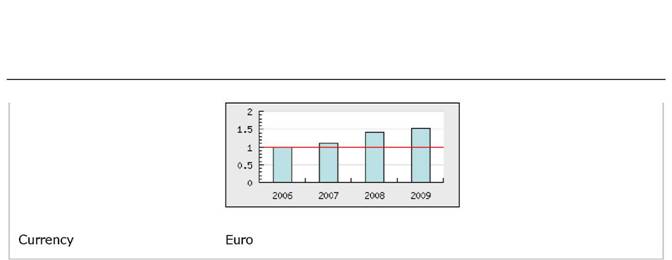

Current ratio 2009 1,69

Quick ratio 2009 1,54

Nett working capital 2009 4.198.626

Profitability Positive

Solvency Positive

Liquidity Sufficient

Current- & Quick ratio

|

2 |

|

|

|

|

|

||||

|

1 |

|

|

|

|

|

|

|

|

|

|

0 |

|

|

i |

|

1 |

|

i |

|

|

|

2006 |

2007 |

2003 |

2009 |

||||||

BALANCE

|

|

|

|

|

|

|

2009 |

2008 |

2007 |

|

End of bookyear |

31-12-2009 |

31-12-2008 |

31-12-2007 |

|

Other tangible assets |

144.024 |

|

|

|

Tangible assets |

144.024 |

165.958 |

182.000 |

|

Fixed assets |

144.024 |

165.958 |

182.000 |

|

|

|||

|

Stocks and work in progress |

949.087 |

1.558.655 |

2.615.000 |

|

Trade debtors |

7.741.727 |

7.778.290 |

|

|

Other amounts receivable |

1.578.306 |

925.624 |

|

|

Accounts receivable |

9.320.033 |

8.703.914 |

9.470.000 |

|

Liquid assets |

1.552 |

514 |

1.000 |

|

Current assets |

10.270.672 |

10.263.083 |

12.086.000 |

|

Total assets |

10.414.696 |

10.429.041 |

12.268.000 |

|

|

|||

|

Capital and reserves |

4.209.782 |

4.049.623 |

3.610.000 |

|

Provisions |

132.868 |

177.531 |

166.000 |

|

other long term debts |

|

0 |

|

|

Long term liabilities |

|

O |

2.000 |

|

Debts to credit institutions |

5.427.735 |

5.802.216 |

|

|

Other short term debts |

644.311 |

399.671 |

|

|

Total short term debt |

6.072.046 |

6.201.887 |

8.490.000 |

|

Total debt |

6.204.914 |

6.379.418 |

8.658.000 |

|

Total Liabilities |

10.414.696 |

10.429.041 |

12.268.000 |

|

|

|||

|

PROFIT & LOSS ACCOUNT |

|

|

|

|

BOOKYEAR |

2009 |

2008 |

2007 |

|

Turnover |

|

|

23.906.000 |

|

Nett Turnover |

|

|

23.906.000 |

|

Cost of sales |

|

|

21.572.000 |

|

Gross profit |

2.141.299 |

2.331.499 |

2.334.000 |

|

Wages employees |

|

|

771.000 |

|

Sales costs |

143.109 |

183.210 |

|

|

Other operating charges |

1.475.372 |

1.241.863 |

694.000 |

|

Operating charges |

1.618.481 |

1.425.073 |

23.037.000 |

|

Operating profit |

522.818 |

906.426 |

869.000 |

|

Financial income |

0 |

0 |

|

|

Financial charges |

55.517 |

338.470 |

515.000 |

|

Financial Result |

-55.517 |

-338.470 |

-515.000 |

|

Result Participations |

|

|

-886.000 |

|

Result before taxes |

467.301 |

567.956 |

-532.000 |

|

Income taxes |

107.142 |

128.090 |

84.000 |

|

Result after taxes |

360.159 |

439.866 |

-616.000 |

|

Nett result |

360.159 |

439.866 |

-616.000 |

|

Income Attributable to minority |

|

|

46.000 |

|

Interest |

|

|

|

COMPANY STRUCTURE

|

Froconsur Holding B.V. (01059154) |

|

|

|

|

|

Froconsur Overseas B.V.

(01069106) |

|

|

|

|

|

Subsidiary |

|

|

Froconsur B.V. (01076844) |

|

|

|

|

|

Subsidiary |

|

|

Latido Leeuwarden B.V.

(01076845) |

|

|

|

|

|

Subsidiary |

|

|

Froconsur Logistics B.V.

(01079666) |

|

|

|

|

|

Subsidiary |

|

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.45.20 |

|

|

1 |

Rs.73.16 |

|

Euro |

1 |

Rs.61.88 |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with full

security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

---- |

NB |

New Company |

---- |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.