![]()

MIRA INFORM REPORT

|

Report Date : |

23.02.2011 |

IDENTIFICATION DETAILS

|

Name : |

VAN SON LIQUIDS B.V. |

|

|

|

|

Registered Office : |

2e Loswal 18, 1216bc

|

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.12.2009 |

|

|

|

|

Date of Incorporation : |

28.07.1986 |

|

|

|

|

Com. Reg. No.: |

32041559 |

|

|

|

|

Legal Form : |

Limited Company |

|

|

|

|

Line of Business : |

Manufacturer of paints |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Maximum Credit Limit : |

€ 40.000 |

|

Status : |

Moderate |

|

Payment

Behaviour : |

Regular |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – June 30, 2010

|

Country Name |

Previous Rating (01.04.2010) |

Current Rating (30.06.2010) |

|

|

a1 |

a1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

CONTACTINFORMATION

|

Company name |

Van Son

Liquids B.V. |

|

Tradename |

Van Son Liquids B.V. |

|

Address |

2e Loswal 18 |

|

|

1216BC |

|

|

|

|

Mail address |

Postbus 491 |

|

|

1200AL |

|

|

|

|

Telephone number |

0356260930 |

|

Telefax number |

0356260935 |

|

E-mail address |

|

|

Website |

CREDIT LIMIT

|

Credit limit |

A credit of € 40.000 may be

granted |

COMPANY INFORMATION

|

Handelsregisternummer |

32041559 |

|

Registered

in Chamber of commerce |

Gooi-, Eem- en Flevoland |

|

Act of foundation |

17-11-1986 |

|

Date of constitution |

28-07-1986 |

|

Continuation date |

17-11-1986 |

|

Last change in statutes |

17-07-1998 |

|

Legal form |

Besloten Vennootschap (Limited

Company) |

|

Place of constitution |

|

|

Capital |

EUR 1.134.450,54 |

|

Issued capital |

EUR 249.579,12 |

|

Paid up capital |

EUR 249.579,12 |

NACE-code Manufacture of paints (2430)

SBI-code Manufacture of paints, varnishes and similar

coatings, printing ink a mastics (203)

Formal objective Het

fabriceren en in de handel brengen van drukinkten en aanverwante artikelen, in

de ruimste zin, alsmede het waarnemen van agenturen

(Manufacturing and marketing of printing inks and related products in the widest sense, and observing agencies)

|

Employees |

Total: 0 |

|

|

|

Special remarks employees |

Only worked with borrowed

personnel from the Koninklijke |

|

|

|

|

Drukinktfabrieken van Son B.V.. |

|

|

|

Bookyear |

2009 |

2008 |

2007 |

|

Number |

0 |

0 |

15 |

|

Change |

0,00% |

-100,00% |

0,00% |

COMPANY STRUCTURE

Shareholder

KvK: 32020245

Active since: 15-12-1994

Percentage: 100.00%

Holding company

KvK: 32020245

Affiliated companies

Tube Packaging B.V.

Kleine Drift 41

1221JX

KvK: 05059603

Koninklijke Drukinktfabrieken Van

Son B.V. Kleine Drift 41

1221JX

KvK: 32001374

Bankers

·

ABN

Amro Bankers NV

·

Fortis

Bankers (

|

Real

estate |

Lease |

|

|

The real estate is checked at

the land registration office |

|

|

Object code: |

|

|

Owner: GRAVURE & |

MANAGEMENT

Management

J.W. van der Laan

Johannes Wilhelmus

Authorization: Limited authorization

Position: Manager

Date appointed: 01-09-1993

Date of birth: 05-07-1952

W.J. van Mastrigt

Willem Johan

Authorization: Fully authorized

Position: Manager

Date appointed: 01-02-2009

Date of birth: 13-11-1958

PAYMENT INFORMATION

Payment experiences Payments are regular

Payments Based on multiple payment experiences up to €

7.500

Quarter: 2 2010: 60 Average days

Quarter: 3 2010: 63 Average days

Quarter: 4 2010: 60 Average days

Quarter: 1 2011: 40 Average days

|

|

invoices |

current quarter |

2010 Q4 |

2010 Q3 |

2010 Q2 |

|

|

Total |

52 |

100% |

11.643 |

14.330 |

14.278 |

14.004 |

|

Within terms |

22 |

68,7% |

7.994 |

2.907 |

3.011 |

3.530 |

|

Delayed 0 - 30 |

28 |

31,3% |

3.649 |

11.423 |

10.312 |

9.678 |

|

Delayed 31 - 60 |

2 |

0,0% |

|

|

955 |

796 |

|

Delayed 61 - 90 |

|

|||||

|

Delayed 91 - 120 |

|

|

|

|

|

|

|

Delayed 120+ days |

|

|||||

FINANCIAL INFORMATION

Publication financial statement Annual

accounts 2009 are published on 03-02-2011

Annual

accounts 2008 are published on 16-02-2010

Annual

accounts 2007 are published on 13-03-2009

Type of

publication Corporate

Publication Publication according to

obligations by law

CORE FIGURES

|

BOOKYEAR |

2009 |

2008 |

2007 |

|

Quick ratio |

0,55 |

0,87 |

1,12 |

|

Current ratio |

0,93 |

1,35 |

1,84 |

|

Nett workingcapital / Balance |

-0,03 |

0,10 |

0,15 |

|

total |

|

|

|

|

Capital and reserves / Balance |

0,33 |

0,39 |

0,42 |

|

total |

|

|

|

|

Capital and reserves / Fixed |

0,49 |

0,63 |

0,63 |

|

assets |

|

|

|

|

Solvency |

0,49 |

0,65 |

0,74 |

|

Nett workingcapital |

-96.000 |

399.000 |

615.000 |

|

Capital and reserves |

1.192.000 |

1.629.000 |

1.759.000 |

|

Change capital and reserves |

-26,83% |

-7,39% |

22,41% |

|

change short term liabilities |

16,43% |

54,62% |

-72,54% |

Annual accounts The company is

obligated to publish its annual accounts

Last annual accounts 2009

Tendency Not

to be judged because of the absence of sufficient financial

information

Tendency

capital and reserves

Capital and reserves 2009 1.192.000

Total debt 2009 2.450.000

Current ratio 2009 0,93

Quick ratio 2009 0,55

Nett workingcapital 2009 -96.000

Profitability

Negative

Solvency Positive

Liquidity Negative

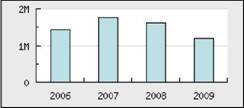

Current- & Quickratio

|

2 1 0 |

|

|

|

||||||

|

|

|

i |

|

i |

|

i |

|

i |

|

|

2006 2007 2008 2009 |

|||||||||

|

1.5 1 0.5 0 |

: |

|

|

||||||

|

|

|

i |

|

i |

|

i |

|

i |

|

|

2006 2007 2008 2009 |

|||||||||

BALANCE Sheet

Currency Euro

|

BOOKYEAR |

2009 |

2008 |

2007 |

|

End of bookyear |

31-12-2009 |

31-12-2008 |

31-12-2007 |

|

Tangible assets |

2.413.000 |

2.605.000 |

2.789.000 |

|

Fixed assets |

2.413.000 |

2.605.000 |

2.789.000 |

|

|

|||

|

Stocks and work in progress |

503.000 |

544.000 |

526.000 |

|

Accounts receivable |

716.000 |

864.000 |

731.000 |

|

Liquid assets |

10.000 |

129.000 |

94.000 |

|

Current assets |

1.229.000 |

1.537.000 |

1.351.000 |

|

Total assets |

3.642.000 |

4.142.000 |

4.140.000 |

|

|

|||

|

Capital and reserves |

1.192.000 |

1.629.000 |

1.759.000 |

|

other long term debts |

|

1.375.000 |

1.645.000 |

|

Long term liabilities |

1.125.000 |

1.375.000 |

1.645.000 |

|

Other short term debts |

|

1.138.000 |

736.000 |

|

Total short term debt |

1.325.000 |

1.138.000 |

736.000 |

|

Total debt |

2.450.000 |

2.513.000 |

2.381.000 |

|

Total Liabilities |

3.642.000 |

4.142.000 |

4.140.000 |

COMPANY STRUCTURE

Tube Packaging B.V. (05059603)

Koninklijke Drukinktfabrieken Van Son B.V. (32001374)

Van Son Liquids B.V. (32041559)

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.45.20 |

|

|

1 |

Rs.73.07 |

|

Euro |

1 |

Rs.61.41 |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.