MIRA

INFORM REPORT

|

Report Date : |

13.08.2013 |

IDENTIFICATION DETAILS

|

Name : |

MOXY-COPENHAGEN APS |

|

|

|

|

Registered Office : |

Prags Boulevard 92 2300 Kobenhavn S |

|

|

|

|

Country : |

Denmark |

|

|

|

|

Financials (as on) : |

31.12.2012 |

|

|

|

|

Date of Incorporation : |

05.11.2008 |

|

|

|

|

Com. Reg. No.: |

31761603 |

|

|

|

|

Legal Form : |

Private limited company - ApS |

|

|

|

|

Line of Business : |

Retail sale of clothing in specialised stores |

|

|

|

|

No. of Employees : |

12 Approximately |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

Payment Behaviour : |

No Complaints |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31st, 2013

|

Country Name |

Previous Rating (31.12.2012) |

Current Rating (31.03.2013) |

|

Denmark |

A2 |

A2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

DENMARK - ECONOMIC OVERVIEW

This thoroughly modern market economy features a high-tech

agricultural sector, state-of-the-art industry with world-leading firms in

pharmaceuticals, maritime shipping and renewable energy, and a high dependence

on foreign trade. Denmark is a member of the European Union (EU); Danish

legislation and regulations conform to EU standards on almost all issues. Danes

enjoy a high standard of living and the Danish economy is characterized by

extensive government welfare measures and an equitable distribution of income.

Denmark is a net exporter of food and energy and enjoys a comfortable balance

of payments surplus but depends on imports of raw materials for the

manufacturing sector. Within the EU, Denmark is among the strongest supporters

of trade liberalization. After a long consumption-driven upswing, Denmark's economy

began slowing in 2007 with the end of a housing boom. Housing prices dropped

markedly in 2008-09 and, following a short respite in 2010, has since continued

to decline. The global financial crisis has exacerbated this cyclical slowdown

through increased borrowing costs and lower export demand, consumer confidence,

and investment. The global financial crisis cut Danish real GDP in 2008-09.

Denmark made a modest recovery in 2010 with real GDP growth of 1.3%, in part

because of increased government spending; however, the country experienced a

technical recession in late 2010-early 2011. Historically low levels of

unemployment rose sharply with the recession and have remained at about 6% in

2010-12, based on the national measure, about two-thirds average EU unemployment.

An impending decline in the ratio of workers to retirees will be a major

long-term issue. Denmark maintained a healthy budget surplus for many years up

to 2008, but the budget balance swung into deficit in 2009. In spite of the

deficits, the new coalition government delivered a modest stimulus to the

economy in 2012. Nonetheless, Denmark's fiscal position remains among the

strongest in the EU with public debt at about 45% of GDP in 2012. Despite

previously meeting the criteria to join the European Economic and Monetary

Union (EMU), so far Denmark has decided not to join, although the Danish krone

remains pegged to the euro. Denmark held the EU presidency during the first

half of 2012; priorities included promoting a responsible, dynamic, green, and

safe Europe, while working to steer Europe out of its euro zone economic

crisis.

Source

: CIA

Summary

|

Company name |

MOXY-COPENHAGEN APS |

|

Operative address |

PRAGS BOULEVARD 92 |

|

Status |

Active |

|

Legal form |

Private limited company - ApS |

||||

|

Registration number |

Trade register number: 31761603 |

||||

|

VAT-number |

DK31 76 16 03 |

||||

|

Year |

2012 |

Mutation |

2011 |

Mutation |

2010 |

|

Fixed assets |

12.455 |

|

|

|

|

|

Total receivables |

18.348 |

18,61 |

15.469 |

26,17 |

12.260 |

|

|

|||||

|

Total equity |

19.688 |

28,39 |

15.334 |

217,41 |

-13.060 |

|

Short term liabilities |

146.117 |

16,05 |

125.904 |

-1,48 |

127.798 |

|

|

|||||

|

Net result |

4.420 |

-84,50 |

28.517 |

227,38 |

-22.388 |

|

|

|||||

|

Working capital |

8.705 |

-42,73 |

15.200 |

215,21 |

-13.193 |

|

Quick ratio |

0,69 |

7,81 |

0,64 |

-1,54 |

0,65 |

Contact information

|

Company name |

MOXY-COPENHAGEN APS |

|

Operative address |

PRAGS BOULEVARD 92 |

|

Correspondence address |

PRAGS BOULEVARD 92 |

|

Telephone number |

+45 32952274 |

|

Fax number |

+45 32952274 |

|

Website |

www.moxy-copenhagen.dk |

Registration

|

Registration number |

Trade register number: 31761603 |

|

VAT-number |

DK31 76 16 03 |

|

Status |

Active |

|

Establishment date |

2008-11-05 |

|

Legal form |

Private limited company - ApS |

|

Subscribed share capital |

DKK 125.000 |

Activities

|

NACE |

Retail sale of clothing in specialised stores (4771) |

Relations

|

Shareholders |

Name: KARINA THOLSTRUP HANSEN |

Management

|

Management |

Fullname: Mr. Rikke Molge |

Financial analysis

|

Trend |

Fluctuating |

|

Profitability |

Nil |

|

Solvability |

Limited |

|

Liquidity |

Limited |

|

Show amount in |

Euro |

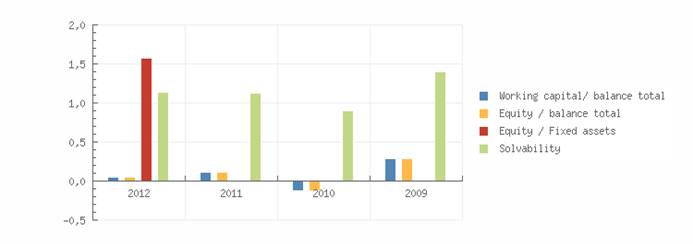

Key figures

|

Year |

2012 |

2011 |

2010 |

2009 |

|

|

Quick ratio |

0,69 |

0,64 |

0,65 |

0,37 |

|

|

Current ratio |

1,06 |

1,12 |

0,90 |

1,40 |

|

|

|

|||||

|

Working capital/ balance total |

0,05 |

0,11 |

-0,12 |

0,29 |

|

|

Equity / balance total |

0,05 |

0,11 |

-0,12 |

0,29 |

|

|

Equity / Fixed assets |

1,58 |

|

|

|

|

|

Solvability |

1,14 |

1,12 |

0,90 |

1,40 |

|

|

|

|||||

|

Working capital |

8.705 |

15.200 |

-13.193 |

9.362 |

|

|

Equity |

19.688 |

15.334 |

-13.060 |

9.496 |

|

|

Mutation equity |

28,39 |

217,41 |

-237,53 |

|

|

|

Mutation short term liabilities |

16,05 |

-1,48 |

446,01 |

|

|

|

|

|||||

|

Return on total assets (ROA) |

3,60 |

27,07 |

-26,16 |

-29,79 |

|

|

Return on equity (ROE) |

30,61 |

249,13 |

229,59 |

-102,81 |

|

|

Gross profit margin |

2,00 |

|

-28,67 |

-30,42 |

|

|

Net profit margin |

1,12 |

|

-18,52 |

-22,50 |

|

|

|

|||||

|

Average collection ratio |

2,70 |

|

0,95 |

1,37 |

|

|

Average payment ratio |

21,50 |

|

9,86 |

5,22 |

|

|

Equity turnover ratio |

20,04 |

|

-9,25 |

3,38 |

|

|

Total assets turnover ratio |

2,36 |

|

1,05 |

0,98 |

|

|

Fixed assets turnover ratio |

31,68 |

|

|

|

|

|

Inventory conversion ratio |

7,24 |

|

3,83 |

1,33 |

|

|

|

|||||

|

Turnover |

394.556 |

|

120.869 |

32.099 |

|

|

Gross margin |

31.607 |

45.196 |

-34.648 |

-9.763 |

|

|

Operating result |

7.902 |

39.143 |

-34.648 |

-9.763 |

|

|

Net result after taxes |

4.420 |

28.517 |

-22.388 |

-7.222 |

|

|

|

|||||

|

Cashflow |

5.357 |

|

|

|

|

|

EBITDA |

8.839 |

|

|

|

|

|

Summary |

The 2012 financial result structure is a

postive working captial of 8.705 euro, which is in agreement with 5 % of the

total assets of the company. |

||||

Financial statement

|

Last annual account |

2012 |

|

Remark annual account |

The company is obliged to file its financial statements. |

|

Type of annual account |

Corporate |

|

Annual account |

MOXY-COPENHAGEN APS |

Balance

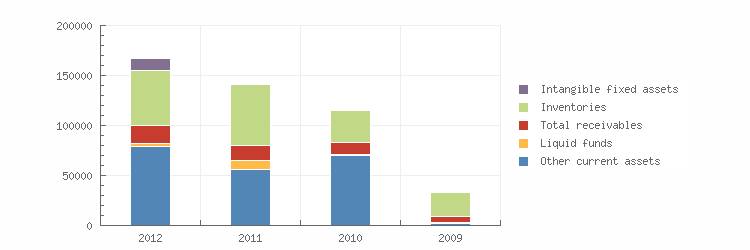

|

Year |

2012 |

2011 |

2010 |

2009 |

|

|

End date |

2012-12-31 |

2011-12-31 |

2010-12-31 |

2009-12-31 |

|

|

Intangible fixed assets |

12.455 |

|

|

|

|

|

Fixed assets |

12.455 |

|

|

|

|

|

|

|||||

|

Inventories |

54.509 |

60.800 |

31.583 |

24.074 |

|

|

Total receivables |

18.348 |

15.469 |

12.260 |

6.152 |

|

|

Liquid funds |

2.679 |

8.743 |

800 |

134 |

|

|

Other current assets |

79.286 |

56.092 |

69.963 |

2.407 |

|

|

Current assets |

154.822 |

141.104 |

114.605 |

32.768 |

|

|

Total assets |

167.278 |

141.104 |

114.605 |

32.768 |

|

|

|

|||||

|

Total equity |

19.688 |

15.334 |

-13.060 |

9.496 |

|

|

Provisions |

1.339 |

|

|

|

|

|

Accounts payable |

|

|

2.399 |

|

|

|

Short term liabilities |

146.117 |

125.904 |

127.798 |

23.406 |

|

|

Total liabilities |

167.278 |

141.104 |

114.605 |

32.768 |

|

|

Summary |

The total assets of the company increased

with 18.55 % between 2011 and 2012. |

||||

Profit and loss

|

Year |

2012 |

2011 |

2010 |

2009 |

|

|

Net turnover |

394.556 |

|

120.869 |

32.099 |

|

|

|

|||||

|

Cost of sales |

362.949 |

|

155.517 |

41.862 |

|

|

Gross margin |

31.607 |

45.196 |

-34.648 |

-9.763 |

|

|

|

|||||

|

Wages and salaries |

22.768 |

6.053 |

|

|

|

|

Amorization and depreciation |

938 |

|

|

|

|

|

Operating expenses |

23.706 |

6.053 |

|

|

|

|

Operating result |

7.902 |

39.143 |

-34.648 |

-9.763 |

|

|

|

|||||

|

Financial income |

536 |

538 |

4.931 |

|

|

|

Financial expenses |

2.411 |

1.480 |

267 |

|

|

|

Financial result |

-1.875 |

-942 |

4.664 |

|

|

|

Result on ordinary operations before taxes |

6.027 |

38.202 |

-29.984 |

-9.763 |

|

|

|

|||||

|

Taxation on the result of ordinary activities |

1.607 |

9.685 |

-7.596 |

-2.541 |

|

|

Result of ordinary activities after taxes |

4.420 |

28.517 |

-22.388 |

-7.222 |

|

|

|

|||||

|

Net result |

4.420 |

28.517 |

-22.388 |

-7.222 |

|

|

Summary |

The gross profit of the company decreased

by -30.07 % between 2011 and 2012. |

||||

Publications

|

Remarks |

Status: Active |

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.60.80 |

|

|

1 |

Rs.94.21 |

|

Euro |

1 |

Rs.81.03 |

INFORMATION DETAILS

|

Report

Prepared by : |

PRL |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a

composite of weighted scores obtained from each of the major sections of this

report. The assessed factors and their relative weights (as indicated through

%) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.