MIRA

INFORM REPORT

|

Report Date : |

24.08.2013 |

IDENTIFICATION DETAILS

|

Name : |

MTS SYSTEMS CORPORATION |

|

|

|

|

Registered Office : |

Technology Drive 14000 Eden Prairie 55344 Minnesota |

|

|

|

|

Country : |

United States |

|

|

|

|

Financials (as on) : |

30.03.2013 |

|

|

|

|

Date of Incorporation : |

12.09.1966 |

|

|

|

|

Com. Reg. No.: |

1K-817 |

|

|

|

|

Legal Form : |

Corporation for Profit |

|

|

|

|

Line of Business : |

Testing and Sensing Solutions |

|

|

|

|

No. of Employees : |

2 147 |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Good |

|

Payment Behaviour : |

Regular |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31st, 2013

|

Country Name |

Previous Rating (31.12.2012) |

Current Rating (31.03.2013) |

|

United States |

A1 |

A1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

UNITED STATES - ECONOMIC OVERVIEW

The US has the largest and most technologically powerful

economy in the world, with a per capita GDP of $49,800. In this market-oriented

economy, private individuals and business firms make most of the decisions, and

the federal and state governments buy needed goods and services predominantly

in the private marketplace. US business firms enjoy greater flexibility than

their counterparts in Western Europe and Japan in decisions to expand capital

plant, to lay off surplus workers, and to develop new products. At the same

time, they face higher barriers to enter their rivals' home markets than

foreign firms face entering US markets. US firms are at or near the forefront

in technological advances, especially in computers and in medical, aerospace,

and military equipment; their advantage has narrowed since the end of World War

II. The onrush of technology largely explains the gradual development of a

"two-tier labor market" in which those at the bottom lack the

education and the professional/technical skills of those at the top and, more

and more, fail to get comparable pay raises, health insurance coverage, and

other benefits. Since 1975, practically all the gains in household income have

gone to the top 20% of households. Since 1996, dividends and capital gains have

grown faster than wages or any other category of after-tax income. Imported oil

accounts for nearly 55% of US consumption. Crude oil prices doubled between

2001 and 2006, the year home prices peaked; higher gasoline prices ate into

consumers' budgets and many individuals fell behind in their mortgage payments.

Oil prices climbed another 50% between 2006 and 2008, and bank foreclosures more

than doubled in the same period. Besides dampening the housing market, soaring

oil prices caused a drop in the value of the dollar and a deterioration in the

US merchandise trade deficit, which peaked at $840 billion in 2008. The

sub-prime mortgage crisis, falling home prices, investment bank failures, tight

credit, and the global economic downturn pushed the United States into a

recession by mid-2008. GDP contracted until the third quarter of 2009, making

this the deepest and longest downturn since the Great Depression. To help

stabilize financial markets, in October 2008 the US Congress established a $700

billion Troubled Asset Relief Program (TARP). The government used some of these

funds to purchase equity in US banks and industrial corporations, much of which

had been returned to the government by early 2011. In January 2009 the US

Congress passed and President Barack OBAMA signed a bill providing an

additional $787 billion fiscal stimulus to be used over 10 years - two-thirds

on additional spending and one-third on tax cuts - to create jobs and to help

the economy recover. In 2010 and 2011, the federal budget deficit reached

nearly 9% of GDP. In 2012 the federal government reduced the growth of spending

and the deficit shrank to 7.6% of GDP. Wars in Iraq and Afghanistan required

major shifts in national resources from civilian to military purposes and

contributed to the growth of the budget deficit and public debt. Through 2011,

the direct costs of the wars totaled nearly $900 billion, according to US

government figures. US revenues from taxes and other sources are lower, as a

percentage of GDP, than those of most other countries. In March 2010, President

OBAMA signed into law the Patient Protection and Affordable Care Act, a health

insurance reform that will extend coverage to an additional 32 million American

citizens by 2016, through private health insurance for the general population

and Medicaid for the impoverished. Total spending on health care - public plus

private - rose from 9.0% of GDP in 1980 to 17.9% in 2010. In July 2010, the

president signed the DODD-FRANK Wall Street Reform and Consumer Protection Act,

a law designed to promote financial stability by protecting consumers from

financial abuses, ending taxpayer bailouts of financial firms, dealing with

troubled banks that are "too big to fail," and improving

accountability and transparency in the financial system - in particular, by

requiring certain financial derivatives to be traded in markets that are

subject to government regulation and oversight. In December 2012, the Federal

Reserve Board announced plans to purchase $85 billion per month of

mortgage-backed and Treasury securities in an effort to hold down long-term

interest rates, and to keep short term rates near zero until unemployment drops

to 6.5% from the December rate of 7.8%, or until inflation rises above 2.5%.

Long-term problems include stagnation of wages for lower-income families,

inadequate investment in deteriorating infrastructure, rapidly rising medical

and pension costs of an aging population, energy shortages, and sizable current

account and budget deficits - including significant budget shortages for state

governments.

Source

: CIA

REGISTERED NAME & COMPANY

SUMMARY

|

IDENTIFICATION |

|||

|

Legal Name: |

MTS SYSTEMS CORPORATION |

||

|

Legal Address |

Technology Drive 14000 |

||

|

Postal Town |

Eden Prairie |

||

|

Post Code |

55344 |

||

|

Primary Geographic Area |

Minnesota |

||

|

Country |

US |

||

|

Location Status |

Headquarters,Legal

Address, |

||

|

Operative Address |

Technology Drive 14000,

55344 Eden Prairie, MN, USA. |

||

|

Telephone: |

+1 (952) 937-4000 / +1

(800) 328-2255 |

Registration Number : |

1K-817 |

|

Fax: |

+1 (952) 937-4515 |

Legal Form: |

Corporation for Profit |

|

Email: |

info@mts.com |

Registered in: |

US |

|

Website: |

www.mts.com |

Date Created: |

1966 |

|

Manager: |

Jeffrey A. Graves - President and Chief Executive Officer |

Date Incorporated: |

September 12, 1966 |

|

Staff: |

2 147 |

Stock: |

15 694 491 |

|

|

|

Value: |

USD

0.25 par value |

|

Activity: |

Testing and Sensing

Solutions. |

||

DIRECTORS/MANAGEMENT

|

Management: |

JEFFREY A. GRAVES

President and Chief

Executive Officer

SUSAN E. KNIGHT

Chief Financial Officer

and Senior Vice President

DAVID J. ANDERSON

Non- Executive Chair of

the Board

JEAN-LOU CHAMEAU

Director

BRENDAN C. HEGARTY

Director

EMILY M. LIGGETT

Director

WILLIAM V. MURRAY

Director

BARB J. SAMARDZICH

Director

GAIL P. STEINEL

Director

NEGATIVE INFORMATION

Legal Fillings

|

There are several UCC**

files listed with the Secretary of State of Minnesota such as: There are various

claims, lawsuits, and pending actions against the Company and its

subsidiaries incident to the operations of its business. It is the opinion of

management, after consultation with counsel, that the ultimate resolution of

such claims, lawsuits and pending actions will not have a material adverse

effect on the Company’s consolidated financial position, results of

operations or liquidity. THE COMPANY IS NOT

LISTED ON THE OFAC LIST.* For information: * The Specially

Designated Nationals (SDN) List is a publication of OFAC which lists

individuals and organizations with whom United States citizens and permanent

residents are prohibited from doing business. ** The Uniform

Commercial Code (UCC) is one of a number of uniform acts that have been

promulgated in conjunction with efforts to harmonize the law of sales and

other commercial transactions in all 50 states within the United States of

America. The UCC deals primarily

with transactions involving personal property (movable property), not real

property (immovable property). It allows a creditor to

notify other creditors about a debtor’s assets used as collateral for a

secured transaction by filing a public notice (financing statement) with a

particular filing office. The Uniform Commercial

Code Bureau files and maintains on financial obligations (including IRS

liens) incurred by individuals (in business as a sole proprietor), business

entities and corporations. |

|

Public |

YES |

SHARE & SHARE CAPITAL

INFORMATION

|

Shareholders |

|

|

Listed at the stock

exchange: |

|

|

|

YES |

|

Capital: |

|

|

|

Breakdown % of Shares Held by All

Insider and 5% Owners: 1% % of Shares Held by

Institutional & Mutual Fund Owners: 90% % of Float Held by

Institutional & Mutual Fund Owners: 91% Number of Institutions

Holding Shares: 170 |

Shareholders Parent

Company(ies):

Major Direct Holders

Holder Shares

SAMARDZICH

BARB J 21,261

KNIGHT SUSAN E 18,528

HELLWIG JOACHIM 12,530

ANDERSON

DAVID J 11,482

MURRAY WILLIAM V 11,401

Top Institutional Holders

Holder Shares

Vanguard Group, Inc. (The) 961,400

Wellington Management

Company, LLP 906,962

New South Capital

Manangement Inc. 786,458

BlackRock Fund Advisors 758,902

Royce & Associates,

LLC 660,207

BlackRock Institutional

Trust Company, N.A. 476,330

Price (T.Rowe) Associates

Inc 439,340

Schroder Investment

Management Group 427,800

Dimensional Fund Advisors

LP 402,881

Mairs & Power Inc 1,786,960

Top Mutual Fund Holders

Holder Shares

Mairs & Power Growth

Fund Inc 1,200,000

Pennsylvania Mutual Fund

Inc 471,275

Price (T.Rowe) Small-Cap

Value Fund 424,200

iShares Core S&P

Smallcap ETF 277,721

iShares Russell 2000 Index

Fund 250,826

Vanguard Small-Cap Index

Fund 234,028

Vanguard Total Stock

Market Index Fund 219,672

Vanguard Small-Cap Growth

Index Fund 187,960

Victory Portfolios-Victory

Small Company

Opportunity Fund 177,789

Royce Total Return Fund 168,722

PAYMENT INFORMATION

|

Payments |

REGULAR |

GROUP STRUCTURE & AFFILIATED

COMPANIES

|

Related Companies: |

Subsidiaries of the

Registrant

MTS

Japan Ltd. - Japan

MTS Sensor Technology K.K.

- Japan

MTS Korea, Inc. - South

Korea

MTS Systems (China) Co.,

Ltd. - China (PRC)

MTS Systems GmbH - Germany

MTS Systems Norden AB -

Sweden

MTS Systems Ltd. - United

Kingdom

MTS Systems Srl - Italy

MTS Holdings France, SARL

- France

MTS Systems SAS - France

MTS Sensor Technologie

GmbH and Co. KG - Germany

MTS Automotive Sensors

GmbH - Germany

MTS Sensor Technologie und

Verwaltungs-GmbH - Germany

MTS

Systems (Hong Kong), Inc. - Minnesota

MTS Systems Switzerland

GmbH - Switzerland

MTS Testing Systems

(Canada) Ltd. - Ontario

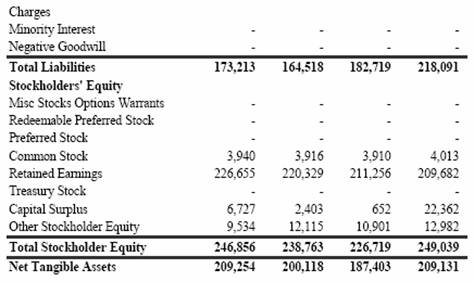

FINANCIAL INFORMATION

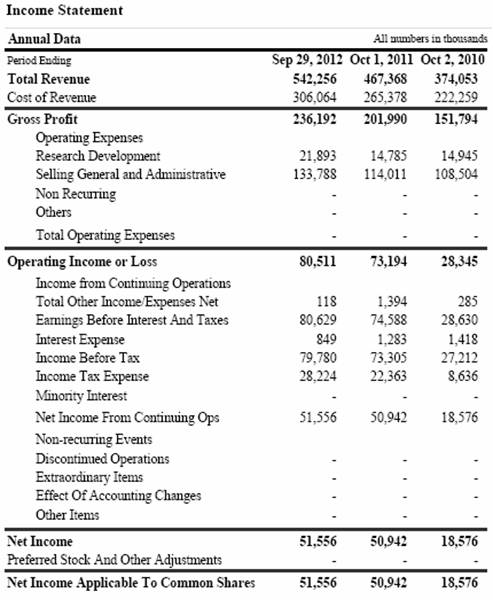

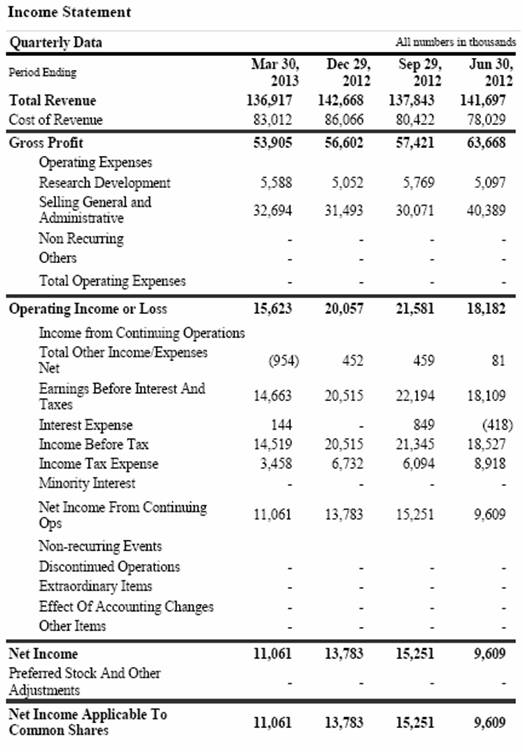

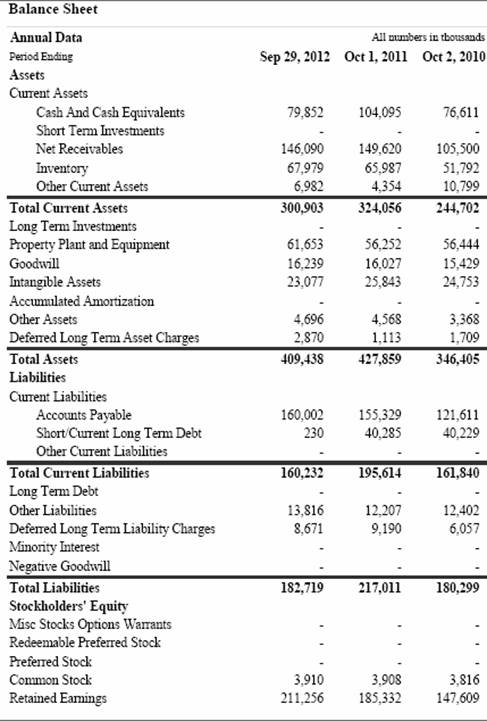

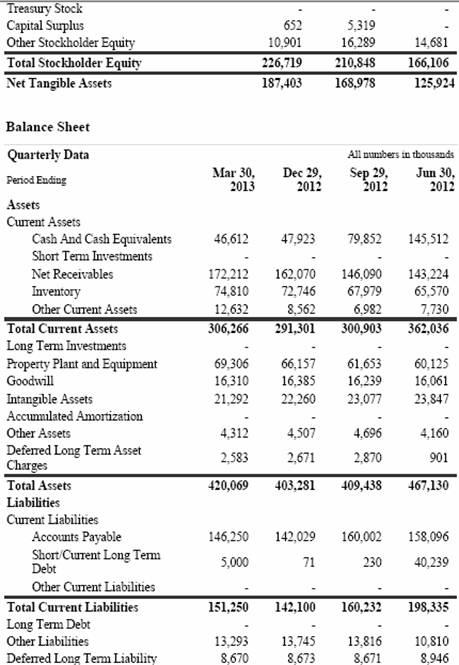

|

Financials - COMMERCIAL TRENDS

AND FORECAST |

|

The subject is a public

company traded at NYSE Stock Exchange under the symbol "MTSC".

Please find enclosed the financial statements. |

|

FINANCIAL SUMMARY |

|

|

Profitability |

GOOD |

|

Indebtedness |

CONTROLLED |

|

Cash |

NORMAL |

FOREIGN EXCHANGE RATES

N/a

ADDITIONAL INFORMATION

|

GEOPOLITICS - UNITED

STATES |

|

|

POLITICAL DATA |

ECONOMIC DATA |

|

Form of Government:

Federal

|

Currency: 100.00 USD =

77.7140 EUR |

|

BANKS |

|

|

Name of the Bank |

Wells Fargo Bank, NA |

|

Location |

Confidential |

|

Comments |

We could not verify this

information with the company. |

|

|

|

|

Name of the Bank |

Fifth Third Bank |

|

Location |

Confidential |

|

Comments |

We could not verify this

information with the company. |

|

|

|

|

Name of the Bank |

The Bank of Tokyo

Mitsubishi UFJ, Ltd |

|

Location |

Confidential |

|

Comments |

We could not verify this

information with the company. |

|

|

|

|

Name of the Bank |

U.S. Bank National

Association |

|

Location |

Confidential |

|

Comments |

We could not verify this

information with the company. |

|

|

|

|

Name of the Bank |

JPMorgan Chase Bank, N.A |

|

Location |

Confidential |

|

Comments |

We could not verify this

information with the company. |

|

|

|

|

Name of the Bank |

COMMERCE NATIONAL BANK |

|

Location |

COLUMBUS, OH. |

|

Comments |

We could not verify this

information with the company. |

|

BUSINESS HISTORY |

|

|

|

MTS Systems Corporation

was founded in 1966. |

|

PRINCIPAL ACTIVITY |

|

|

|

MTS Systems Corporation

supplies test systems and industrial position sensors. |

|

Products/Services

description: |

|

The company’s Test segment

provides testing solutions, including road simulators for durability

simulation; tire performance and rolling resistance measurement systems; moving

road-plane systems and balances use for aerodynamics measurements in wind

tunnels; systems for the physical characterization of materials, such as

ceramics, composites, and steel; systems to test durability and performance of

implants, prostheses, and other medical and dental materials and devices.

This segment also offers

products, systems, and software to perform static and fatigue testing of

aircraft and space vehicles; systems for structural engineering, including high

force static and dynamic testing; and seismic simulation tables to test the

designs of structures and set building codes.

In addition, it provides

various accessories and spare parts, as well as installation, calibration,

maintenance, training, and consulting services.

This segment serves

automobile, truck, motorcycle, motorsports vehicle, construction equipment,

agricultural equipment, rail, and off-road vehicle manufacturers and their

suppliers, as well as power generation, aerospace, bio-medical, wind energy,

structural engineering, and petroleum industries.

The company’s Sensors

segment manufactures products utilizing magnetostriction technology for

manufacturers of mobile equipment, plastic injection molding machines, and wood

product processing equipment, as well as to steel mill, fluid power, oil and

gas, medical, and alternative energy industries.

It also offers products to

measure fluid displacement for customers in the process industries.

|

Sales are: |

|

|

|

Wholesale |

|

Clients: |

|

|

|

The company sells its products

through direct sales organization, and independent representatives and

distributors, as well as through the Internet and catalogs. |

|

Suppliers: |

|

|

|

MTS

SYSTEMS(CHINA)CO.,LTD A5,FOREIGN TRADE XINGYE

INDUSTRIAL TONGLE,NANSHAN SHENZHEN, GUANGDONG 518052 CN |

|

Operations area: |

|

|

|

National, International |

|

The company imports from

Sweden, Netherlands, Germany, UK, Japan, China, Australia |

|

|

The company export to

Americas, Europa and Asia. |

|

|

Trade References: |

|

|

|

We could not obtained suppliers

contact information from North America or near regiosn for us to check trade

references. |

|

Competitors: |

|

|

|

Aero Systems

Engineering, Inc. General Electric Company OYO Corporation |

|

The subject employs 2

147 employee(s) |

|

|

Comments on staff: |

|

|

|

The Company had 2 147

employees as of September 29, 2012, including 1 157 employees located outside

the United States. |

|

PAYMENTS |

|

|

|

regular |

|

LOCATION |

|

|

Headquarters |

|

|

|

Technology Drive 14000, 55344

Eden Prairie, MN, USA. |

|

Branches: |

|

|

|

The company has two

branches: Cary, North Carolina,

USA Chanhassen,

Minnesota, USA |

|

Business Overview: |

|

|

|

Demand is driven by

consumer income and the rate of product innovation. The profitability of

individual companies depends on manufacturing efficiency and effective

marketing and distribution. Large companies have advantages in economies of

scale in manufacturing, marketing, and distribution. Small companies can

compete effectively by offering specialty products or components in system

solutions, such as speakers in a home theatre system. |

NOTES & COMMENTS

|

Rating |

|

Local credit bureau gave

a Good credit rate. The company is in Good Standing.

This means that all local and federal taxes were paid on due date. |

Final Opinion

|

|

MTS Systems Corporation

was founded in 1966 and it is based in Minnesota. It is a large size, public

company, which supplies test systems and industrial position sensors. The comapny works

nationally and internationally importing materials from Sweden, Netherlands,

Germany, UK, Japan, China, Australia and exporting its products to the Americas,

Europa and Asia. The operative facilities

of the company are well equipped and prepared. Regarding legal fillings

found, we consider there would not be negative outcomes affecting the

company´s profitabillity. The comapny´s

profitability is good and its indebtedness is controlled. Theefore, we may

establish a credit line of EUR 3 000 000. |

|

APPENDIX |

|

|

Comments |

|

|

|

We contacted an

adminsitrative assistant who refused to provide its name nor the information requested

nor transferred our call on grounds of confidentiality. |

Standard & Poor’s

|

United

States of America Long-Term Rating Lowered To 'AA+' Due To Political Risks,

Rising Debt Burden; Outlook Negative |

|

Publication

date: 05-Aug-2011 20:13:14 EST |

·

We have lowered our long-term

sovereign credit rating on the United States of America to 'AA+' from 'AAA' and

affirmed the 'A-1+' short-term rating.

·

We have also removed both the short- and long-term ratings from

CreditWatch negative.

·

The downgrade reflects our

opinion that the fiscal consolidation plan that Congress and the Administration

recently agreed to falls short of what, in our view, would be necessary to

stabilize the government's medium-term debt dynamics.

·

More broadly, the downgrade

reflects our view that the effectiveness, stability, and predictability of

American policymaking and political institutions have weakened at a time of

ongoing fiscal and economic challenges to a degree more than we envisioned when

we assigned a negative outlook to the rating on April 18, 2011.

·

Since then, we have changed our

view of the difficulties in bridging the gulf between the political parties

over fiscal policy, which makes us pessimistic about the capacity of Congress

and the Administration to be able to leverage their agreement this week into a

broader fiscal consolidation plan that stabilizes the government's debt

dynamics any time soon.

·

The outlook on the long-term

rating is negative. We could lower the long-term rating to 'AA' within the next

two years if we see that less reduction in spending than agreed to, higher

interest rates, or new fiscal pressures during the period result in a higher

general government debt trajectory than we currently assume in our base case.

TORONTO (Standard &

Poor's) Aug. 5, 2011--Standard & Poor's Ratings Services said today that it

lowered its long-term sovereign credit rating on the United States of America

to 'AA+' from 'AAA'. Standard & Poor's also said that the outlook on the long-term

rating is negative. At the same time, Standard & Poor's affirmed its 'A-1+'

short-term rating on the U.S. In addition, Standard & Poor's removed both

ratings from CreditWatch, where they were placed on July 14, 2011, with

negative implications.

The transfer and

convertibility (T&C) assessment of the U.S.--our assessment of the

likelihood of official interference in the ability of U.S.-based public- and

private-sector issuers to secure foreign exchange for

debt service--remains

'AAA'.

We lowered our long-term

rating on the U.S. because we believe that the prolonged controversy over

raising the statutory debt ceiling and the related fiscal policy debate

indicate that further near-term progress containing the growth in public

spending, especially on entitlements, or on reaching an agreement on raising

revenues is less likely than we previously assumed and will remain a

contentious and fitful process. We also believe that the fiscal consolidation

plan that Congress and the Administration agreed to this week falls short of

the amount that we believe is necessary to stabilize the general government

debt burden by the middle of the decade.

Our lowering of the

rating was prompted by our view on the rising public debt burden and our

perception of greater policymaking uncertainty, consistent with our criteria

(see "Sovereign Government Rating Methodology and

Assumptions ," June 30, 2011, especially Paragraphs 36-41).

Nevertheless, we view the U.S. federal government's other economic, external,

and monetary credit attributes, which form the basis for the sovereign rating,

as broadly unchanged.

We have taken the ratings

off CreditWatch because the Aug. 2 passage of the Budget Control Act Amendment

of 2011 has removed any perceived immediate threat of payment default posed by

delays to raising the government's debt ceiling. In addition, we believe that

the act provides sufficient clarity to allow us to evaluate the likely course

of U.S. fiscal policy for the next few years.

The political

brinksmanship of recent months highlights what we see as America's governance

and policymaking becoming less stable, less effective, and less predictable

than what we previously believed. The statutory debt ceiling and the threat of

default have become political bargaining chips in the debate over fiscal

policy. Despite this year's wide-ranging debate, in our view, the differences

between political parties have proven to be extraordinarily difficult to

bridge, and, as we see it, the resulting agreement fell well short of the

comprehensive fiscal consolidation program that some proponents had envisaged

until quite recently. Republicans and Democrats have only been able to agree to

relatively modest savings on discretionary spending while delegating to the

Select Committee decisions on more comprehensive measures. It appears that for

now, new revenues have dropped down on the menu of policy options. In addition,

the plan envisions only minor policy changes on Medicare and little change in

other entitlements,

the containment of which

we and most other independent observers regard as key to long-term fiscal

sustainability.

Our opinion is that elected

officials remain wary of tackling the structural issues required to effectively

address the rising U.S. public debt burden in a manner consistent with a 'AAA'

rating and with 'AAA' rated sovereign peers (see Sovereign Government Rating Methodology and

Assumptions," June 30, 2011, especially Paragraphs 36-41). In

our view, the difficulty in framing a consensus on fiscal policy weakens the

government's ability to manage public finances and diverts attention from the

debate over how to achieve more balanced and dynamic economic growth in an era

of fiscal stringency and private-sector deleveraging (ibid). A new political

consensus might (or might not) emerge after the 2012 elections, but we believe

that by then, the government debt burden will likely be higher, the needed

medium-term fiscal adjustment potentially greater, and the inflection point on

the U.S. population's demographics and other age-related spending drivers

closer at hand (see "Global Aging 2011: In The U.S., Going Gray Will Likely

Cost Even More Green, Now," June 21, 2011).

Standard & Poor's

takes no position on the mix of spending and revenue measures that Congress and

the Administration might conclude is appropriate for putting the U.S.'s

finances on a sustainable footing.

The act calls for as much

as $2.4 trillion of reductions in expenditure growth over the 10 years through

2021. These cuts will be implemented in two steps: the $917 billion agreed to

initially, followed by an additional $1.5 trillion that the newly formed

Congressional Joint Select Committee on Deficit Reduction is supposed to

recommend by November 2011. The act contains no measures to raise taxes or

otherwise enhance revenues, though the committee could recommend them.

The act further provides

that if Congress does not enact the committee's recommendations, cuts of $1.2 trillion

will be implemented over the same time period. The reductions would mainly

affect outlays for civilian discretionary spending, defense, and Medicare. We

understand that this fall-back mechanism is designed to encourage Congress to

embrace a more balanced mix of expenditure savings, as the committee might

recommend.

We note that in a letter

to Congress on Aug. 1, 2011, the Congressional Budget Office (CBO) estimated

total budgetary savings under the act to be at least $2.1 trillion over the

next 10 years relative to its baseline assumptions. In updating our own fiscal

projections, with certain modifications outlined below, we have relied on the

CBO's latest "Alternate Fiscal Scenario" of June 2011, updated to

include the CBO assumptions contained in its Aug. 1 letter to Congress. In

general, the CBO's "Alternate Fiscal Scenario" assumes a continuation

of recent Congressional action overriding existing law.

We view the act's

measures as a step toward fiscal consolidation. However, this is within the framework

of a legislative mechanism that leaves open the details of what is finally

agreed to until the end of 2011, and Congress and the Administration could

modify any agreement in the future. Even assuming that at least $2.1 trillion

of the spending reductions the act envisages are implemented, we maintain our

view that the U.S. net general government debt burden (all levels of government

combined, excluding liquid financial assets) will likely continue to grow.

Under our revised base case fiscal scenario--which we consider to be consistent

with a 'AA+' long-term rating and a negative outlook--we now project that net

general government debt would rise from an estimated 74% of GDP by the end of

2011 to 79% in 2015 and 85% by 2021. Even the projected 2015 ratio of sovereign

indebtedness is high in relation to those of peer credits and, as noted, would

continue to rise under the act's revised policy settings.

Compared with previous

projections, our revised base case scenario now assumes that the 2001 and 2003

tax cuts, due to expire by the end of 2012, remain in place. We have changed

our assumption on this because the majority of Republicans in Congress continue

to resist any measure that would raise revenues, a position we believe Congress

reinforced by passing the act. Key macroeconomic assumptions in the base case

scenario include trend real GDP growth of 3% and consumer price inflation near

2% annually over the decade.

Our revised upside

scenario--which, other things being equal, we view as consistent with the

outlook on the 'AA+' long-term rating being revised to stable--retains these

same macroeconomic assumptions. In addition, it incorporates $950 billion of

new revenues on the assumption that the 2001 and 2003 tax cuts for high earners

lapse from 2013 onwards, as the Administration is advocating. In this scenario,

we project that the net general government debt would rise from an estimated

74% of GDP by the end of 2011 to 77% in 2015 and to 78% by 2021.

Our revised downside

scenario--which, other things being equal, we view as being consistent with a

possible further downgrade to a 'AA' long-term rating--features less-favorable

macroeconomic assumptions, as outlined below and also assumes that the second

round of spending cuts (at least $1.2 trillion) that the act calls for does not

occur. This scenario also assumes somewhat higher nominal interest rates for

U.S. Treasuries. We still believe that the role of the U.S. dollar as the key

reserve currency confers a government funding advantage, one that could change

only slowly over time, and that Fed policy might lean toward continued loose

monetary policy at a time of fiscal tightening. Nonetheless, it is possible

that interest rates could rise if investors re-price relative risks. As a

result, our alternate scenario factors in a 50 basis point (bp)-75 bp rise in

10-year bond yields relative to the base and upside cases from 2013 onwards. In

this scenario, we project the net public debt burden would rise from 74% of GDP

in 2011 to 90% in 2015 and to 101% by 2021.

Our revised scenarios

also take into account the significant negative revisions to historical GDP

data that the Bureau of Economic Analysis announced on July 29. From our

perspective, the effect of these revisions underscores two related points when

evaluating the likely debt trajectory of the U.S. government. First, the

revisions show that the recent recession was deeper than previously assumed, so

the GDP this year is lower than previously thought in both nominal and real

terms. Consequently, the debt burden is slightly higher. Second, the revised

data highlight the sub-par path of the current economic recovery when compared

with rebounds following previous post-war recessions. We believe the sluggish

pace of the current economic recovery could be consistent with the experiences

of countries that have had financial crises in which the slow process of debt

deleveraging in the private sector leads to a persistent drag on demand. As a

result, our downside case scenario assumes relatively modest real trend GDP

growth of 2.5% and inflation of near 1.5% annually going forward.

When comparing the U.S.

to sovereigns with 'AAA' long-term ratings that we view as relevant

peers--Canada, France, Germany, and the U.K.--we also observe, based on our

base case scenarios for each, that the trajectory of the U.S.'s net public debt

is diverging from the others. Including the U.S., we estimate that these five

sovereigns will have net general government debt to GDP ratios this year

ranging from 34% (Canada) to 80% (the U.K.), with the U.S. debt burden at 74%.

By 2015, we project that their net public debt to GDP ratios will range between

30% (lowest, Canada) and 83% (highest, France), with the U.S. debt burden at

79%. However, in contrast with the U.S., we project that the net public debt

burdens of these other sovereigns will begin to decline, either before or by

2015.

Standard & Poor's

transfer T&C assessment of the U.S. remains 'AAA'. Our T&C assessment

reflects our view of the likelihood of the sovereign restricting other public

and private issuers' access to foreign exchange needed to meet debt service.

Although in our view the credit standing of the U.S. government has

deteriorated modestly, we see little indication that official interference of

this kind is entering onto the policy agenda of either Congress or the

Administration. Consequently, we continue to view this risk as being highly

remote.

The outlook on the

long-term rating is negative. As our downside alternate fiscal scenario illustrates,

a higher public debt trajectory than we currently assume could lead us to lower

the long-term rating again. On the other hand, as our upside scenario

highlights, if the recommendations of the Congressional Joint Select Committee

on Deficit Reduction--independently or coupled with other initiatives, such as

the lapsing of the 2001 and 2003 tax cuts for high earners--lead to fiscal

consolidation measures beyond the minimum mandated, and we believe they are

likely to slow the deterioration of the government's debt dynamics, the

long-term rating could stabilize at 'AA+'.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.64.69 |

|

|

1 |

Rs.100.79 |

|

Euro |

1 |

Rs.86.30 |

INFORMATION DETAILS

|

Report

Prepared by : |

PRL |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with full

security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.