MIRA

INFORM REPORT

|

Report Date : |

13.02.2013 |

IDENTIFICATION DETAILS

|

Name : |

RELIGARE FINVEST LIMITED (w.e.f. 04.04.2006) |

|

|

|

|

Formerly Known as: |

FORTIS FINVEST LIMITED |

|

|

|

|

Registered Office : |

D3, P3B, District Centre, Saket, New Delhi – 110017, Delhi |

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.03.2012 |

|

|

|

|

Date of Incorporation : |

06.01.1995 |

|

|

|

|

Com. Reg. No.: |

55-64132 |

|

|

|

|

CIN No.: [Company

Identification No.] |

U74999DL1995PLC064132 |

|

|

|

|

TAN No.: [Tax

Deduction & Collection Account No.] |

DELF02758A |

|

|

|

|

PAN No.: [Permanent

Account No.] |

AAFCS6801H |

|

|

|

|

Legal Form : |

A Closely Held Public Limited Liability Company |

|

|

|

|

Line of Business : |

Non Banking Financial Company |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba (45) |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal commitments. |

Satisfactory |

|

Maximum Credit Limit : |

USD 83222580 |

|

|

|

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

Usually Correct |

|

|

|

|

Litigation : |

Clear |

|

|

|

|

Comments : |

Subject is a subsidiary of “RELIGARE ENTERPRISES LTD” It is a well established and reputed company having a satisfactory

track. The External borrowing of the company is huge which may impact the

liquidity position of the company. However, general financial position of the company appears to be

strong. Performance capability appears to be high. Fundamental seems to be

healthy. Trade relations are reported to be fair. Business is active. Payments

are reported to be usually correct and as per commitments. In view of strong holdings and experience promoter the company can be

considered good for normal business dealings at usual trade terms and

conditions. |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – June 30, 2012

|

Country Name |

Previous Rating (31.03.2012) |

Current Rating (30.06.2012) |

|

India |

A1 |

A1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

INDIAN ECONOMIC OVERVIEW

India is developing into an open-market economy, yet traces

of its past autarkic policies remain. Economic liberalization, including

industrial deregulation, privatization of state-owned enterprises, and reduced

controls on foreign trade and investment, began in the early 1990s and has

served to accelerate the country's growth, which has averaged more than 7% per

year since 1997. India's diverse economy encompasses traditional village

farming, modern agriculture, handicrafts, a wide range of modern industries,

and a multitude of services. Slightly more than half of the work force is in

agriculture, but services are the major source of economic growth, accounting

for more than half of India's output, with only one-third of its labor force.

India has capitalized on its large educated English-speaking population to

become a major exporter of information technology services and software

workers. In 2010, the Indian economy rebounded robustly from the global

financial crisis - in large part because of strong domestic demand - and growth

exceeded 8% year-on-year in real terms. However, India's economic growth in

2011 slowed because of persistently high inflation and interest rates and

little progress on economic reforms. High international crude prices have

exacerbated the government's fuel subsidy expenditures contributing to a higher

fiscal deficit, and a worsening current account deficit. Little economic reform

took place in 2011 largely due to corruption scandals that have slowed

legislative work. India's medium-term growth outlook is positive due to a young

population and corresponding low dependency ratio, healthy savings and

investment rates, and increasing integration into the global economy. India has

many long-term challenges that it has not yet fully addressed, including

widespread poverty, inadequate physical and social infrastructure, limited

non-agricultural employment opportunities, scarce access to quality basic and

higher education, and accommodating rural-to-urban migration.

|

Source

: CIA |

EXTERNAL AGENCY RATING

|

Rating Agency Name |

ICRA (Short Term) |

|

Rating |

A1+ |

|

Rating Explanation |

Having very strong degree of safety regarding timely payment of

financial obligation. It carry lowest credit risk. |

|

Date |

September, 2012 |

RBI DEFAULTERS’ LIST STATUS

Subject’s name is not enlisted as a defaulter

in the publicly available RBI Defaulters’ list.

EPF (Employee Provident Fund) DEFAULTERS’ LIST STATUS

Subject’s name is not enlisted as a defaulter in

the publicly available EPF (Employee Provident Fund) Defaulters’ list as of

31-03-2012.

LOCATIONS

|

Registered Office : |

D3, P3B, District Centre, Saket, New Delhi – 110017, Delhi, India |

|

Tel. No.: |

91-11-66325000 |

|

Fax No.: |

91-11-30815288 |

|

E-Mail : |

|

|

Website : |

DIRECTORS

AS ON 01.06.2012

|

Name : |

Mr. Sunil Naraindas Godhwani |

|

Designation : |

Director |

|

Address : |

A – 2, Inayat Farm, Asola Fatehpur Beri, P. O. Mehrauli, New Delhi –

110030, India |

|

Date of Birth/Age : |

10.12.1960 |

|

Date of Appointment : |

29.09.2004 |

|

Email: |

|

|

DIN No.: |

00174831 |

|

|

|

|

Name : |

Mr. Atul Gupta |

|

Designation : |

Director |

|

Address : |

42, Prayag Appartment, B – 1, Vasundhra Enclave, |

|

Date of Birth/Age : |

07.11.1970 |

|

Date of Appointment : |

30.12.2006 |

|

Email : |

|

|

DIN No.: |

00510562 |

|

|

|

|

Name : |

Mr. Jatinder Singh Grewal |

|

Designation : |

Director |

|

Address : |

F – 07, Mittal Park, CHS 44, |

|

Date of Birth/Age : |

25.07.1956 |

|

Date of Appointment : |

15.11.2007 |

|

Email : |

|

|

DIN No.: |

01051943 |

|

|

|

|

Name : |

Mr. Sunil Kumar Garg |

|

Designation : |

Director |

|

Address : |

C – 90, Ramaprastha, |

|

Date of Birth/Age : |

21.10.1968 |

|

Date of Appointment : |

27.09.2007 |

|

Email : |

|

|

DIN No.: |

01179441 |

|

|

|

|

Name : |

Mr. Padam Narain Behl |

|

Designation : |

Director |

|

Address : |

D – 70, |

|

Date of Birth/Age : |

02.10.1951 |

|

Date of Appointment : |

27.09.2007 |

|

DIN No.: |

01314395 |

|

|

|

|

Name : |

Mr. Jaickismin Wadhumal Balani |

|

Designation : |

Director |

|

Address : |

Compas De La |

|

Date of Birth/Age : |

14.11.1948 |

|

Date of Appointment : |

27.09.2007 |

|

DIN No.: |

01338053 |

|

|

|

|

Name : |

Mr. Rama Krishna Shetty |

|

Designation : |

Director |

|

Address : |

D -2, 166, Chartered Cottage, |

|

Date of Birth/Age : |

19.03.1948 |

|

Date of Appointment : |

30.04.2007 |

|

DIN No.: |

01521858 |

|

|

|

|

Name : |

Mr. Vinay Kumar Kaul |

|

Designation : |

Director |

|

Address : |

B – XI, 8202-8204, Vasant Kunj, |

|

Date of Birth/Age : |

06.04.1944 |

|

Date of Appointment : |

24.09.2004 |

|

Email : |

|

|

|

|

|

Name : |

Mr. Kavi Arora |

|

Designation : |

Managing Director & Ceo |

|

Address : |

H.No.356, Espace Nirvana Country, Sector - 50, Gurgaon, 122018,

Haryana |

|

Date of Birth/Age : |

04.11.1970 |

|

Date of Appointment : |

14.11.2011 |

|

DIN No.: |

01429165 |

|

|

|

|

Name : |

Mr. Shachindra Nath |

|

Designation : |

Director |

|

Address : |

C-4, Sarai Khawaja, Green Valley Sector 41-42, Faridabad, 121012, Haryana |

|

Date of Birth/Age : |

13.10.1971 |

|

Date of Appointment : |

14.11.2011 |

|

DIN No.: |

00510618 |

|

|

|

|

Name : |

Mr. Achal Ghai |

|

Designation : |

Director |

|

Address : |

Villa 6, Cluster 40, Jumeirah Islands,, P. O. Box No 18264 Dubai, 018264, , United Arab Emirates |

|

Date of Birth/Age : |

30.08.1963 |

|

Date of Appointment : |

17.11.2011 |

|

DIN No.: |

00312672 |

|

|

|

|

Name : |

Mr. Srinivas Chidambaram |

|

Designation : |

Director |

|

Address : |

S-283, Greater Kailash Part Ii, New Delhi-110048. |

|

Date of Birth/Age : |

21.05.1966 |

|

Date of Appointment : |

23.01.2012 |

|

DIN No.: |

00514665 |

|

|

|

|

Name : |

Mr. Basab Mitra |

|

Designation : |

Director |

|

Address : |

34, Sagarika Chs, Sec – 10/A, Vashi, Navi Mumbai- 400703, Maharashtra |

|

Date of Birth/Age : |

07.06.1969 |

|

Date of Appointment : |

25.04.2012 |

|

DIN No.: |

05166506 |

|

|

|

|

Name : |

Mr. Raghuram Raju |

|

Designation : |

Director |

|

Address : |

B-4/138, Safdarjung Enclave, New Delhi- 110029 |

|

Date of Birth/Age : |

27.10.1962 |

|

Date of Appointment : |

25.04.2012 |

|

DIN No.: |

01741712 |

|

|

|

|

Name : |

Mr. Anil Saxena |

|

Designation : |

Managing Director |

|

Address : |

House No. 603, Aspire – 1, Supertech Emerald Court, Sector - 93a, Noida – 201301 |

|

Date of Birth/Age : |

03.07.1968 |

|

Date of Appointment : |

06.04.2012 |

|

Date of Ceasing As Managing : |

14.11.2011 (Resigned as Managing Director

but continue as Director) |

|

DIN No.: |

01555425 |

|

|

|

|

Name : |

Mr. Dilip Saxena |

|

Designation : |

Director |

|

Address : |

2068/38, Naiwala, Karol Bagh, New Delhi |

|

Date of Birth/Age : |

06.01.1995 |

|

Date of Appointment : |

10.11.1999 |

|

|

|

|

Name : |

Ms. Rajni Rathore |

|

Designation : |

Director |

|

Address : |

B-1124, Shastri Nagar, Delhi-110052 |

|

Date of Birth/Age : |

06.01.1995 |

|

Date of Appointment : |

10.11.1999 |

|

|

|

|

Name : |

Mr. Deepak Saxena |

|

Designation : |

Director |

|

Address : |

231, Dhruv Appts, Patparganj, Delhi |

|

Date of Birth/Age : |

11.04.1997 |

|

Date of Appointment : |

05.10.2000 |

|

|

|

|

Name : |

Ms. Geeta Sethi |

|

Designation : |

Director |

|

Address : |

341-C/A-6, Paschim Vihar, New Delhi-110063 |

|

Date of Birth/Age : |

11.04.1997 |

|

Date of Appointment : |

05.10.2000 |

|

|

|

|

Name : |

Mr. Nikhil Anand |

|

Designation : |

Director |

|

Address : |

A-1/175, Janakpuri, New Delhi-110058 |

|

Date of Appointment: |

01.08.2000 |

|

Date of Ceasing: |

05.07.2004 |

|

|

|

|

Name : |

Mr. Ekeesh Chopra |

|

Designation : |

Director |

|

Address : |

M-85, Guru Harkishan Nagar, Delhi |

|

Date of Birth/Age : |

01.08.2000 |

|

Date of Appointment : |

05.07.2004 |

|

|

|

|

Name : |

Mr. Rajveer Singh |

|

Designation : |

Director |

|

Address : |

S-93, Greater Kailash , Part-I, New Delhi |

|

Date of Birth/Age : |

19.05.2004 |

|

Date of Appointment : |

11.10.2004 |

|

|

|

|

Name : |

Mr. G S Sodhi |

|

Designation : |

Director |

|

Address : |

S-334, Panchsheel Park, New Delhi |

|

Date of Birth/Age : |

19.05.2004 |

|

Date of Appointment : |

11.10.2004 |

|

|

|

|

Name : |

Mr. Malvinder Mohan Singh |

|

Designation : |

Director |

|

Address : |

1a Lady Hill Road # 03-01 Shangri – La Residences, Singapore 258685 |

|

Date of Birth/Age : |

27.11.1972 |

|

Date of Appointment : |

11.10.2004 |

|

Date of Ceasing: |

19.12.2005 |

|

|

|

|

Name : |

Mr. Shivinder Mohan Singh |

|

Designation : |

Director |

|

Address : |

1, Rajesh Pilot Lane, New Delhi – 110011 |

|

Date of Birth/Age : |

21.07.1975 |

|

Date of Appointment : |

11.10.2004 |

|

Date of Ceasing: |

11.01.2006 |

|

|

|

|

Name : |

Mr. Yuvraj Narain |

|

Designation : |

Director |

|

Address : |

Narain Niwas 1, Basheer Bagh Lane Village - Shahurpur (Mehrauli), New

Delhi – 110030 |

|

Date of Birth/Age : |

16.11.1956 |

|

Date of Appointment : |

11.01.2006 |

|

Date of Ceasing: |

30.12.2006 |

KEY EXECUTIVES

|

Name : |

Punit Arora |

|

Designation : |

Company Secretary |

|

Address : |

315, Nagin Lake Appartments, Paschim Vihar, New Delhi-110087 |

|

Date of Birth/Age : |

12.012.1976 |

|

Date of Appointment : |

01.11.2006 |

|

|

|

|

Name : |

Atul Gupta |

|

Designation : |

Manager |

|

Address : |

42, Prayag Appartment, B-1, Vasundhra Enclave, New Delhi- 110096. |

|

Date of Birth/Age : |

07.11.1970 |

|

Date of Appointment : |

25.03.2006 |

|

Date of Ceasing: |

30.12.2006 |

MAJOR SHAREHOLDERS / SHAREHOLDING PATTERN

LIST OF EQUITY SHARE

HOLDERS AS ON 01.06.2012

|

Names of

Shareholders |

Address |

No. of Shares |

|

Religare Enterprises Ltd

/ N.A. |

D3, P3B, District Centre,

Saket, New Delhi-110017 |

173321537 |

|

Malvinder Mohan Singh*

S/o Late Dr. Parvinder Singh |

1A Lady Hill Road # 03-01

Shangri - LA Residences, Singapore 258685 |

100 |

|

Shivinder Mohan Singh*

S/o Late Dr. Parvinder Singh |

1, Rajesh Pilot Lane, New

Delhi - 110011 |

100 |

|

Japna Malvinder Singh*

W/o Sh. Malvinder Mohan Singh |

1, Rajesh Pilot Lane, New

Delhi - 110011 |

100 |

|

Aditi Shivinder Singh*

S/o Shivinder Mohan Singh |

1, Rajesh Pilot Lane, New

Delhi - 110011 |

100 |

|

Gurkirat Singh Dhillon*

S/o Gurinder Singh Dhillon |

Dera Baba Jaimal Singh,

Beas, Amritsar(Punjab) |

100 |

|

Gurpreet Singh* S/o Gurinder Singh

Dhillon |

Dera Baba Jaimal Singh,

Beas, Amritsar(Punjab) |

100 |

|

Avigo PE Investments Ltd,

Mauritius/N.A. |

355, NeXTeracom Tower 1, 3rd

Floor, Cybercity Ebene ,Mauritius |

30 |

|

NYLIM Jacob Ballas India

Fund III, LLC/N.A. |

IFS Court, Twenty Eight ,

Cybercity Ebene, Mauritius |

20 |

LIST OF PREFERENCE

SHAREHOLDERS AS ON 01.06.2012

|

Names of Shareholders |

Address |

No. of Shares |

|

ICICI Bank Limited / N.A. |

ICICI Bank Towers, NBCC

Place, Bhishma Pitamah Marg, Pragati Vihar, New Delhi - 110 003, India |

112,500,000 Non- Convertible Preference Shares |

|

Avigo PE Investments Ltd,

Mauritius/N.A. |

355, NeXTeracom Tower 1,

3rd Floor, Cybercity Ebene ,Mauritius |

19,999,960 Compulsorily Convertible Preference Shares |

|

NYLIM Jacob Ballas India Fund III, LLC/N.A. |

IFS Court, Twenty Eight ,

Cybercity Ebene, Mauritius |

26,666,640 Compulsorily Convertible Preference Shares |

LIST OF ALLOTTEES AS ON 27.01.2012 (EQUITY)

|

Names of Allottees |

Address |

No. of Shares |

|

NYLIM Jacob Ballas India Fund III, LLC |

IFS Court, Twenty Eight, Cybercity, Ebene,

Mauritius |

2000 |

|

|

|

|

AS ON 27.01.2012 (COMPULSORILY CONVERTIBLE PREFERENCE SHARES)

|

Names of Allottees |

Address |

No. of Shares |

|

NYLIM Jacob Ballas India Fund III, LLC |

IFS Court, Twenty Eight, Cybercity, Ebene,

Mauritius |

26666640 |

AS ON 01.06.2012

|

Category |

Percentage |

|

Directors or relatives of Directors |

100.00 |

|

Total |

100.00 |

BUSINESS DETAILS

|

Line of Business : |

Non Banking Financial Company |

GENERAL INFORMATION

|

No. of Employees : |

Not Available |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

Bankers : |

· Axis Bank Limited, 2nd Floor, Statesman House, 148, Barakhamba Road, New Delhi - 110001, Delhi, India ·

UTI Bank Limited, Trishul 3rd Floor Opp

Samartheshwar Temple, Law Garden Ellisbridge, Ahmedabad - 380006, Gujarat,

India |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

Facilities : |

|

|

|

|

|

Banking

Relations : |

-- |

|

|

|

|

Auditors : |

|

|

Name : |

Price Waterhouse Chartered Accountant |

|

Address : |

252, Veer Savarkar Marg Shivaji Park, Dadar Mumbai 400028,

Maharashtra, India |

|

|

|

|

Holding Company : |

Religare Enterprises Limited |

|

|

|

|

Subsidiaries : |

Religare Housing Development Finance Corporation Limited |

CAPITAL STRUCTURE

AS ON 31.03.2012

Authorised Capital :

|

No. of Shares |

Type |

Value |

Amount |

|

190833400 |

Equity Shares |

Rs.10/- |

Rs.1908.334 Millions |

|

12500000 |

Non

Convertible Cumulative Redeemable Preference Shares |

Rs.10/- |

Rs.125.000 Millions |

|

46666600 |

Compulsorily

Convertible Preference Shares |

Rs.10/- |

Rs.446.666 Millions |

|

|

|

|

|

Issued, Subscribed & Paid-up Capital :

|

No. of Shares |

Type |

Value |

Amount |

|

173322187 |

Equity Shares |

Rs.10/- |

Rs.1733.221 Millions |

|

11250000 |

1 % Non

Convertible Cumulative Redeemable Preference Shares |

Rs.10/- |

Rs.112.500

Millions |

|

46666600 |

0.01%

Compulsorily Convertible Preference Shares |

Rs.10/- |

Rs.466.666

Millions |

|

|

|

|

|

|

Particulars |

31.03.2012 |

|

|

|

Number of Shares |

Amount in Millions |

|

Authorized

Equity Shares of 10/- each Balance as at the beginning of

the year Reclassified into Non

Convertible Cumulative Redeemable Preference Shares of Rs. 10/- each Reclassified Into Compulsorily Convertible

Preference Shares of Rs. 10/-each |

250000000 12500000 46666600 |

2500.000 125.000 466.666 |

|

Balance

as at the end of the year (A} |

190833400 |

1908.334 |

|

Non

Convertible Cumulative Redeemable Preference Shares of Rs. 10/- each |

|

|

|

Balance as at the beginning of

the year Reclassified from Equity Shares

of Rs. 10/- each |

0.000 12500000 |

0.000 125.000 |

|

Balance

as It the end of the year (B) |

12500000 |

125.000 |

|

Comoulsorilv

Convertible Preference Shares of Rs. 10/- each |

|

|

|

Balance as at the beginning of

the year Reclassified from Equity Shares

of Rs. 10/- each |

0.000 46666600 |

0.000 466.666 |

|

Balance

as at the end of the year ( C) |

46666600 |

466.666 |

|

Balance

as at the end of the year (A+B+C) |

250000000 |

2500.000 |

|

Issued, Subscribed & Paid-up Capital Equity Shares of Rs. 10/- each Balance as at the beginning of

the year Add: Shares Issued during the

year |

173322137 50 |

1733.221 0.000 |

|

Balance

as at the end of the year {A) |

173322187 |

1733.221 |

|

1 % Non Convertible Cumulative Redeemable Preference

Shares Balance as at the beginning of

the year Add: Shares Issued during the

year Less: Redemption of Preference

shares |

0.000 12500000 1250000 |

0.000 125.000 12.500 |

|

Balance as

at the beginning of the year (B) |

11250000 |

112.500 |

|

0.01% Compulsorily Convertible Preference Shares Balance as at the beginning of

the year Add: Shares Issued during the

year |

0.000 46666600 |

0.000 466.666 |

|

Balance as

at the end of the year (C) |

46666600 |

466.666 |

|

Balance

as at the end of the year (A+B+C) |

231238787 |

2312.387 |

FINANCIAL DATA

[all figures are

in Rupees Millions]

ABRIDGED BALANCE

SHEET

|

SOURCES OF FUNDS |

31.03.2012 |

31.03.2011 |

31.03.2010 |

|

|

SHAREHOLDERS FUNDS |

|

|

|

|

|

1] Share Capital |

2312.387 |

1733.221 |

1703.221 |

|

|

2] Share Application Money |

0.000 |

0.000 |

0.000 |

|

|

3] Reserves & Surplus |

18493.258 |

14368.115 |

12953.532 |

|

|

4] (Accumulated Losses) |

0.000 |

0.000 |

0.000 |

|

|

NETWORTH |

20805.645 |

16101.336 |

14656.753 |

|

|

LOAN FUNDS |

|

|

|

|

|

1] Secured Loans |

72180.115 |

40915.311 |

9977.095 |

|

|

2] Unsecured Loans |

32023.141 |

37823.552 |

32834.135 |

|

|

TOTAL BORROWING |

104203.256 |

78738.863 |

42811.230 |

|

|

DEFERRED TAX LIABILITIES |

0.000 |

0.000 |

5.857 |

|

|

|

|

|

|

|

|

TOTAL |

125008.901 |

94840.199 |

57473.840 |

|

|

|

|

|

|

|

|

APPLICATION OF FUNDS |

|

|

|

|

|

|

|

|

|

|

|

FIXED ASSETS [Net Block] |

540.890 |

630.590 |

642.779 |

|

|

Capital work-in-progress |

188.469 |

161.584 |

43.663 |

|

|

|

|

|

|

|

|

INVESTMENT |

3287.425 |

1571.594 |

5358.253 |

|

|

DEFERREX TAX ASSETS |

265.994 |

81.520 |

0.000 |

|

|

|

|

|

|

|

|

CURRENT ASSETS, LOANS & ADVANCES |

|

|

|

|

|

|

Inventories |

2856.325

|

4853.337 |

6858.370 |

|

|

Sundry Debtors |

431.125

|

1812.481 |

3841.963 |

|

|

Cash & Bank Balances |

14631.077

|

10046.881 |

2184.068 |

|

|

Other Current Assets |

1990.870

|

733.694 |

235.695 |

|

|

Loans & Advances |

127362.225

|

90574.831 |

41420.241 |

|

Total

Current Assets |

147271.622

|

108021.224 |

54540.337 |

|

|

Less : CURRENT

LIABILITIES & PROVISIONS |

|

|

|

|

|

|

Sundry Creditors |

463.267

|

10.095 |

404.670 |

|

|

Other Current Liabilities |

23688.685

|

15000.446 |

2481.325 |

|

|

Provisions |

2393.547

|

615.772 |

225.197 |

|

Total

Current Liabilities |

26545.499

|

15626.313 |

3111.192 |

|

|

Net Current Assets |

120726.123

|

92394.911 |

51429.145 |

|

|

|

|

|

|

|

|

MISCELLANEOUS EXPENSES |

0.000 |

0.000 |

0.000 |

|

|

|

|

|

|

|

|

TOTAL |

125008.901 |

94840.199 |

57473.840 |

|

PROFIT & LOSS

ACCOUNT

|

|

PARTICULARS |

31.03.2012 |

31.03.2011 |

31.03.2010 |

|

|

|

SALES |

|

|

|

|

|

|

|

Income |

18213.090 |

11029.722 |

4620.175 |

|

|

|

Other Income |

374.065 |

601.414 |

741.471 |

|

|

|

TOTAL (A) |

18587.155 |

11631.136 |

5361.646 |

|

|

|

|

|

|

|

|

Less |

EXPENSES |

|

|

|

|

|

|

|

Employees Benefit |

1084.802 |

1075.428 |

693.892 |

|

|

|

Others Expenses |

2760.199 |

2237.385 |

1435.286 |

|

|

|

TOTAL (B) |

3845.001 |

3312.813 |

2129.178 |

|

|

|

|

|

|

|

|

Less |

PROFIT

BEFORE INTEREST, TAX, DEPRECIATION AND AMORTISATION (A-B) (C) |

14742.154 |

8318.323 |

3232.468 |

|

|

|

|

|

|

|

|

|

Less |

FINANCIAL

EXPENSES (D) |

12688.635 |

6456.824 |

1770.479 |

|

|

|

|

|

|

|

|

|

|

PROFIT

BEFORE TAX, DEPRECIATION AND AMORTISATION (C-D) (E) |

2053.519 |

1861.499 |

1461.989 |

|

|

|

|

|

|

|

|

|

Less/ Add |

DEPRECIATION/

AMORTISATION (F) |

100.329 |

99.890 |

43.131 |

|

|

|

|

|

|

|

|

|

|

PROFIT BEFORE

TAX (E-F) (G) |

1953.190 |

1761.609 |

1418.858 |

|

|

|

|

|

|

|

|

|

Less |

TAX (I) |

574.964 |

613.864 |

390.577 |

|

|

|

|

|

|

|

|

|

|

PROFIT AFTER TAX

(G-I) (J) |

1378.226 |

1147.745 |

1028.281 |

|

|

|

|

|

|

|

|

|

|

Earnings Per

Share (Rs.) |

7.75 |

6.66 |

-- |

|

KEY RATIOS

|

PARTICULARS |

|

31.03.2012 |

31.03.2011 |

31.03.2010 |

|

PAT / Total Income |

(%) |

7.41

|

9.87 |

19.18 |

|

|

|

|

|

|

|

Net Profit Margin (PBT/Sales) |

(%) |

10.72

|

15.97 |

30.71 |

|

|

|

|

|

|

|

Return on Total Assets (PBT/Total Assets} |

(%) |

1.32

|

1.62 |

2.57 |

|

|

|

|

|

|

|

Return on Investment (ROI) (PBT/Networth) |

|

0.09

|

0.10 |

0.09 |

|

|

|

|

|

|

|

Debt Equity Ratio (Total Debt/Networth) |

|

5.00

|

4.89 |

2.92 |

|

|

|

|

|

|

|

Current Ratio (Current Asset/Current Liability) |

|

5.55

|

6.91 |

17.53 |

LOCAL AGENCY FURTHER INFORMATION

|

Sr. No. |

Check List by Info Agents |

Available in

Report (Yes / No) |

|

1] |

Year of Establishment |

Yes |

|

2] |

Locality of the firm |

Yes |

|

3] |

Constitutions of the firm |

Yes |

|

4] |

Premises details |

Yes |

|

5] |

Type of Business |

Yes |

|

6] |

Line of Business |

Yes |

|

7] |

Promoter's background |

Yes |

|

8] |

No. of employees |

No |

|

9] |

Name of person contacted |

No |

|

10] |

Designation of contact

person |

No |

|

11] |

Turnover of firm for last

three years |

Yes |

|

12] |

Profitability for last

three years |

Yes |

|

13] |

Reasons for variation

<> 20% |

-------- |

|

14] |

Estimation for coming

financial year |

No |

|

15] |

Capital in the business |

Yes |

|

16] |

Details of sister

concerns |

Yes |

|

17] |

Major suppliers |

No |

|

18] |

Major customers |

No |

|

19] |

Payments terms |

No |

|

20] |

Export / Import details

(if applicable) |

No |

|

21] |

Market information |

---------------------- |

|

22] |

Litigations that the firm

/ promoter involved in |

---------------------- |

|

23] |

Banking Details |

Yes |

|

24] |

Banking facility details |

Yes |

|

25] |

Conduct of the banking

account |

---------------------- |

|

26] |

Buyer visit details |

No |

|

27] |

Financials, if provided |

Yes |

|

28] |

Incorporation details, if

applicable |

Yes |

|

29] |

Last accounts filed at

ROC |

Yes |

|

30] |

Major Shareholders, if

available |

Yes |

|

31] |

Date of Birth of

Proprietor/Partner/Director, if available |

Yes |

|

32] |

PAN of

Proprietor/Partner/Director, if available |

No |

|

33] |

Voter ID No of Proprietor/Partner/Director,

if available |

No |

|

34] |

External Agency Rating,

if available |

Yes |

OVERVIEW

Subject was incorporated on

6th January, 1995 as Skylark Securities Private Limited. The name of The

Subject was changed from Skylark Securities Private Limited to Fortis Finvest

Private Limited on 23rd September, 2004. The Subject was convened into a public

limited Subject on 07th October, 2004 and the name was changed Fortis

Finvest Limited. Further, on 4th April, 2006 the name of

the Subject was changed to Religare Finvest Limited {the 'Subject).

The Subject is holding

Certificate of Registration (CoR) as Non-Banking Financial Institution, without

accepting public deposits, registered with the Reserve Bank of India

("RBI") under section 45-IAof the Reserve Bank of India Act, 1934 and

primarily engaged in lending, investment, financial advisory services and

distribution of third party financial products. The Subject received the CoR from RBI initially on 03rd January,

2001 as category B Non-Deposit taking Non-Banking Financial Institution and

consequently upon change in name of the Subject , RBI issued a fresh CoR on

10th November, 2006 enabling the subject to carry on the business as a

Non-Deposit taking Category B Non Banking Financial Institution.

RESULTS OF

OPERATIONS

The revenue of the Subject has increased from Rs. 11,631.14 million in

F.Y. 2010-11 to Rs.18,587.16 million in F.Y. 2011-12, translating to growth of

60 % over the previous financial year. Profit before Tax increased from Rs.

1,761.61 million to Rs. 1,953.19 million, an increase of 11% over the previous

financial year. The Net Profit after Tax also increased from Rs. 1,147.75

million to Rs. 1,378.23 million, a growth of 20 % over the previous financial

year. After growing itslending book largely from its own equity during

FY2009-10, the Subject had increasingly relied on borrowed funds for growth of

the balance sheet in FY2010-11 and this was further accentuated in FY2011-12.

Furthermore, the nature of the Subject ’s business is such thatduring a period

rising interest rates as witnessed during FY2011-12, the cost of borrowings

increases quickly but there is a lag in raising interest rates to customers.

Consequently, in FY2011-12, interest expenses grew faster than interest income

and correspondingly, PAT growth was not as fast as revenue growth.

BUSINESS OVERVIEW

AND FUTURE OUTLOOK

The Small and Medium Enterprises (SME) sector can be

regarded as the backbone of India’s economy as it generates higher number of

jobs per unit of capital employed than other sectors and accounts for a very

high share of output and exports: it is estimated that the sector provides

employment to around 60 million people, accounts for about 45% of the

manufacturing output and generates around 40% of the country’s exports. A 2009

study by ASSOCHAM had estimated that the SME sector will contribute around 22%

to India’s GDP in 2012 as against around 17% in 2010 and indications are that

this level of share in GDP will be achieved by the SME sector. The same study

had pegged the SME financing opportunity at Rs. 500 billion and Religare

Finvest Limited (RFL) continues to target this opportunity.

RFL’s suite of SME-centric products includes SME-Loans

against Property (LAP), SME-Commercial Assets finance (comprising commercial

vehicle finance and construction equipment finance) and SME-Working Capital

Finance. While the products may be identified by the nature of security offered

(as in the case of LAP), RFL focuses on loans that have enhancement of

productive capacity rather than consumption as their end-use. One of their

strengths in this business is their understanding of the psyche of

entrepreneurs – this has been institutionalised in the form of a proprietary

credit scoring model that they believe is not easily replicable and gives them

a competitive advantage. Their scoring model allows them to make credit

decisions that are neither conservative nor aggressive. They have restricted

delinquencies to levels that are the envy of their peers: at the end of FY12,

accounts (for Asset Finance Segment) that were 30

days past due (DPD) were 2.33% and 90 DPD were just 0.73% of outstanding loans.

Their constant focus on operating efficiencies has translated to an Operating

Expenses to Average Net Receivables ratio for the Asset Finance segment of just

1.45% for the fourth quarter of Financial Year ended 2012.

These levels of operating expenses are near benchmark

levels in the industry and their peer group and they will continue to improve

it further. RFL has established a presence in all the important SME clusters

across India and as of March 31, 2012, had 37 branches in 15 states. The size

of their Asset Finance book stood at Rs.84 billion as on March 31, 2012, or

practically twothirds of RFL’s overall book size; 90% of these loans are

secured.

In addition to SME financing which is the core focus, RFL

provides Capital Market Finance (comprising Loans Against Shares to promoters

as well as retail investors, ESOP financing and IPO financing), which

complements the services offered by RSL; and Corporate Lending, which allows

them to profitably park temporary surpluses. They had deployed Rs. 23.2 billion

and Rs. 18.5 billion in Capital Market Finance and Corporate Lending

respectively, as of March 31, 2012. RFL continues to maintain a strong balance

sheet. Their net worth as of March 31, 2011 stood at Rs. 20.8 billion. The

ratings assigned to their debt are a testament to the strength of their balance

sheet. ICRA has assigned the highest rating [ICRA] ‘A1+’ to their short term

debt for an amount of Rs. 50 billion; a rating of [ICRA]‘AA-’ to long term debt

for an amount of Rs. 25 billion, a rating of [ICRA]‘AA-’ to long term bank

loans for an amount of Rs. 73.5 billion, a rating of [ICRA]’A1+’ to short term

bank loans for an amount of Rs. 6 bn and a rating of [ICRA]’A+’ to

Non-Convertible Cumulative Redeemable Preference Shares for an amount of Rs.

1,250 mn. Additionally, CARE has assigned a rating of ‘CARE AA-’ to RFL’s long

term debt for an amount of Rs. 15 billion and FITCH has assigned a rating of

‘AA-(Ind)’ to RFL’s Tier-II subordinate debt program for an amount of Rs. 4.5

billion.

As they stand at the threshold of a massive opportunity, their conviction

is that their proprietary knowledge of the SME sector and their credit needs

will stand them in good stead and allow them to profitably serve this

systemically important sector.

NOTE:

The registered office address of the company has been shifted from 55 hanuman Road, Connaught Circus, New Delhi – 110001, Delhi, India to 3rd Floor, Devika Tower, 6 Nehru Place, New Delhi – 110019, Delhi, India w.e.f. 01.03.2006

The registered office address of the company has been

shifted from

3rd Floor, Devika Tower, 6 Nehru Place, New Delhi – 110019, Delhi to

19 Nehru Place, New Delhi 110019, Delhi, India w.e.f. 30.01.2009

The registered office address of the company has been shifted from 19 Nehru Place, New Delhi 110019,

Delhi, India to present address w.e.f. 21.01.2010

FORM 8:

|

Corporate

identity number of the company |

U74999DL1995PLC064132 |

|

Name of the

company |

RELIGARE FINVEST

LIMITED |

|

Address of the

registered office or of the principal place of business in |

D3, P3B,District

Centre, Saket New Delhi – 110017, Delhi, India |

|

This form is for |

Modification of

charge |

|

Type of charge |

Book Debts |

|

Particular of

charge holder |

Axis Bank Limited

|

|

Nature of

instrument creating charge |

Supplemental Deed

Of Hypothecation |

|

Date of

instrument Creating the charge |

10.01.2013 |

|

Amount secured by

the charge |

Rs.2500.000

Millions |

|

Brief of the

principal terms an conditions and extent and operation of the charge |

Margin Pari Passu Charge. |

|

Short particulars

of the property charged |

First Pari Passu

Charge On The Standard Assets Portfolio Of Receivables With A Cover Of At

Least 1.25 Times Along With Other Lenders. |

|

Date of

instrument modifying the charge |

15.03.2011 |

|

Particulars of

the present modification |

Term Loan Of Rs

3000.000 Millions (Out Of Rs. 3500.000 Millions) Shall Stand Modified To Rs.

2000.000 Millions, Due To Novation/Transfer Of Loan Of Rs. 1000.000 Millions

In Favour Of State Bank Of Travancore By The Bank And Total Charge Shall

Stand Modified To Rs.2500.000 Millions And Shall Continued To Be Secured By

First Pari Passu Charge Over All Present And Future Receivables Of The

Company. |

PRESS RELEASE:

JACOB BALLAS TO INVEST RS200 CRORE IN RELIGARE

FINVEST LIMITED

02/01/2012 06:10 PM

Religare Finvest currently has

more than 25,000 MSME accounts and its loan book stands at Rs.11,3800.000

Millions.

Religare Finvest Limited (RFL), one of India’s largest capitalized NBFCs and a

subsidiary of Religare Enterprises Limited, announced that NYLIM Jacob Ballas

India Fund III LLC (Jacob Ballas Fund) has agreed to invest Rs2000.000 Millions

in the form of compulsory convertible preference shares. This will be the

second equity investment in the company (RFL) in quick

succession with Avigo Capital having invested Rs1500.000 Millions in November

2011. Religare Finvest provides debt capital to MSMEs

in the form of loans against property, working capital loans,

loans against plant and machinery, vehicles and construction equipment and loan

against marketable securities among others. Religare Finvest currently has more

than 25,000 MSME accounts and its loan book stands at Rs11,3800.000 Millions

(as on 30 September 2011).

Jacob Ballas Fund is advised by Jacob Ballas Capital India Private Limited

("JBC", www.jbindia.co.in ), a leading private

equity advisor based in New Delhi, India with a 19 member team, advising

three India focused Mauritius based private equity funds.

Investors in the Funds comprise predominantly leading international

institutions such as insurance companies, sovereign wealth funds, pension

funds, banks, funds of funds as well as reputed international family investment

offices. The Funds have generated ten liquidity events from its portfolio

including full and partial exits.

Commenting on this development, Shachindra Nath, group CEO, Religare

Enterprises Ltd said, “We are pleased to announce this capital infusion by

Jacob Ballas in Religare Finvest Limited. This investment is not only an

external endorsement of the operating model but also demonstrates that despite

macro headwinds in challenging times there are value seeking investors for

fundamentally strong business models. Our NBFC, led by a strong leadership team

over the last three years has created a unique MSME focused operating model

backed by strong underwriting capabilities. This move also positions

us well to capitalize on the existing business opportunities

while delivering superlative value for all our stakeholders.”

REGULATORY

OVERHANG EASES FOR NBFCS: INDIA RATINGS

January 31, 2013 at 18.58

India Ratings has maintained a

stable outlook on the major non-bank finance companies (NBFCs) sector in 2013.

This is because major NBFCs' robust pre-provision operating profit (PPOP)

provides a strong cushion against rising credit costs and elevated funding

costs.

India Ratings has maintained a stable outlook on the major non-bank

finance companies (NBFCs) sector in 2013. This is because major NBFCs' robust

pre-provision operating profit (PPOP) provides a strong cushion against rising

credit costs and elevated funding costs, while there will be only limited

impact of proposed regulatory changes on these companies.

Softening interest rates and the expected uptick in economic growth will ease

off cyclical pressures in 2013. However, the continued harsh operating

environment around some key asset classes, including heavy and medium

commercial vehicles (a key segment for many major NBFCs) and construction

equipment, and building pressure points in the fast-growing light commercial

vehicles will keep asset quality under pressure. Funding costs will remain high

due to the regulatory changes implemented in last two years. The agency expects

return on average assets to range between 2.3%-2.5% in 2013 (FY12: 2.7%).

India Ratings' stress test on the major NBFCs - which considers scenarios of

multi-fold increase in non-performing loans and a significant increase in

funding costs - shows strong resilience of PPOP at the aggregated level in

absorbing stressed credit and funding costs.

In India Ratings' view, NBFCs' high dependence on banks could increase

in 2013 on account of the new 30% sectoral caps on mutual funds' debt investments

(another key channel of funding for NBFCs). Despite softening interest rates,

funding costs will remain elevated from the exclusion of bank loans to NBFCs

from priority sector lending and restrictions on bilateral assignments. Net

interest margin is estimated to drop to 5.9% (FY12: 6.1%).

India Ratings believes the new draft guidelines on NBFCs proposed by the

Reserve Bank of India (RBI) in December 2012 (based on the Usha Thorat

Committee Report) will strengthen the NBFC sector fundamentally in the

long-term. The proposed enhancements in disclosure standards and corporate

governance will increase transparency and improve investor confidence and its

access to capital markets for large NBFCs (which are subject to most of these

stricter requirements). The financial impact of the proposed revisions in asset

classification, provisioning norms and tighter liquidity requirements will be

manageable. Small NBFCs though could see increased consolidation from the

proposed requirement of asset size of INR250m for registration with the RBI.

A special report "2013 Outlook: Major Non-Bank Finance Companies -

Stable, but Strong Headwinds Remain"

RELIGARE FINVEST SELLS 39.30 LK SHARES OF

CONFIDENCE PETRO

January 18, 2013 at 08.15

On January 17, 2013 Religare Finvest Ltd sold 3,930,000 shares of Confidence Petroleum at Rs 2.35 on the BSE. In the previous trading session, the share closed at Rs 3.39, up Rs 0.51, or 17.71%. It has touched a 52-week low of Rs 2.31.

On January 17, 2013 Religare Finvest Ltd sold 3,930,000 shares of Confidence Petroleum at Rs 2.35 on the BSE.

In the previous trading session, the share closed at Rs 3.39, up Rs 0.51, or 17.71%. It has touched a 52-week low of Rs 2.31.

The company's trailing 12-month (TTM) EPS was at Rs 1.75 per share. (Sep, 2012). The stock's price-to-earnings (P/E) ratio was 1.94. The latest book value of the company is Rs 8.40 per share. At current value, the price-to-book value of the company was 0.4.

RELIGARE FINVEST LIMITED TO RAISE UPTO RS.

5,000 MILLION THROUGH PUBLIC ISSUE OF SECURED REDEEMABLE NON CONVERTIBLE

DEBENTURES

MUMBAI, September 11, 2012: Religare Finvest Limited (“RFL” or “Company”

or “Issuer”), a systematically important non-deposit accepting Non-Banking

Finance Company (NBFC) registered with the RBI and a subsidiary of Religare

Enterprises Limited (“REL” or the “Promoter”), proposes a public issue of

Secured Redeemable Non-Convertible Debentures of face value of Rs. 1,000 each,

(“NCDs”), aggregating upto Rs. 2,500 Million with an option to retain

over-subscription of upto Rs. 2,500 Million, for issuance of additional NCDs

aggregating to a total of upto Rs. 5,000 Million hereinafter referred to as the

“Issue”.

The Issue is

scheduled to open for subscription on Friday, September 14, 2012 and close on

September 27, 2012* (both days inclusive). Applicants of the NCDs will be

allocated on first come first serve basis (determined on the basis of the

upload of each Application into the electronic book of the Stock Exchanges).

The NCDs are proposed to be listed on the BSE Limited, (“BSE”) and National

Stock Exchange of India Limited. BSE shall be the Designated Stock Exchange.

The net proceeds of

the Issue (i.e.; after meeting the expenditures of and related expenses) will

be used for various financing activities including lending and investments,

subject to applicable statutory and/or regulatory requirements, to repay our

existing debt and towards our business operations including for our capital

expenditure and working capital requirements.

The minimum

application size for the Issue is Rs. 10,000 or 10 NCDs of face value of Rs.

1,000 each (for all Series of NCDs, namely Series I, Series II, Series III,

Series IV and Series V either taken individually or collectively). The NCDs

offered through this Issue are of varying tenures of 36 months and one day, 60

months, 70 months and 72 months. The NCDs offers annualised returns upto

12.6184%**. The NCDs with a tenure of 70 months and 72 months (ie. Series V),

which offers only the cumulative option, will double the investment in less

than 6 years**.

The NCDs proposed to

be issued under this Issue have been rated ‘[ICRA] AA-(negative)’ by ICRA for

an amount of up to Rs 5000.000 Millions and ‘CARE AA-’ by CARE for an amount of

upto Rs 5000.000 Millions. The rating of the NCDs by both ICRA and CARE

indicate high degree of safety regarding timely servicing of financial

obligations and carrying very low credit risk.

Axis Bank Limited,

A. K. Capital Services Limited, JM Financial Institutional Securities Private

Limited, Kotak Mahindra Capital Company Limited and Religare Capital Markets

Limited^ are the Lead Managers to the Issue. Link Intime India Private Limited

is the Registrar to the Issue.

About Religare

Finvest Ltd – www.religarefinvest.com

RFL is a

systemically important non-deposit accepting NBFC, focusing on small and medium

enterprises (SME) and retail capital market financing. RFL offers a diversified

and broad suite of lending products to its SME, retail and other customers.

Through its reach and focus on the SME segment and their broad product

offering, RFL provides debt capital to power the growth of the small and medium

enterprises, the back bone of India’s economy.

RFL’s lending

products aimed at providing financing to the SME segment include: Loan against

Property, Loan against/for Commercial Assets, Loan against Marketable

Securities, and Working Capital Loans – Secured and Unsecured; while its retail

capital market financing includes Loan against Securities; and Employee stock

option funding

As on March 31,

2012, SME finance and retail capital market finance activities accounted for

70% and 13% of its total loan book respectively. Corporate lending represented

15% of our loan book as on March 31, 2012 and corporate auto lease represented

2% of our loan book as on March 31, 2012. Further, its SME finance comprises of

loans against property representing 47% of its total loan book as on March 31,

2012, commercial assets loans (commercial vehicle and construction equipment

finance) representing 10% of its total loan book as on March 31, 2012, SME

working capital financing representing 8% of its total loan book as on March

31, 2012 and loans against marketable securities representing 13% of its total

loan book as on March 31, 2012. Its retail capital market finance comprises of

loans against securities representing 13% of our total loan book as on March

31, 2012.

The Company’s Income

from Operations and Net Profit After Tax (PAT) for the financial year ended

March 31, 2012 was Rs. 18213.100 Millions and 1378.200 Millions, respectively.

Its Income from Operations and Profit After tax has grown at a CAGR of 98% and

16% respectively over the last three fiscal years. Its Loan Book has grown at a

CAGR of 75% over the last three fiscal years. The aggregate loan book as at

March 31, 2012 was Rs. 12,5735.900 Millions. The Company’s employee strength as

on June 30, 2012 was 1,018.

Religare Finvest

Limited, (“Company”), is proposing, subject to receipt of requisite approvals,

market conditions and other considerations, a public issue of its securities

and has filed a prospectus, (“Prospectus”), with the Registrar of Companies,

N.C.T. of Delhi and Haryana, the Securities and Exchange Board of India, the

BSE Limited, (“BSE”) and the National Stock Exchange of India Limited, (“NSE”).

The Prospectus is available on the website of the BSE at www.bseindia.com, the

NSE at www.nseindia.com, the Company at www.religarefinvest.com and respective

websites of the Lead Managers to the Issue at www.axisbank.com,

www.akcapindia.com, www.jmfl.com, investmentbank.kotak.com and religarecm.com.

Investors should note that investment in debt securities involves a high degree

of risk and for details relating to the same, please see the section entitled

“Risk Factors” on page 1 of the Prospectus. Investors are urged to take any

decision to invest in the debt securities issued pursuant to the Prospectus

solely on the basis of the disclosures made therein.

The company is

having a valid Certificate of Registration dated 10 November 2006 issued by the

Reserve Bank of India under Section 45 IA of the Reserve Bank of India Act,

1934. However, the RBI does not accept any responsibility or guarantee about

the present position as to the financial soundness of the company or for the

correctness of any of the statements or representations made or opinions

expressed by the company and for repayment of deposits/discharge of liabilities

of the Company.

* The Issue may

close on such earlier date or extended date as may be decided at the discretion

of the duly authorized committee of Directors of our Company subject to

necessary approvals. For further information on the Issue programme, please

refer to “General Information – Issue Programme” page 36 of the Prospectus. In

the event of such early closure or extension of the Issue, our Company shall

ensure that notice of the same is provided to the prospective investors, on or

before such early date of closure or the initial Closing Date, as the case may

be, through advertisement/s in a leading national daily newspaper

**For detailed terms

and conditions please refer to the Prospectus.

^Religare Capital

Markets Limited ("RCML") is a wholly owned subsidiary of the Promoter

of the Company. As the Promoter of the Company, directly exercises control over

RCML and also there are common promoters (directly or indirectly) and common

directors between RCML and the Company, RCML is deemed to be an associate of

the Company as per the Securities and Exchange Board of India (Merchant

Bankers)Regulations, 1992, as amended ("Merchant Bankers

Regulations"). RCML has signed the due diligence certificate and

accordingly has been disclosed as a Lead Manager. Further, in compliance with

the provisio to Regulation 21A (1) and explanation to Regulation 21A (1) of the

Merchant Bankers Regulations, RCML would be involved only in marketing of the

Issue.

RELIGARE

FINVEST LTD. RECEIVES ISO 9001:2008 CERTIFICATION FROM BSI FOR ITS WORLD-CLASS

PROCESSES

New Delhi, February 28, 2012: Religare Finvest Ltd. (RFL),oneof India's I

argestcapitalized NBFCs and a subsidiary of Religare Enterprises Limited, has

been awarded with ISO 9001:2008 certification by BSI, a leading global

independent business services organization, for its customer-focused Central

Processing Unit, Customer Service and Information Technology Functions.

This development is a great milestone for RFL

as it continues to build out a best of breed Small and M edium Enterprises(SM

E)- focused lending business model. RFL provides debt capital to SM Es in the form

of loans against property, working capital loans, loans against plant and

machinery,vehicles and construction equipment and loan against marketable

securities among others. Religare Finvest currently has over 20000 SME

customers and close to 34000 live SME accounts and its loan book stands at more

than INR 12,1470.700 Millions (as on December 31, 2011). The company had

completed a successful NCD issue and has raised capital from two private equity

players in the recent past- Avigo Capital in November 2011 and Jacob Ballas in

January 2012.

Commenting on this development, Mr. Kavi Arora, Managing Director and CEO, Religare

Finvest Ltd said: "It is indeed a proud moment

for us to receive this prestigious and coveted certification from BSI for three

of our processes in one go. This will no doubt encourage us to set our

standards even higher in line with international best practices and

benchmarks"

Adding to this, Mr. Venkataram Arabolu, Managing Director, BSI

Group- India, said "ISO 9001 is byfar the wo rld's

most esta blished qualityframework and sets the standard not only for quality

management systems, but management systems in general. We are pleased to see

that the processes implemented by Religare Finvest Ltd. are in sync with the

criteria and we are delighted to award the ISO 9001:2008 Certification to them

for the excellent implementation, that goes beyond the basic standards."

About

Religare Finvest Ltd -

www .religarefinvest.com

Religare Finvest Ltd. ("RFL") i s a

Systemically Important Non-Deposit Accepting NBFC, focusing on small and medium

enterprises ("SME") fin ancing and capital market financing. Through

its reach and focus on the SME segment and the broad product offering, RFL provides

the debt capital to power the growth of the small and medium enterprise. RFL's

lending products aimed at providing financing to the SME segment include:

·

Loans against property

·

Working capital loans

· Loans against plant and machinery

· Loans for Commercial vehicles and construction equipment

·

Loan against Marketable Securities

About BSI Group - www.bsigroup.co.in

Since its foundation in 1901, BSI Group has grown into

a leading global independent business services organization that inspires

confidence and delivers assurance to customers with standards-based solutions.

Originating as the world's first national standards body, the Group has over

2,250 staff operating in over 100 countries through more than 50 global

offices. The Group's key offerings include:

·

The development and sale of

private, national and international standards and supporting information,

having created 8 of the top 10 Management Systems standards of the world.

·

Second and third-party management

systems assessment and certification

·

Testing and certification of

products and services

·

Performance management software

solutions

· Training services in support of standards implementation and business best practice

RELIGARE FINVEST NON-CONVERTIBLE DEBENTURES,

ARE THEY WORTH INVESTING?

(17-SEP-2012)

COMPANY OVERVIEW

Religare Finvest Limited (RFL) a subsidiary

of Religare Enterprises Limited (REL), is a Small and Medium Enterprise (SME)

financing focused NBFC. Primarily, RFL provides capital to power the growth of

the SME's.

As per economic survey 2011-2012, the SME sector accounts for 45% of goods

manufactured and 40% of exports. As such, growth of this sector is pivotal for

the economic and social development of the country. If the Indian economy is to

move on to a higher growth trajectory, SMEs, who collectively contribute 17% of

India's GDP, would have to grow and prosper. This thus brings out the

importance of NBFCs providing credit to such SMEs. The diversified suite of

lending solutions of RFL includes:

·

SME

Mortgage Loans

·

SME

Commercial Assets Loans

·

SME

Working Capital Loans

Apart from this, RFL

also caters to retail capital markets financing business which includes Loan

against marketable securities. As on June 30, 2012 RFL has a distribution

network of 25 branches spread across the country.

(Source: Offer Document, PersonalFN Research)

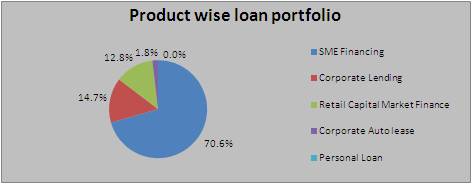

RFL's loan portfolio

as on March 31, 2012 revealed that the SME Financing formed 70.6% of the total

loan book, while the second and third position was occupied by corporate

lending and capital market financing which comprised 14.7% and 12.8%

respectively.

At present in order to augment the lending and working capital needs of the

company, Religare Finvest Limited is currently offering secured Non-Convertible

Redeemable Debentures (NCD) of face value of Rs 1,000 each at par aggregating

to Rs 2500.000 Millions along with a green shoe option to retain

oversubscription up to Rs 2500.000 Millions, thereby taking the total issue

size upto Rs 5000.000 Millions.

As on March 31, 2012, SME finance and retail capital market finance activities accounted for 70% and 13% of its total loan book respectively.

As at June 30, 2012 the Company had a distribution network of 25 branches

spread across the country with an employee strength of 1018.

RFL’s Income from Operations and Net Profit After Tax (PAT) for the financial

year ending March 31, 2012 grew at a 3 year CAGR of 98% and 16% to Rs.

18213.100 Millions and Rs. 1378.200 Millions respectively.

The capital adequacy ratio as of March 31, 2012 computed on the basis of

applicable RBI requirements was 19.65%, compared to the minimum capital

adequacy requirement of 15.00% stipulated by the RBI.

The Loan Book grew at a CAGR of 75% over the last three years to Rs. 1257.359

Millions as on March 31’2012 The Gross NPAs as a percentage of total loan stood

at 0.85% and the Net NPAs as a percentage of Net Loan Assets stood at 0.52% as

on March 31, 2012.

Financial Analysis:

Profits Details: (Rs. in Crs)

|

Year |

Profit Before Tax |

Profit After Tax |

|

2011-12 |

195.32 |

137.82 |

|

2010-11 |

176.16 |

114.78 |

|

2009-10 |

141.89 |

102.82 |

|

2008-09 |

68.62 |

46.04 |

|

2007-08 |

54.59 |

35.70 |

CHARGES

|

ENTITY |

PERSON |

COMPETENT AUTHORITY |

REGULATORY

CHARGES |

REGULATORY

ACTION(S) / DATE OF ORDER |

FURTHER

DEVELOPMENTS |

|

RELIGARE FINVEST

LTD. |

|

SEBI |

DID NOT MAKE DISCLOSURE OF SHAREHOLDING/CHANGES IN SHAREHOLDING

TO COMPANY AND STOCK EXCHANGES AS REQUIRED UNDER REGULATION 7(1) READ WITH

7(2) OF SEBI TAKEOVER CODE, 1997 IN MATTER OF JK AGRI GENETICS LTD. |

|

CMT REPORT (Corruption, Money Laundering & Terrorism]

The Public Notice information has been collected from various sources

including but not limited to: The Courts,

1] INFORMATION ON DESIGNATED

PARTY

No exist designating subject or any of its beneficial owners,

controlling shareholders or senior officers as terrorist or terrorist

organization or whom notice had been received that all financial transactions

involving their assets have been blocked or convicted, found guilty or against

whom a judgement or order had been entered in a proceedings for violating

money-laundering, anti-corruption or bribery or international economic or

anti-terrorism sanction laws or whose assets were seized, blocked, frozen or

ordered forfeited for violation of money laundering or international

anti-terrorism laws.

2] Court Declaration :

No records exist to suggest that subject is or

was the subject of any formal or informal allegations, prosecutions or other

official proceeding for making any prohibited payments or other improper

payments to government officials for engaging in prohibited transactions or

with designated parties.

3] Asset Declaration :

No records exist to suggest that the property or assets of the subject

are derived from criminal conduct or a prohibited transaction.

4] Record on Financial

Crime :

Charges or conviction

registered against subject: None

5] Records on Violation of

Anti-Corruption Laws :

Charges or

investigation registered against subject: None

6] Records on Int’l

Anti-Money Laundering Laws/Standards :

Charges or

investigation registered against subject: None

7] Criminal Records

No available

information exist that suggest that subject or any of its principals have been

formally charged or convicted by a competent governmental authority for any

financial crime or under any formal investigation by a competent government

authority for any violation of anti-corruption laws or international anti-money

laundering laws or standard.

8] Affiliation with

Government :

No record

exists to suggest that any director or indirect owners, controlling

shareholders, director, officer or employee of the company is a government

official or a family member or close business associate of a Government

official.

9] Compensation Package :

Our market

survey revealed that the amount of compensation sought by the subject is fair

and reasonable and comparable to compensation paid to others for similar

services.

10] Press Report :

No press reports / filings exists on

the subject.

CORPORATE GOVERNANCE

MIRA INFORM as part of its Due Diligence do provide comments on Corporate

Governance to identify management and governance. These factors often have been

predictive and in some cases have created vulnerabilities to credit

deterioration.

Our Governance Assessment focuses principally on the interactions

between a company’s management, its Board of Directors, Shareholders and other

financial stakeholders.

CONTRAVENTION

Subject is not known to have contravened any existing local laws,

regulations or policies that prohibit, restrict or otherwise affect the terms

and conditions that could be included in the agreement with the subject.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.53.96 |

|

|

1 |

Rs.84.49 |

|

Euro |

1 |

Rs.72.23 |

INFORMATION DETAILS

|

Report Prepared

by : |

SDA |

SCORE & RATING EXPLANATIONS

|

SCORE FACTORS |

RANGE |

POINTS |

|

HISTORY |

1~10 |

5 |

|

PAID-UP CAPITAL |

1~10 |

5 |

|

OPERATING SCALE |

1~10 |

5 |

|

FINANCIAL CONDITION |

|

|

|

--BUSINESS SCALE |

1~10 |

5 |

|

--PROFITABILIRY |

1~10 |

5 |

|

--LIQUIDITY |

1~10 |

5 |

|

--LEVERAGE |

1~10 |

5 |

|

--RESERVES |

1~10 |

5 |

|

--CREDIT LINES |

1~10 |

5 |

|

--MARGINS |

-5~5 |

-- |

|

DEMERIT POINTS |

|

|

|

--BANK CHARGES |

YES/NO |

NO |

|

--LITIGATION |

YES/NO |

NO |

|

--OTHER ADVERSE INFORMATION |

YES/NO |

NO |

|

MERIT POINTS |

|

|

|

--SOLE DISTRIBUTORSHIP |

YES/NO |

NO |

|

--EXPORT ACTIVITIES |

YES/NO |

YES |

|

--AFFILIATION |

YES/NO |

YES |

|

--LISTED |

YES/NO |

NO |

|

--OTHER MERIT FACTORS |

YES/NO |

YES |

|

TOTAL |

|

45 |

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a

composite of weighted scores obtained from each of the major sections of this

report. The assessed factors and their relative weights (as indicated through

%) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with full

security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

- |

NB |

New Business |

- |

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.