MIRA

INFORM REPORT

|

Report Date : |

04.10.2013 |

IDENTIFICATION DETAILS

|

Name : |

PROXY MARKET |

|

|

|

|

Registered Office : |

28 Rue Le Titien ‑ Val Fleuri, Maarif, Casablanca |

|

|

|

|

Country : |

Morocco |

|

|

|

|

Financials (as on) : |

31.12.2011 |

|

|

|

|

Date of Incorporation : |

18.01.2007 |

|

|

|

|

Com. Reg. No.: |

159527 |

|

|

|

|

Legal Form : |

Societe A Responsibilite Limitee |

|

|

|

|

Line of Business : |

importer and distributor of catering disposable products, food and drink packaging and hygiene products |

|

|

|

|

No. of Employees : |

20 |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31st, 2013

|

Country Name |

Previous Rating (31.12.2012) |

Current Rating (31.03.2013) |

|

Morocco |

A2 |

A2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

morocco ECONOMIC OVERVIEW

Morocco has

capitalized on its proximity to Europe and relatively low labor costs to build

a diverse, open, market-oriented economy. In the 1980s Morocco was a heavily

indebted country before pursuing austerity measures and pro-market reforms,

overseen by the IMF. Since taking the throne in 1999, King MOHAMMED VI has

presided over a stable economy marked by steady growth, low inflation, and

gradually falling unemployment, although a poor harvest and economic

difficulties in Europe contributed to an economic slowdown in 2012. Industrial

development strategies and infrastructure improvements - most visibly

illustrated by a new port and free trade zone near Tangier - are improving

Morocco's competitiveness. Morocco also seeks to expand its renewable energy

capacity with a goal of making renewable 40% of electricity output by 2020. Key

sectors of the economy include agriculture, tourism, phosphates, textiles,

apparel, and subcomponents. To boost exports, Morocco entered into a bilateral

Free Trade Agreement with the United States in 2006 and an Advanced Status

agreement with the European Union in 2008. Despite Morocco's economic progress,

the country suffers from high unemployment, poverty, and illiteracy,

particularly in rural areas. In 2011 and 2012, high prices on fuel - which is

subsidized and almost entirely imported - strained the government''s budget and

widened the country''s current account deficit. Key economic challenges for

Morocco include fighting corruption and reforming the education system, the

judiciary, and the government''s costly subsidy program.

|

Source : CIA |

Company name

PROXY MARKET

Rating Briefing

Payment Record: UNDETERMINED

This rating is based on available data. In the event of additional

information a possibility for a different rating applies.

Registration Briefing

Registration Number: 159527

Registration Date: 18/01/2007

Legal Form: SOCIETE A RESPONSIBILITE LIMITEE

Latest Financials: December 31, 2011

Financial Briefing

Nominal Capital: 1,000,000 Moroccan Dirham

Issued Capital: N/A

Turnover: 14,552,263 Moroccan Dirham

Net Profit: 190,403 Moroccan Dirham

Net Worth: 1,299,136 Moroccan Dirham

Company Details

Company Name: PROXY

MARKET

Headquarter Address: 28

Rue Le Titien ‑ Val Fleuri,

Maarif,

Casablanca,

Morocco

Telephone: +212522

361385

+212522 951854

Fax: +212522

365272

E‑Mail: proxymarket@menara.ma

Web Site: www.proxymarketmaroc.com

Company was originally started on 18/01/2007

Registration & Legal Details

Current Legal Form: SOCIETE

A RESPONSIBILITE LIMITEE

Registration Address: 14

Rue Abou Omar El Harit N° 1,

Casablanca

Registration Number: 159527

Registration Date: 18/01/2007

Year/Date Company Established: 18/01/2007

Registration Town: Casablanca

Tax Registration Number: 02203871

Capital

Currency: Moroccan

Dirham

Authorized Capital: 1,000,000

Paid Up Capital: 1,000,000

Start up Capital:

100,000

Capital to increase to:

900,000

Capital increase on 09/2009 to 900,000

Authorized Capital Breakdown

Number

of Shares: 10,000 Type

of Shares: None Selected

Issued

Shares: 10,000 Value

per share: MDH 100.00

Value

of this type: 1,000,000.00

Shareholders / Owners

Shareholders:

Name/Other Information Shares Held % of

Voting/Non‑Voting

capital

Mr. Amine Bennis, 3,334 33.34%

(VOTING)

Casablanca,

Morocco

Mr. Youssef Bennis, 3,333 33.33%

(VOTING)

Casablanca,

Morocco

Ms. Nouha Bennis, 3,333 33.33%

(VOTING)

Casablanca,

Morocco

Principals

Name: Mr

Saad Bennis

Position within the company: General Manager

Date of Birth: 18/06/1964

Country of Birth: Morocco

Nationality: Moroccan

Can fluently speak: Arabic,

French & English

Name: Mr

Lahcen Bouchghoul

Position within the company: Purchasing Manager

Country of Birth: Morocco

Nationality: Moroccan

Can fluently speak: Arabic

& French

Name: Ms

Zina Mechkour

Position within the company: Accountant

Country of Birth: Morocco

Nationality: Moroccan

Can fluently speak: Arabic

& French

Company Activities

NACE

Codes: 4676 Wholesale of other intermediate

products

The Company

PROXY MARKET is specialized in importing and distribution of catering

disposable products, food and drink packaging and hygiene products.

Local Reporters

consider the investigated company to be MEDIUM in their field of concern.

Operations

Employees Company Employs: 20

HQ Premises Operates from: Owned

Offices , Showroom

Premises Size: 480

square meters

Location: Central

Business Area

Branches 7 Rue Belaamane,

Hay Erraha,

Casablanca,

Morocco

Branch is: Rented

Description of branch: Warehouse

Branch premises size: 280.00 sq.mtrs.

Imports

Import % and type of product: 90% Finished Goods

Imports From: United

Arab Emirates, Egypt, France,

Turkey,

Tunisia

Importing Terms: Cash

against documents

Exports

Export

% and type of product: Subject

does not export

Trading

& Selling

Territory: 100%

Nationally

Type of Customer: Caterers,

Fast Food, Hotels,

Restaurants

Number of accounts:

500

Vehicles: Total

number of vehicles: 10

3 vans

7 cars

Related Companies

Subsidiaries

Affiliates

Information

on Related Companies is not available/applicable

Bankers

Société

Générale,

Branch: 2

Mars

Rue Abdeslam

Khattabi Angle Avenue 2 Mars,

Casablanca,

Morocco

Charges Registered

Date of charge Beneficiary

of the charge Amount secured Description of

Registered

by the charge Charge

01/10/2012 Société Générale MDH 1,300,000 Mortgage

09/09/2011 Crédit Agricole MDH 4,000,000 Mortgage

Financial Information

Source: Companies

Registry

Figures

are: Official

Figures

Currency: Moroccan

Dirham

Months Sales Figures Sales Gross

Profit/Loss Net

Profit/Loss

12 31/12/2011 14,552,263 299,546 190,403

12 31/12/2010 11,724,792 195,823 133,653

12 31/12/2009 10,854,047 59,292 29,362

12 31/12/2008 6,954,862 (12,936) (12,936)

Balance Sheet & Profit &

Loss

BALANCE

SHEET

As at: 31‑Dec‑2011 As at: 31‑Dec‑2010 As at: 31‑Dec‑2009

Fixed Assets

Land

& Buildings 2,020,833 2,145,833 2,270,833

Plant & Machinery

Furniture

& Equipment 52,245 41,187 20,020

Motor

Vehicles 353,889 500,718 400,504

Misc. Fixed Assets

Total Fixed Assets 2,426,967 2,687,738 2,691,357

Financial Assets

Shares in Related Companies

Loans to related companies

Investments

Deposits

Misc. Financial Assets

Total Financial Assets 0 0 0

Intangibles

Goodwill

Organisational Expenses

Patents

Misc. Intangible Assets

Total Intangible Assets 0 0 0

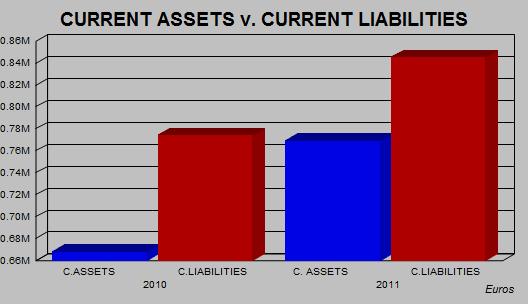

Current Assets

Stock 1,012,490 1,013,698 386,459

Stock & Work in Progress

Trade

Debtors & receivables 6,199,120 5,119,836 4,292,474

Provision for bad debs

Other

receivables 1,183,136 1,139,785 635,378

Due from related companies

Owed by shareholders

Prepaid expenses

Cash 361,001 326,662 56,508

Tax recoverable

Marketable Securities

Misc. Current Assets 2,120,464

Total Current Assets 8,755,747 7,599,981 7,491,283

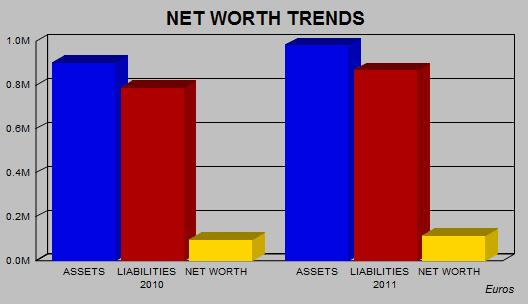

Total Assets 11,182,714 10,287,719 10,182,640

Owner's Equity & Liabilities

Issued

and paid up capital 1,000,000 1,000,000 1,000,000

Share premium account

Retained

earnings 108,733 ‑24,920 ‑54,283

Net

profit/Loss for the year 190,403 133,653 29,362

Revaluation reserves

Legal Reserves

Other reserves

Net

Worth 1,299,136 1,108,733 975,079

Deffered Taxation

Provisions/allowances

Mortgages/Loans 264,345 369,481 349,006

Hire purchase

Due to group of companies

Minority interest

Misc. deferred liabilities

Total Long Term Liabilities 264,345 369,481 349,006

Current Liabilities

Creditors 1,036,981 268,429 820,891

Other

creditors 1,518,690 1,434,106 861,167

Accruals

Bank

overdrafts/Loans 7,056,034 6,996,573 6,999,079

Misc. Loans

Directors accounts

Owing

to shareholders 7,528 110,397 177,418

Owing to related companies

Proposed dividend

Long Term‑due 1 year

Hire Purchase‑under 1 year

Taxation

Advance receipts

Misc. Current Liabilities

Total Current Liabilities 9,619,233 8,809,505 8,858,555

Owner's Equity & Liabilities 11,182,714 10,287,719 10,182,640

PROFIT &

LOSS

Figures are: Figures are: Figures

are:

Fiscal Year Fiscal

Year Fiscal

Year

01/01/2011 to 31/12/2011 01/01/2010 to 31/12/2010 01/01/2009 to 31/12/2009

Total

Income/Turnover 14,552,263 11,724,792 10,854,047

Cost

of sales 12,653,446 10,184,913 8,913,768

Gross

Profit/(Loss) 1,898,817 1,539,879 1,940,279

Admin/selling

expenses 134,697 172,637 178,798

Services 768,598 587,942 539,079

Salaries 369,370 217,300 132,956

Auditors

Fee 571 7 33,600

Stock Depreciation

Depreciation 278,021 240,594 195,959

Misc. Operating Expenses

Misc. Operating Income

Net Operating Profit/(Loss) 347,560 321,399 859,887

Interest Receivable/Finance Income

Group related income

Misc.

Financial Income 754 111,487

Total

Financial Income 0 754 111,487

Interest

Payable/Finance costs 48,009 126,220 833,335

Misc.

financial expenses 5 110 78,747

Total

Financial Expenses 48,014 126,330 912,082

Profit/(Loss)

before taxes 299,546 195,823 59,292

Income

Tax 109,143 62,170 29,930

Other Tax

Profit/(Loss)

after taxes 190,403 133,653 29,362

Extraordinary items

Exceptional items

Misc. Items

Net

Profit/(Loss) 190,403 133,653 29,362

Previous years retained earnings

Current

years net income 190,403 133,653 29,362

Misc. additions in current year

Current years net loss

Dividends in current year

Withdrawals in current year

Misc. deductions in current year

Retained earnings at end of 190,403 133,653 29,362

financial period

Average employees

Directors fee

Earnings per share

Earnings per share‑previous year

Auditors Comments

Accounts

obtained from: Companies registry

Auditors

Opinion: The audited financial statement gives a true and fair view

of the state of

affairs

of the subject

Financial Statements have been prepared on an on‑going

basis.

Assuming support of: shareholders

FINANCIAL RATIOS / COMPARATIVE

DATA

Actual Company Industrial Averages Actual

Company Industrial Averages

Results (2011) (2011) Results

(2010) (2010)

Liquidity Ratios

Current

Ratio 0.91 1.64 0.86 1.52

Acid

Test Ratio 0.80 1.05 0.75 1.00

Accounts

0.07 0.37 0.02 0.41

Payable/Sales Ratio

Current

Liabilities/Net 7.40 2.27 7.95 4.28

Worth

Total

Liabilities/Net 7.61 1.86 8.28 4.44

Worth

Fixed

Assets/Net 186.81 17.67 242.42 41.18

Worth (%)

Profitability Ratios

Gross

Profit Ratio (%) 13.05 26.24 13.13 25.85

Return

on Capital 19.16 20.54 13.25 22.84

Employed (ROCE)(%)

Net

Profit/Sales (%) 2.06 3.60 1.67 ‑1.16

Return

on Assets (%) 2.68 5.06 1.90 3.93

Efficiency Ratios

Sales/Working

Capital ‑16.85 8.49 ‑9.69 7.42

Assets/Sales(%) 76.85 128.74 87.74 123.47

Shareholders

23.06 32.81 17.66 21.97

Return(%)

Average

Inventory 29.22 190.55 25.09 264.26

Period

Average

Collection 141.95 212.00 146.51 139.22

Period

Leverage Ratios

Capital

Employed 11.20 5.43 10.57 6.83

Capital

Structure (%) 16.91 37.64 25.00 0.50

Number

of 762 762

Companies within the

industry (NACE G)

Statistics based on Wholesale

and retail Wholesale

and retail

NACE(G) trade;repair

of motor trade;repair

of motor

vehicles and vehicles

and

motorcycles motorcycles

The statistical

Industrial Average results are calculated against companies within the database

for the specific country.

INDUSTRY SECTOR COMPARATIVE DATA

Elements Taken Result

for specific RANKING Total Companies Used

company

DATE

OF REGISTRATION 18/01/2007 1247 1482

TOTAL

EMPLOYEES 20 452 1293

SALES

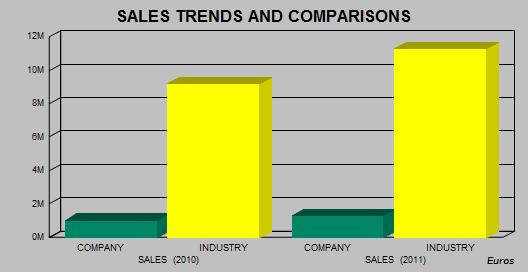

(2011) 1,279,435 283 493

SALES

(2010) 1,030,844 394 699

NET

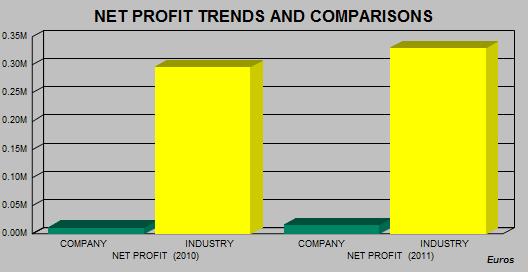

PROFIT (2011) 16,740 293 472

NET

PROFIT (2010) 11,751 456 716

TOTAL

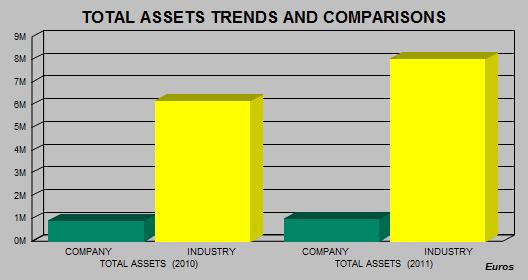

ASSETS (2011) 983,184 272 465

TOTAL

ASSETS (2010) 904,496 394 716

Currency: EUROS

Rankings:

The results given below are

calculated against companies with the Database for the specific country.

Scale: 1 is the highest result

found in our database.

Example: Ranking 5: Total

Companies used to generate the Ranking : 20

This means that this company is

the 5th largest company out of 20 found in our database in the specific

industry

Charts of Financial Trends and Industry Comparisons

PLEASE

NOTE THAT CHARTS ARE SHOWN IN EUROS FOR TREND AND COMPARISON PURPOSES

The statistical

Industrial Average results are calculated against companies within the database

for the specific country.

Payments

Subject's

payments reported to be: UNDETERMINED

Representation

Other Comments

Other Comments: Patent : 37917066

Interview & Reporter Comments

Name/Title: Ms.

Zina Mechkour Accountant

Comment: Latest

Financial Statements are not currently available.

Subject has confirmed the general details provided in the

report but has

declined

to provide any Financial Data.

Reporter

Comment: All legal forms

in Morocco are obliged by law to be registered with the Registry Office

(OMPIC:

Office

Marocain de la Propriete Industrielle et Commerciale) which is publicly

available.

Subject was found registered and Information obtained from

above official source is as

follows

:

Registered

name / registration number / date of registration / registered address / legal

form / capital / main principals – administrators / shareholders / shareholders

% / financial information.

According

to the Morocco Commercial Law, all legal forms except for proprietorship

entities are obliged to file their financial accounts to the OMPIC. However,

the subject latest financial statements are not yet available.

Any other

data stated in the report was obtained directly from the subject company and/or

other publicly available information. Therefore it should be used as a point of

reference as it is not possible to verify such data with official sources.

Conclusions

Local Reputation: The company

being investigated is considered by local reporters to be a Fair /

Normal Trade Risk.

Owner/Shareholders Comments: The owners / shareholders do not have an active

role in the running of the

business.

Financial Results Trend: Financial Information

indicates that the business activities of the company are

showing an upward turn.

Age of Business: The company

is a long established family run business.

Country Intelligence Information

Country: Morocco

Date: 20/08/2013 00:00:00

Source: "Economist

Intelligence Unit" ‑ The Economist

Risk: Last

Updated: 07/08/2013

Sovereign risk

Morocco’s fiscal account will remain deeply in deficit,

owing to high recurrent expenditure on

subsidies and wages. With new lending available on

reasonable terms, much of it concessional,

and a slight

improvement in the country's external position, debt‑service payments

will remain

manageable.

Currency risk

The

current exchange‑rate system—a managed float—will be maintained, with the

Moroccan dirham weakening slightly in 2013 against a stronger euro. A

US$6.2bn precautionary credit line from the IMF in 2012 and a US$1.5bn bond

issuance in December 2012, which has boosted foreign reserves, will increase

confidence in the dirham.

Banking sector risk

The banking sector has benefited from prudential

regulation, relatively low levels of

non‑performing

loans and limited direct foreign exposure. But heavy government borrowing from

the banks to fund a large fiscal deficit will remain a concern. The government

is keen to widen Islamic finance options.

Political risk

The government will maintain high public spending in the

short term to quell political and social

protests

over unemployment, corruption and poverty. Tensions over the disputed territory

of Western Sahara may also lead to violent demonstrations, but a military

conflict is unlikely.

Economic structure risk

A

reliance on agriculture leaves the economy vulnerable to adverse weather conditions.

The fiscal and external deficits fluctuate in line with movements in commodity

prices and external performance is heavily dependent on European demand.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.61.93 |

|

|

1 |

Rs.100.44 |

|

Euro |

1 |

Rs.84.24 |

INFORMATION DETAILS

|

Report

Prepared by : |

MNL |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest capability

for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to

overcome financial difficulties seems comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a

composite of weighted scores obtained from each of the major sections of this

report. The assessed factors and their relative weights (as indicated through

%) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history (10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.