MIRA INFORM REPORT

|

Report Date : |

03.09.2013 |

IDENTIFICATION DETAILS

|

Name : |

COPPERBELT ENERGY CORPORATION PLC |

|

|

|

|

Registered Office : |

Plot

No. 3614, 23rd Avenue, Nkana East., Kitwe |

|

|

|

|

Country : |

Zambia |

|

|

|

|

Financials (as on) : |

31.12.2012 |

|

|

|

|

Date of Incorporation : |

19.09.1997 |

|

|

|

|

Com. Reg. No.: |

39070 |

|

|

|

|

Legal Form : |

Limited Corporation |

|

|

|

|

Line of Business : |

Registered to operate the

generation, transmission, distribution and supply of electricity |

|

|

|

|

No. of Employees : |

375 |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Good |

|

Payment Behaviour : |

Regular |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31st, 2013

|

Country Name |

Previous Rating (31.12.2012) |

Current Rating (31.03.2013) |

|

Zambia |

B2 |

B2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

ZAMBIA - ECONOMIC OVERVIEW

Zambia's economy has experienced

strong growth in recent years, with real GDP growth in 2005-12 more than 6% per

year. Privatization of government-owned copper mines in the 1990s relieved the

government from covering mammoth losses generated by the industry and greatly

increased copper mining output and profitability to spur economic growth.

Copper output has increased steadily since 2004, due to higher copper prices

and foreign investment. In 2005, Zambia qualified for debt relief under the

Highly Indebted Poor Country Initiative, consisting of approximately US$6

billion in debt relief. Poverty remains a significant problem in Zambia,

despite a stronger economy. Zambia's dependency on copper makes it vulnerable

to depressed commodity prices, but record high copper prices and a bumper maize

crop in 2010 helped Zambia rebound quickly from the world economic slowdown

that began in 2008. Zambia has made some strides to improve the ease of doing

business. A high birth rate, relatively high HIV/AIDS burden, and market

distorting agricultural policies have meant that Zambia''s economic growth has

not dramatically decreased the stubbornly high poverty rate

|

Source

: CIA |

SUBJECT'S

NAME

|

Registered Name: |

COPPERBELT

ENERGY CORPORATION PLC |

||

|

Requested Name: |

COPPERBELT ENERGY CORPORATION PLC |

||

|

Other Names: |

CEC |

||

ADDRESS AND TELECOMMUNICATION

|

|||

|

Physical Address: |

Plot

No. 3614, 23rd Avenue, Nkana East., Kitwe |

||

|

Corporate Head Office: |

37B

Cheetah Road, Post Net 145, Private Bag E835 Kabulonga,

Lusaka |

||

|

Postal Address: |

P.

o. Box 20819 |

||

|

|

Kitwe |

||

|

Country: |

Zambia |

||

|

Phone: |

260-212-244051/244556/244000/244063 |

||

|

Fax: |

260-212-244010/244040/244012 |

||

|

Email: |

email@misalas@cec.com.zm/ info@cec.com.zm |

||

|

Website: |

www.cecinvestor.com |

||

CREDIT OPINION

|

|

||

|

Financial Index as of

December 2012 shows subject firm with a medium risk of credit. However, bank

and credit information obtained reveal a history of prompt payments. |

|||

LEGAL

|

|

||

|

Legal Form: |

Limited Corporation |

||

|

Date Incorporated: |

19-Sept-1997 |

||

|

Reg. Number: |

39070 |

||

|

Nominal Capital |

ZMK.

140,000,000 |

||

|

Subscribed Capital |

ZMK.

140,000,000 |

||

|

Subscribed Capital is Subscribed in the following form: |

|||

|

|

Position |

Shares |

|

|

Mr. Hanson Sindowe |

Chairman |

|

|

|

Mr. Owen I. Silavwe |

MD |

|

|

|

Mrs. Jean Madzongwe |

Director |

|

|

|

Mr. Michael John Tarney |

Director |

|

|

|

Mr. Muna Hantuba |

Director |

|

|

|

Mrs. Julia Chaila |

Director |

|

|

|

Mr. Abel Mkandawire |

Director |

|

|

|

Mr. Edson Mweemba Hamakowa |

Director |

|

|

|

Mr. Pius Haangoma Maambo |

Director |

|

|

|

Government of Zambia (Golden Share) |

Shareholder |

1 Special Share |

|

|

ZCCM Investments Holdings Plc |

Shareholder |

20.00% |

|

|

Private Individuals/Institutions |

Shareholder |

28.00% |

|

|

Zambian Energy Corporation (Ireland) Limited |

Shareholder |

52.00% |

|

RELATED COMPANIES

|

None |

Parent company. |

|

None |

Subsidiary company. |

|

ZAMBIAN FIBRE OPTIC TELECOMMUNICATIONS NETWORK POWER SPORTS LIMITED |

Affiliated companies. |

|

None |

Shareholder of subject

firm. |

|

Various in Major towns |

Branches of the firm |

OPERATIONS

|

|

|

Registered to operate the

generation, transmission, distribution and supply of electricity |

|

|

Imports: |

Asia, Middle East |

|

Exports: |

None |

|

Trademarks: |

None |

|

Terms of sale: |

100% tenders |

|

|

|

|

Main Customers: |

General public |

|

Employees: |

375 employees. |

|

Vehicles: |

Several motor vehicles. |

|

Territory of sales: |

Zambia |

|

Location: |

Owned premises, 100,000 square feet, |

AUDITORS AND INSURANCE

|

Auditors: |

Grant Thornton |

|

Insurance Brokers: |

Information not

available. |

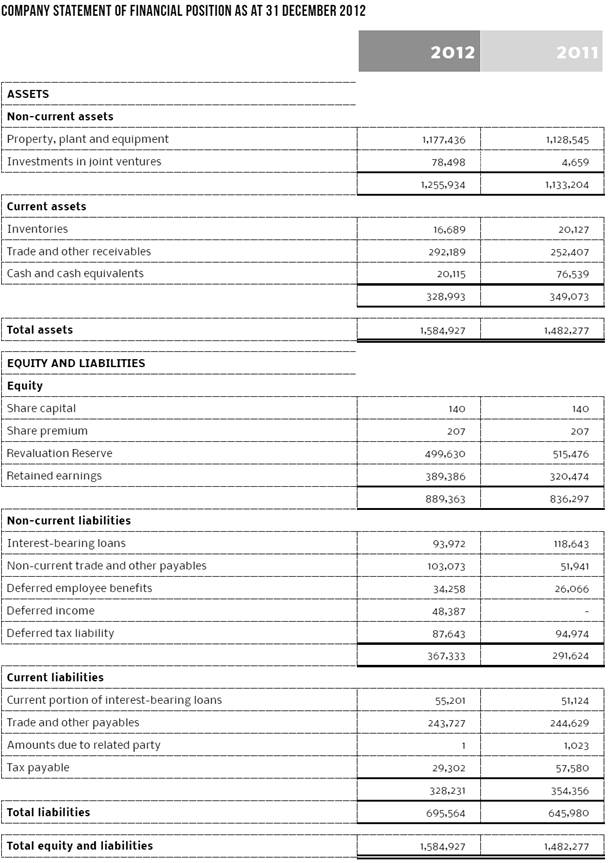

FINANCE

|

|

|

Currency Reported: |

Zambian Kwacha (ZMK.) |

|

Approx. Ex. Rate: |

1 US Dollar = 5365.41

Zambian Kwacha |

|

Fiscal Year End: |

December 31, 2012 |

|

Inflation: |

According to information given by independent sources, the inflation

at December 31st, 2012 was of 13%. |

|

|

|

|

Financial Information

Submitted Below |

|

BANK

|

|

|

Bank Name: |

Citibank

Zambia Limited |

|

Branch: |

Zambia |

|

Comments: |

Other Banks: |

|

|

Barclays Bank of Zambia Limited |

|

|

Stanbic Bank Zambia Limited |

TRADE REFERENCES

|

Experiences: |

Good |

|

|

|

|

NOTARIAL BONDS |

None |

COMMENTS / ADDITIONAL INFORMATION

|

This information was

obtained from outside sources other than the subject company itself and

confirmed the above subject. |

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.65.86 |

|

|

1 |

Rs.102.50 |

|

Euro |

1 |

Rs.87.05 |

INFORMATION DETAILS

|

Report Prepared

by : |

PDT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is

calculated from a composite of weighted scores obtained from each of the major

sections of this report. The assessed factors and their relative weights (as

indicated through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.