MIRA

INFORM REPORT

|

Report Date : |

18.08.2014 |

IDENTIFICATION DETAILS

|

Name : |

SETEMA B.V. |

|

|

|

|

Registered Office : |

Kerkstraat 32 5843AP Westerbeek |

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.12.2012 |

|

|

|

|

Date of Incorporation : |

01.01.2003 |

|

|

|

|

Com. Reg. No.: |

17151190 |

|

|

|

|

Legal Form : |

Private Company |

|

|

|

|

Line of Business : |

Manufacture of machinery for textile, apparel and leather production |

|

|

|

|

No. of Employees |

02 |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

Payment Behaviour : |

No complaints |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – June 1, 2014

|

Country Name |

Previous Rating (31.03.2014) |

Current Rating (01.06.2014) |

|

|

B1 |

B1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

|

Source

: CIA |

Company name and address

ummar

Company name SETEMA B.V.

Operative address Kerkstraat 32

5843AP Westerbeek

Legal form Private Company

Registration number KvK-nummer:

17151190

VAT-number 811982452

|

Year |

2012 |

|

Mutation |

2011 |

|

Mutation |

2010 |

|

Fixed assets |

4.319 |

|

-42,52 |

7.514 |

|

-34,45 |

11.463 |

|

Total receivables |

76.539 |

|

-15,77 |

90.866 |

t |

155,87 |

35.513 |

|

|

|||||||

|

Total equity |

100.000 |

|

464,33 |

-27.448 |

t |

75,28 |

-111.032 |

|

Short term liabilities |

294.663 |

r |

51,66 |

194.297 |

|

-31,52 |

283.736 |

|

|

|||||||

|

Working capital |

95.681 |

|

373,67 |

-34.962 |

t |

71,46 |

-122.495 |

|

Quick ratio |

1,32 |

r |

60,98 |

0,82 |

t |

43,86 |

0,57 |

Contact information

Company name Setema B.V.

Trade names SETeMa B.V.

Operative address Kerkstraat 32

5843AP Westerbeek

Correspondence address Kerkstraat 32

5843AP Westerbeek

Telephone number 0485385764

Fax number 0485385751

Email address info@setema.com

Website www.setema.com

Registration

Registration number KvK-nummer:

17151190

Branch number 000018767710

VAT-number 811982452

Status Active

First registration company register 2003-03-24

Memorandum 2003-03-21

Establishment date 2003-01-01

Legal form Private Company

Activities

SBI Manufacture of

machinery for textile, apparel and leather production (2894)

Exporter Yes

Importer Yes

Goal Het ontwikkelen,

verrichten van research, het verzorgen van produktie, de verkoop, lease en

export van

textielmachines en onderdelen van textielmachines.

Relations

Shareholders SETeMa Holding B.V.

Kerkstraat 32

5843AP WESTERBEEK

Registration number: 171855020000

Percentage: 100%

Companies on same address SETeMa Holding B.V.

Registration number: 171855020000

Stichting Psychologica

Registration number: 172375560000

Management

Active management

SETeMa Holding B.V.

Kerkstraat 32

5843AP WESTERBEEK

Registration number: 171855020000

Competence: Fully authorized

Function: Manager

Starting date: 2008-12-01

Employees

Year 2014 2012 2011

2010 2009

Total 2 2 2 2 2

Payments

Description Payments made under regular condition

Key figures

|

|

|||||

|

Year |

2012 |

2011 |

2010 |

2009 |

2008 |

|

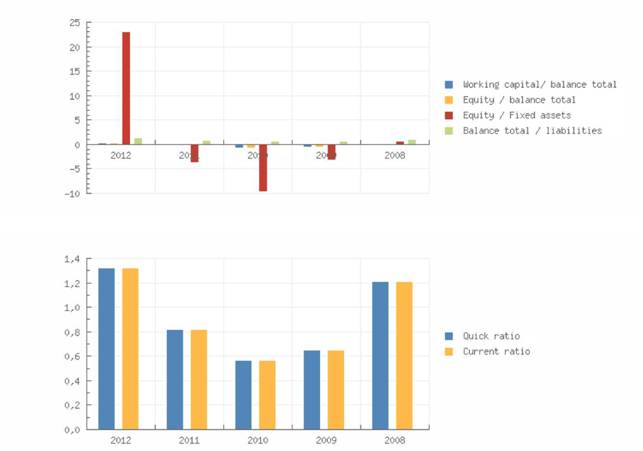

Quick ratio |

1,32 |

0,82 |

0,57 |

0,65 |

1,21 |

|

Current ratio |

1,32 |

0,82 |

0,57 |

0,65 |

1,21 |

|

|

|||||

|

Working capital/ balance total |

0,24 |

-0,21 |

-0,71 |

-0,47 |

0,16 |

|

Equity / balance total |

0,25 |

-0,16 |

-0,64 |

-0,36 |

0,04 |

|

Equity / Fixed assets |

23,15 |

-3,65 |

-9,69 |

-3,14 |

0,73 |

|

Equity / liabilities |

0,34 |

-0,14 |

-0,39 |

-0,26 |

0,04 |

|

Balance total / liabilities |

1,34 |

0,86 |

0,61 |

0,74 |

1,04 |

|

|

|||||

|

Year |

2012 |

2011 |

2010 |

2009 |

2008 |

|

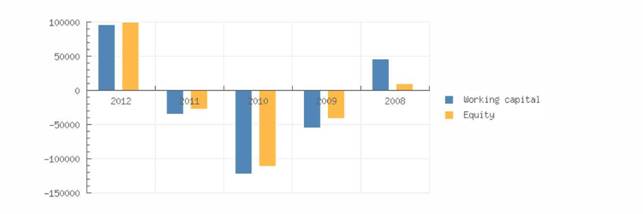

Working capital |

95.681 |

-34.962 |

-122.495 |

-54.558 |

46.184 |

|

Equity |

100.000 |

-27.448 |

-111.032 |

-41.377 |

10.169 |

|

Mutation equity |

464,33 |

75,28 |

-168,34 |

-506,89 |

-86,44 |

|

Mutation short term liabilities |

51,66 |

-31,52 |

80,58 |

-29,67 |

4,40 |

Summary

The 2012 financial result structure is a postive working captial of

95.681 euro, which is in

agreement with 24 % of the total assets of the company.

The working capital has increased with 373.67 % compared to previous

year. The ratio, with

respect to the total assets of the company has however, increased.

The improvement between 2011 and 2012 has mainly been caused by an

increase of the

current assets.

The current ratio of the company in 2012 was 1.32. When the current

ratio is below 1.5, the

company may have problems meeting its short-term obligations.

The quick ratio in 2012 of the company was 1.32. A company with a Quick

Ratio of more than

1 can currently pay back its current liabilities.

The 2011 financial result structure is a negative working captial of

-34.962 euro, which is in

agreement with -21 % of the total assets of the company.

The working capital has increased with 71.46 % compared to previous

year. The ratio, with

respect to the total assets of the company has however, increased.

The improvement between 2010 and 2011 has mainly been caused by an

increase of the

current assets.

The current ratio of the company in 2011 was 0.82. When the current

ratio is below 1.5, the

company may have problems meeting its short-term obligations.

The quick ratio in 2011 of the company was 0.82. A company with a Quick

Ratio of less than

1 cannot currently pay back its current liabilities

Financial statement

Remark annual account The company is

obliged to file its financial statements.

Type of annual account Corporate

Annual account Setema

B.V.

Kerkstraat 32

5843AP Westerbeek

Registration number: 171511900000

Balance

|

Year |

2012 |

2011 |

2010 |

2009 |

2008 |

|

End date |

2012-12-31 |

2011-12-31 |

2010-12-31 |

2009-12-31 |

2008-12-31 |

|

Tangible fixed assets |

4.319 |

7.514 |

11.463 |

13.181 |

13.985 |

|

Fixed assets |

4.319 |

7.514 |

11.463 |

13.181 |

13.985 |

|

Total receivables |

76.539 |

90.866 |

35.513 |

18.177 |

187.254 |

|

Liquid funds |

313.805 |

68.469 |

125.728 |

84.393 |

82.351 |

|

Current assets |

390.344 |

159.335 |

161.241 |

102.570 |

269.605 |

|

Total assets |

394.663 |

166.849 |

172.704 |

115.751 |

283.590 |

|

|

|||||

|

Issued capital |

18.000 |

18.000 |

18.000 |

18.000 |

18.000 |

|

Other reserves |

82.000 |

-45.448 |

-129.032 |

-59.377 |

-7.831 |

|

Total reserves |

82.000 |

-45.448 |

-129.032 |

-59.377 |

-7.831 |

|

Total equity |

100.000 |

-27.448 |

-111.032 |

-41.377 |

10.169 |

|

|

|||||

|

Long term interest yielding debt |

|

|

|

|

50.000 |

|

Long term liabilities |

|

50.000 |

|||

|

Short term liabilities |

294.663 |

194.297 |

283.736 |

157.128 |

223.421 |

|

Total short and long term

liabilities |

294.663 |

194.297 |

283.736 |

157.128 |

273.421 |

|

Total liabilities |

394.663 |

166.849 |

172.704 |

115.751 |

283.590 |

Summary

The total assets of the company increased with 136.54 % between 2011 and

2012.

Despite the assets growth, the non current assets decreased with -42.52

%.

The asset growth has mainly been financed by a Net Worth increase of

464.33 %. Debt,

however, grew with 51.66 %.

In 2012 the assets of the company were 1.09 % composed of fixed assets

and 98.91 % by

current assets. The assets are being financed by an equity of 25.34 %,

and total debt of

74.66 %.

The total assets of the company decreased with -3.39 % between 2010 and

2011.

This downturn is mainly retrievable in the fixed asset decrease of

-34.45 %.

The asset reduction is in contrast with the equity growth of 75.28 %.

Due to this the total debt

decreased with -31.52 %.

In 2011 the assets of the company were 4.5 % composed of fixed assets

and 95.5 % by

current assets. The assets are being financed by an equity of -16.45 %,

and total debt of

116.45 %.

Analysis

Branch (SBI) Manufacture of

machinery and equipment n.e.c. (28)

Region Noord-Oost-Brabant

In the

In the region Noord-Oost-Brabant 151 of the

companies are registered with the SBI code 28

In the

In the region Noord-Oost-Brabant 4 of the

bankruptcies are published within this sector

The risk of this specific sector in the

The risk of this specific sector in the

region Noord-Oost-Brabant is normal

Publications

Filings 27-09-2013: De

jaarrekening over 2012 is gepubliceerd.

09-10-2012: De jaarrekening over 2011 is

gepubliceerd.

19-10-2011: De jaarrekening over 2010 is

gepubliceerd.

10-12-2010: De jaarrekening over 2009 is

gepubliceerd.

03-02-2010: De jaarrekening over 2008 is

gepubliceerd.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.61.06 |

|

|

1 |

Rs.101.84 |

|

Euro |

1 |

Rs.81.56 |

INFORMATION DETAILS

|

Analysis Done by

: |

KAR |

|

|

|

|

Report Prepared

by : |

|

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

|

<10 |

C |

Absolute credit

risk exists. Caution needed to be exercised |

Credit not recommended |

|

|

-- |

NB |

New Business |

-- |

|

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.