MIRA INFORM REPORT

|

Report Date : |

05.07.2014 |

IDENTIFICATION DETAILS

|

Name : |

PUNJI BIKAS SAVING AND CREDIT CO-OPERATIVE LTD. |

|

|

|

|

Registered Office : |

P.O.B. No.: 11432 Pako, New Road, Kathmandu |

|

|

|

|

Country : |

Nepal |

|

|

|

|

Financials (as on) : |

15.07.2013 |

|

|

|

|

Date of Incorporation : |

05.07.2010 |

|

|

|

|

Legal Form : |

Limited Company |

|

|

|

|

Line of Business : |

Subject business activities includes Co-operative systems, Loans, Personal

& Business Loans as well as Banking Services also |

|

|

|

|

No of Employees : |

200 |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made on

e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31, 2014

|

Country Name |

Previous Rating (31.12.2013) |

Current Rating (31.03.2014) |

|

Nepal |

B1 |

B1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low Risk |

A2 |

|

Moderate Low Risk |

B1 |

|

Moderate Risk |

B2 |

|

Moderate High Risk |

C1 |

|

High Risk |

C2 |

nepal ECONOMIC OVERVIEW

Nepal is among the poorest and least developed countries in the world,

with about one-quarter of its population living below the poverty line. Nepal

is heavily dependent on remittances, which amount to as much as 22-25% of GDP.

Agriculture is the mainstay of the economy, providing a livelihood for more

than 70% of the population and accounting for a little over one-third of GDP.

Industrial activity mainly involves the processing of agricultural products,

including pulses, jute, sugarcane, tobacco, and grain. Nepal has considerable

scope for exploiting its potential in hydropower, with an estimated 42,000 MW

of commercially feasible capacity, but political uncertainty and a difficult

business climate have hampered foreign investment. Additional challenges to Nepal's

growth include its landlocked geographic location, persistent power shortages,

underdeveloped transportation infrastructure, civil strife and labor unrest,

and its susceptibility to natural disaster. The lack of political consensus in

the past several years has delayed national budgets and prevented much-needed

economic reform, although the government passed a full budget in 2013.

|

Source

: CIA |

Company

Identification Details

|

Enquired Name |

: |

PUNJI BIKAS SAVING AND CREDIT CO-OPERATIVE

LTD. |

|

Correct Name of Company |

: |

PUNJI BIKAS SAVING AND CREDIT CO-OPERATIVE LTD. |

|

|

|

|

|

Registered Office |

: |

P.O.B. No.: 11432 Pako, New Road, Kathmandu,

Nepal Phone: 4221517, 4258380 Fax: 977-1-4221726 |

|

|

|

|

|

Industry |

: |

Credit & Co-operative |

Official

Company Data

|

Legal Form |

: |

Limited Company |

|

Corporate Identity

Number (CIN) |

: |

1021 |

|

ROC Code |

: |

Kathmandu |

|

Registration Date |

: |

05.07.2010 |

|

Employee |

: |

200 |

|

Auditor |

: |

|

|

Business |

: |

Subject business activities includes Co-operative systems, Loans,

Personal & Business Loans as well as Banking Services also |

|

Bankers |

: |

Nepal Rasto Bank Ltd |

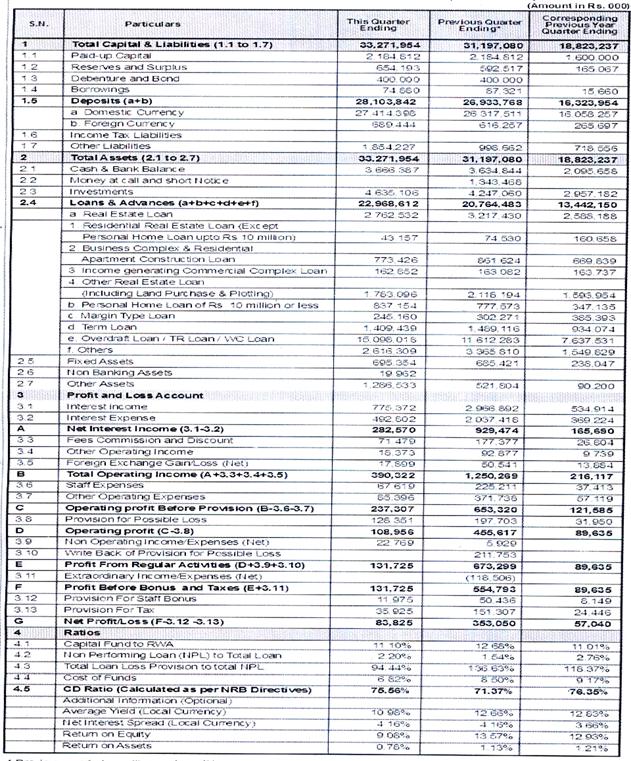

Financial data

(Attached Below)

Balance

sheet as 0n 15th July, 13

Board

of Directors

|

Mr. Chandra Prasad Dhakal |

Chairman |

|

||

|

Mr. Suman Agarwal |

Director |

||

|

Mr. Suraj Kumar Shrestha |

Director |

||

|

Mr. Krishna Bahadur Surana |

Director |

||

|

Mr. Sudarshan Krishna Shrestha |

Director |

||

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.59.79 |

|

UK Pound |

1 |

Rs.102.66 |

|

Euro |

1 |

Rs.81.32 |

INFORMATION DETAILS

|

Analysis Done by

: |

SUB |

|

|

|

|

Report Prepared

by : |

MNL |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s

credit risk and to set the amount of credit to be extended. It is calculated

from a composite of weighted scores obtained from each of the major sections of

this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.