MIRA INFORM REPORT

|

Report Date : |

30.06.2014 |

IDENTIFICATION DETAILS

|

Name : |

AMNITEC LIMITED |

|

|

|

|

Formerly Known As : |

UNITED FLEXIBLE LIMITED |

|

|

|

|

Registered Office : |

Abercanaid Merthyr Tydfil MID Glamorgaon CF 48 1UX |

|

|

|

|

Country : |

United Kingdom |

|

|

|

|

Financials (as on) : |

31.12.2012 |

|

|

|

|

Date of Incorporation : |

18.07.1957 |

|

|

|

|

Legal Form : |

Private limited with share capital |

|

|

|

|

Line of Business : |

Manufacturer of other fabricated metal products n.e.c. |

|

|

|

|

No of Employees : |

Not Available |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

|

|

|

Payment Behaviour : |

Slow But Correct |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made on

e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31, 2014

|

Country Name |

Previous Rating (31.12.2013) |

Current Rating (31.03.2014) |

|

United Kingdom |

A1 |

A1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low Risk |

A2 |

|

Moderate Low Risk |

B1 |

|

Moderate Risk |

B2 |

|

Moderate High Risk |

C1 |

|

High Risk |

C2 |

|

Very High Risk |

D |

UNITED KINGDOM ECONOMIC OVERVIEW

The UK, a leading trading power and financial center, is the third largest economy in Europe after Germany and France. Over the past two decades, the government has greatly reduced public ownership. Agriculture is intensive, highly mechanized, and efficient by European standards, producing about 60% of food needs with less than 2% of the labor force. The UK has large coal, natural gas, and oil resources, but its oil and natural gas reserves are declining and the UK became a net importer of energy in 2005. Services, particularly banking, insurance, and business services, are key drivers of British GDP growth. Manufacturing, meanwhile, has declined in importance but still accounts for about 10% of economic output. After emerging from recession in 1992, Britain's economy enjoyed the longest period of expansion on record during which time growth outpaced most of Western Europe. In 2008, however, the global financial crisis hit the economy particularly hard, due to the importance of its financial sector. Falling home prices, high consumer debt, and the global economic slowdown compounded Britain's economic problems, pushing the economy into recession in the latter half of 2008 and prompting the then BROWN (Labour) government to implement a number of measures to stimulate the economy and stabilize the financial markets; these included nationalizing parts of the banking system, temporarily cutting taxes, suspending public sector borrowing rules, and moving forward public spending on capital projects. Facing burgeoning public deficits and debt levels, in 2010 the CAMERON-led coalition government (between Conservatives and Liberal Democrats) initiated a five-year austerity program, which aimed to lower London's budget deficit from about 11% of GDP in 2010 to nearly 1% by 2015. In November 2011, Chancellor of the Exchequer George OSBORNE announced additional austerity measures through 2017 largely due to the euro-zone debt crisis. The CAMERON government raised the value added tax from 17.5% to 20% in 2011. It has pledged to reduce the corporation tax rate to 21% by 2014. The Bank of England (BoE) implemented an asset purchase program of £375 billion (approximately $605 billion) as of December 2013. During times of economic crisis, the BoE coordinates interest rate moves with the European Central Bank, but Britain remains outside the European Economic and Monetary Union (EMU). In 2012, weak consumer spending and subdued business investment weighed on the economy, however, in 2013 GDP grew 1.4%, accelerating unexpectedly in the second half of the year because of greater consumer spending and a recovering housing market. The budget deficit is falling but remains high at nearly 7% and public debt has continued to increase

|

Source

: CIA |

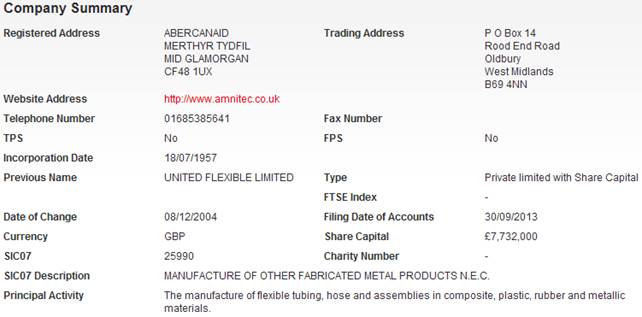

REGISTERED

NAME & COMPANY SUMMARY

AMNITEC LIMITED

DIRECTORS/MANAGEMENT

Current Directors

|

Name |

Date of

Birth |

09/04/1949 |

|

|

Officers

Title |

Mr |

Nationality |

American |

|

Present

Appointments |

3 |

Function |

Director |

|

Appointment

Date |

10/08/2004 |

|

|

|

Address |

7700

Dunvegan Close, Atlanta, Ga 30350 |

||

Current Company Secretary

|

Name |

Date of

Birth |

26/06/1947 |

|

|

Officers

Title |

Mr |

Nationality |

American |

|

Present

Appointments |

2 |

Function |

Company

Secretary |

|

Appointment

Date |

22/11/2004 |

|

|

|

Address |

Abercanaid,

Merthyr Tydfil, Mid Glamorgan, CF48 1UX |

||

Previous Director/Company Secretaries

|

Name |

Current

Directorships |

Previous Directorships |

|

0 |

1 |

|

|

0 |

18 |

|

|

0 |

18 |

|

|

19 |

68 |

|

|

0 |

2 |

|

|

0 |

1 |

|

|

4 |

69 |

|

|

0 |

2 |

|

|

1 |

5 |

|

|

1 |

5 |

|

|

2 |

4 |

|

|

56 |

19 |

|

|

0 |

1 |

|

|

0 |

9 |

|

|

1 |

10 |

|

|

0 |

7 |

|

|

0 |

7 |

|

|

2 |

45 |

|

|

0 |

4 |

|

|

0 |

4 |

|

|

0 |

8 |

|

|

3 |

6 |

|

|

0 |

4 |

|

|

6 |

8 |

|

|

0 |

11 |

|

|

0 |

1 |

NEGATIVE

INFORMATION

Mortgage Summary

Total Mortgage

3

Outstanding

2

Satisfied

1

Trade Debtors / Bad Debt Summary

Total Number of Documented Trade 2

Total Value of Documented Trade £310

CCJ

|

Total

Number of Exact CCJs - |

Total

Value of Exact CCJs - |

||

|

Total

Number of Possible CCJs - |

Total

Value of Possible CCJs - |

||

|

Total

Number of Satisfied CCJs - |

Total

Value of Satisfied CCJs - |

||

|

Total

Number of Writs - |

- |

|

|

Exact CCJ Details

|

No CCJs

found |

Possible CCJs Details

|

There are

no possible CCJ details |

Writ Details

|

No writs

found |

Mortgage Details

|

Mortgage

Type: |

FIXED

CHARGE ON DEBTS |

||

|

Date

Charge Created: |

19/08/10 |

|

|

|

Date

Charge Registered: |

25/08/10 |

|

|

|

Date Charge

Satisfied: |

- |

|

|

|

Status: |

OUTSTANDING |

|

|

|

Person(s)

Entitled: |

FORTIS

COMMERCIAL FINANCE LIMITED |

||

|

Amount

Secured: |

ALL

MONIES DUE OR TO BECOME DUE FROM THE COMPANY TO THE CHARGEE ON ANY ACCOUNT WHATSOEVER

UNDER THETERMS OF THE AFOREMENTIONED INSTRUMENT CREATING OR EVIDENCING THE

CHARGE |

||

|

Details: |

BY WAY OF

FIXED EQUITABLE CHARGE, ANY DEBT, BY WAY OF FLOATING CHARGE THE SPECIFIED

DEBTS SEE IMAGEFOR FULL DETAILS |

||

|

Mortgage

Type: |

COMPOSITE

GUARANTEE AND DEBENTURE |

||

|

Date

Charge Created: |

10/08/04 |

|

|

|

Date

Charge Registered: |

26/08/04 |

|

|

|

Date

Charge Satisfied: |

17/08/12 |

|

|

|

Status: |

SATISFIED |

|

|

|

Person(s)

Entitled: |

GMAC COMMERCIAL

FINANCE PLC (IN ITS OWN CAPACITY AND IN ITS CAPACITY AS SECURITY AGENT FOR

THEU |

||

|

Amount

Secured: |

|

||

|

Details: |

FIXED AND

FLOATING CHARGES OVER THE UNDERTAKING AND ALL PROPERTY AND ASSETS PRESENT AND

FUTURE INCLUDING GOODWILL BOOKDEBTS UNCALLED CAPITAL BUILDINGS FIXTURESFIXED

PLANT AND MACHINERYSEE THE MORTGAGECHARGE DOCUMENT FOR FULL DETAILS |

||

|

Mortgage

Type: |

COMPOSITE

GUARANTEE AND DEBENTURE |

||

|

Date

Charge Created: |

10/08/04 |

|

|

|

Date

Charge Registered: |

24/08/04 |

|

|

|

Date

Charge Satisfied: |

- |

|

|

|

Status: |

OUTSTANDING |

|

|

|

Person(s)

Entitled: |

SENIOR

PLC |

||

|

Amount

Secured: |

ALL

MONIES DUE OR TO BECOME DUE FROM ANY OBLIGOR OR ANY CHARGOR, SUBJECT TO A MAXIMUM

AGGREGATE LIABILITY OF £564,000.00, TO THE CHARGEE UNDER THE TERMS OF THE

AFOREMENTIONED INSTRUMENT CREATING OR EVIDENCING THE CHARGE |

||

|

Details: |

FIXED AND

FLOATING CHARGES OVER THE UNDERTAKING AND ALL PROPERTY AND ASSETS PRESENT AND

FUTURE INCLUDING GOODWILL BOOKDEBTS UNCALLED CAPITAL BUILDINGS FIXTURESFIXED

PLANT AND MACHINERY SEE THE MORTGAGE CHARGE DOCUMENT FOR FULL DETAILS |

||

SHARE

& SHARE CAPITAL INFORMATION

Top 20 Shareholders

|

Name |

Currency |

Share

Count |

Share

Type |

Nominal Value |

% of

Total Share Count |

|

UNITED

FLEXIBLE LTD |

GBP |

7,732,000 |

ORDINARY |

1 |

100 |

PAYMENT

INFORMATION

|

Average Invoice Value |

£734.29 |

|

Invoices available |

361 |

|

Paid |

331 |

|

Outstanding |

30 |

|

Trade Payment Data is information that we collect from selected third

party partners who send us information about their whole sales ledger. |

|

|

Within Terms |

0-30 Days |

31-60 Days |

61-90 Days |

91+ Days |

|

Paid |

129 |

118 |

67 |

16 |

1 |

|

Outstanding |

15 |

15 |

0 |

0 |

0 |

GROUP

STRUCTURE & AFFILIATED COMPANIES

Group structure

|

Company

Name |

Registered

Number |

Latest

Key Financials |

Consol.

Accounts |

Turnover |

|

|

N/A |

- |

- |

|

|

05127235 |

31.12.2012 |

Y |

£44,200,000

|

|

|

00587472 |

31.12.2012 |

N |

£8,302,000

|

FINANCIAL

INFORMATION

Profit & Loss

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Weeks |

52 |

(%) |

52 |

(%) |

52 |

(%) |

52 |

(%) |

52 |

|

Currency |

GBP |

(%) |

GBP |

(%) |

GBP |

(%) |

GBP |

(%) |

GBP |

|

Consolidated

A/cs |

N |

(%) |

N |

(%) |

N |

(%) |

N |

(%) |

N |

|

Turnover |

£8,302,000 |

-6.2% |

£8,848,000 |

2.3% |

£8,650,000 |

14.5% |

£7,552,000 |

-33.3% |

£11,319,000 |

|

Export |

£5,449,000 |

-5.2% |

£5,750,000 |

18.4% |

£4,856,000 |

- |

- |

- |

- |

|

Cost of

Sales |

£7,182,000 |

0.5% |

£7,148,000 |

1.1% |

£7,071,000 |

11.2% |

£6,357,000 |

-32.5% |

£9,412,000 |

|

Gross

Profit |

£1,120,000 |

-34.1% |

£1,700,000 |

7.7% |

£1,579,000 |

32.1% |

£1,195,000 |

-37.3% |

£1,907,000 |

|

Wages

& Salaries |

£2,656,000 |

-0.3% |

£2,663,000 |

-3.1% |

£2,748,000 |

-1% |

£2,775,000 |

-17.2% |

£3,352,000 |

|

Directors

Emoluments |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Operating

Profit |

£190,000 |

-63.7% |

£523,000 |

190.6% |

£180,000 |

122.3% |

-£807,000 |

-288.1% |

£429,000 |

|

Depreciation |

£49,000 |

-47.9% |

£94,000 |

-14.5% |

£110,000 |

-37.1% |

£175,000 |

-24.9% |

£233,000 |

|

Audit

Fees |

£25,000 |

- |

£25,000 |

-10.7% |

£28,000 |

- |

£28,000 |

33.3% |

£21,000 |

|

Interest

Payments |

£76,000 |

-15.6% |

£90,000 |

11.1% |

£81,000 |

-54.7% |

£179,000 |

-66.8% |

£539,000 |

|

Pre Tax

Profit |

£114,000 |

-73.7% |

£433,000 |

337.4% |

£99,000 |

110% |

-£986,000 |

-388.3% |

£342,000 |

|

Taxation |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Profit

After Tax |

£114,000 |

-73.7% |

£433,000 |

337.4% |

£99,000 |

110% |

-£986,000 |

-388.3% |

£342,000 |

|

Dividends

Payable |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Retained

Profit |

£114,000 |

-73.7% |

£433,000 |

337.4% |

£99,000 |

110% |

-£986,000 |

-388.3% |

£342,000 |

Balance Sheet

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Tangible

Assets |

£140,000 |

-21.3% |

£178,000 |

-31.8% |

£261,000 |

-29.6% |

£371,000 |

-32.1% |

£546,000 |

|

Intangible

Assets |

0 |

- |

0 |

- |

0 |

- |

0 |

- |

0 |

|

Total

Fixed Assets |

£140,000 |

-21.3% |

£178,000 |

-31.8% |

£261,000 |

-29.6% |

£371,000 |

-32.1% |

£546,000 |

|

Stock |

£767,000 |

-0.3% |

£769,000 |

-16.8% |

£924,000 |

15.6% |

£799,000 |

-26.6% |

£1,088,000 |

|

Trade

Debtors |

£1,364,000 |

-14.5% |

£1,596,000 |

13.5% |

£1,406,000 |

-61.9% |

£3,688,000 |

-23.7% |

£4,834,000 |

|

Cash |

£28,000 |

- |

0 |

- |

0 |

-100% |

£65,000 |

-72.8% |

£239,000 |

|

Other

Debtors |

£5,020,000 |

-1.4% |

£5,091,000 |

2.7% |

£4,957,000 |

-17.1% |

£5,981,000 |

8.2% |

£5,529,000 |

|

Miscellaneous

Current Assets |

0 |

- |

0 |

- |

0 |

- |

0 |

- |

0 |

|

Total

Current Assets |

£7,179,000 |

-3.7% |

£7,456,000 |

2.3% |

£7,287,000 |

-30.8% |

£10,533,000 |

-9.9% |

£11,690,000 |

|

Trade

Creditors |

£974,000 |

-8.1% |

£1,060,000 |

-22.2% |

£1,363,000 |

0.7% |

£1,353,000 |

-33.3% |

£2,030,000 |

|

Bank

Loans & Overdrafts |

0 |

-100% |

£22,000 |

-76.3% |

£93,000 |

- |

0 |

- |

0 |

|

Other

Short Term Finance |

£5,654,000 |

-4.3% |

£5,907,000 |

6.7% |

£5,536,000 |

-36.3% |

£8,694,000 |

77.3% |

£4,904,000 |

|

Miscellaneous

Current Liabilities |

£186,000 |

-27.3% |

£256,000 |

-57.5% |

£602,000 |

-39.9% |

£1,002,000 |

36% |

£737,000 |

|

Total Current

Liabilities |

£6,814,000 |

-5.9% |

£7,245,000 |

-4.6% |

£7,594,000 |

-31.3% |

£11,049,000 |

44% |

£7,671,000 |

|

Bank

Loans & Overdrafts and LTL |

£4,000 |

-83.3% |

£24,000 |

-74.2% |

£93,000 |

- |

0 |

-100% |

£3,724,000 |

|

Other

Long Term Finance |

£4,000 |

100% |

£2,000 |

- |

0 |

- |

0 |

-100% |

£3,724,000 |

|

Total

Long Term Liabilities |

£4,000 |

100% |

£2,000 |

- |

0 |

- |

0 |

-100% |

£3,724,000 |

Capital & Reserves

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Called Up

Share Capital |

£7,732,000 |

- |

£7,732,000 |

- |

£7,732,000 |

- |

£7,732,000 |

- |

£7,732,000 |

|

P & L

Account Reserve |

-£7,423,000 |

1.5% |

-£7,537,000 |

5.4% |

-£7,970,000 |

1.2% |

-£8,069,000 |

-13.9% |

-£7,083,000 |

|

Revaluation

Reserve |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Sundry

Reserves |

£192,000 |

- |

£192,000 |

- |

£192,000 |

- |

£192,000 |

- |

£192,000 |

|

Shareholder

Funds |

£501,000 |

29.5% |

£387,000 |

941.3% |

-£46,000 |

68.3% |

-£145,000 |

-117.2% |

£841,000 |

Other Financial Items

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Net Worth |

£501,000 |

29.5% |

£387,000 |

941.3% |

-£46,000 |

68.3% |

-£145,000 |

-117.2% |

£841,000 |

|

Working

Capital |

£365,000 |

73% |

£211,000 |

168.7% |

-£307,000 |

40.5% |

-£516,000 |

-112.8% |

£4,019,000 |

|

Total

Assets |

£7,319,000 |

-4.1% |

£7,634,000 |

1.1% |

£7,548,000 |

-30.8% |

£10,904,000 |

-10.9% |

£12,236,000 |

|

Total

Liabilities |

£6,818,000 |

-5.9% |

£7,247,000 |

-4.6% |

£7,594,000 |

-31.3% |

£11,049,000 |

-3% |

£11,395,000 |

|

Net

Assets |

£501,000 |

29.5% |

£387,000 |

941.3% |

-£46,000 |

68.3% |

-£145,000 |

-117.2% |

£841,000 |

Cash Flow

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Net

Cashflow from Operations |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Net

Cashflow before Financing |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Net

Cashflow from Financing |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

Increase in

Cash |

- |

- |

- |

- |

- |

- |

- |

- |

- |

Miscellaneous

|

Date Of

Accounts |

31/12/12 |

(%) |

31/12/11 |

(%) |

31/12/10 |

(%) |

31/12/09 |

(%) |

31/12/08 |

|

Contingent

Liability |

NO |

- |

NO |

- |

NO |

- |

NO |

- |

NO |

|

Capital

Employed |

£505,000 |

29.8% |

£389,000 |

945.7% |

-£46,000 |

68.3% |

-£145,000 |

-103.2% |

£4,565,000 |

|

Number of

Employees |

106 |

-0.9% |

107 |

-7.8% |

116 |

6.4% |

109 |

-18% |

133 |

|

Auditors |

BDO LLP |

||||||||

|

Auditor

Comments |

The audit

report contains no adverse comments |

||||||||

|

Bankers |

HSBC BANK

PLC |

||||||||

|

Bank

Branch Code |

40-00-00 |

||||||||

Ratios

|

Date Of

Accounts |

31/12/12 |

31/12/11 |

31/12/10 |

31/12/09 |

31/12/08 |

|

Pre-tax

profit margin % |

1.37 |

4.89 |

1.14 |

-13.06 |

3.02 |

|

Current

ratio |

1.05 |

1.03 |

0.96 |

0.95 |

1.52 |

|

Sales/Net

Working Capital |

22.75 |

41.93 |

-28.18 |

-14.64 |

2.82 |

|

Gearing % |

0.80 |

6.20 |

-202.20 |

0 |

442.80 |

|

Equity in

% |

6.80 |

5.10 |

-0.60 |

-1.30 |

6.90 |

|

Creditor

Days |

42.70 |

43.60 |

57.35 |

65.21 |

65.28 |

|

Debtor

Days |

59.80 |

65.65 |

59.16 |

177.75 |

155.45 |

|

Liquidity/Acid

Test |

0.94 |

0.92 |

0.83 |

0.88 |

1.38 |

|

Return On

Capital Employed % |

22.57 |

111.31 |

-215.21 |

680 |

7.49 |

|

Return On

Total Assets Employed % |

1.55 |

5.67 |

1.31 |

-9.04 |

2.79 |

|

Current

Debt Ratio |

13.60 |

18.72 |

-165.08 |

-76.20 |

9.12 |

|

Total

Debt Ratio |

13.60 |

18.72 |

-165.08 |

-76.20 |

13.54 |

|

Stock

Turnover Ratio % |

9.23 |

8.69 |

10.68 |

10.57 |

9.61 |

|

Return on

Net Assets Employed % |

22.75 |

111.88 |

-215.21 |

680 |

40.66 |

Creditor Details

|

|

Total Number |

Total Value |

|

Trade

Creditors |

0 |

- |

|

No

Creditor Data |

Trade Debtors / Bad Debt Detail

|

|

Total Number of Documented Trade |

Total Value of Documented Trade |

|

Trade

Debtors |

2 |

£310 |

|

Company

Name |

Amount |

Statement

Date |

|

£157 |

25/03/2011 |

|

|

£153 |

11/10/2010 |

FOREIGN

EXCHANGE RATES

N/a

ADDITIONAL

INFORMATION

Status History

|

No Status

History found. |

Event

History

|

Date |

Description |

|

11/10/2013 |

New

Accounts Filed |

|

24/09/2013 |

Annual

Returns |

|

09/10/2012 |

New

Accounts Filed |

|

09/10/2012 |

New

Accounts Filed |

|

14/08/2012 |

Annual

Returns |

|

28/10/2011 |

New

Accounts Filed |

|

28/10/2011 |

New

Accounts Filed |

|

09/08/2011 |

Annual

Returns |

|

23/05/2011 |

New

Accounts Filed |

|

07/08/2010 |

Annual

Returns |

|

14/04/2010 |

New

Accounts Filed |

|

23/08/2009 |

Annual

Returns |

|

29/10/2008 |

New

Accounts Filed |

|

24/06/2008 |

Annual

Returns |

|

05/11/2007 |

New

Accounts Filed |

Previous Company Names

|

Date |

Previous

Name |

|

08/12/2004 |

UNITED

FLEXIBLE LIMITED |

|

20/09/2004 |

SENIOR

FLEXONICS LIMITED |

|

06/04/1992 |

SENIOR

TIFT LIMITED |

|

26/04/1989 |

TIFT

LIMITED |

|

08/12/1988 |

T.I. FLEXIBLE

TUBES LIMITED |

|

31/12/1978 |

COMPOFLEX

COMPANY LIMITED |

NOTES

& COMMENTS

Commentary

|

No exact

match CCJs are recorded against the company. |

|

|

Sales in

the latest trading period decreased 6.2% on the previous trading period. |

|

|

Net Worth

increased by 29.5% during the latest trading period. |

|

|

A 4.1%

decline in Total Assets occurred during the latest trading period. |

|

|

Pre-tax

profits decreased by 73.7% compared to the previous trading period. |

|

|

The audit

report contains no adverse comments. |

|

|

No recent

changes in directorship are recorded. |

|

|

The

company is part of a group. |

|

|

The

company was established over 56 years ago. |

|

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs. 60.09 |

|

|

1 |

Rs. 102.39 |

|

Euro |

1 |

Rs. 81.88 |

INFORMATION DETAILS

|

Analysis Done by

: |

SUB |

|

|

|

|

Report Prepared

by : |

DPT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit transaction.

It has above average (strong) capability for payment of interest and

principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome

financial difficulties seems comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s

credit risk and to set the amount of credit to be extended. It is calculated

from a composite of weighted scores obtained from each of the major sections of

this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.