MIRA

INFORM REPORT

|

Report Date : |

19.05.2014 |

IDENTIFICATION DETAILS

|

Name : |

HYUVEFARMA

AD |

|

|

|

|

Registered Office : |

J.K. Iztok, UL. Nikolay Haytov

No.3A, et.5, 1113 Sofia |

|

|

|

|

Country : |

Bulgaria |

|

|

|

|

Financials (as on) : |

31.12.2013 |

|

|

|

|

Date of Incorporation : |

1999 |

|

|

|

|

Legal Form : |

Joint Stock Company |

|

|

|

|

Line of Business : |

Wholesale of pharmaceutical goods |

|

|

|

|

No. of Employees |

107 |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

Payment Behaviour : |

No complaints |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31, 2014

|

Country Name |

Previous Rating (31.12.2013) |

Current Rating (31.03.2014) |

|

Bulgaria |

|

|

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low Risk |

A2 |

|

Moderately Low Risk |

B1 |

|

Moderate Risk |

B2 |

|

Moderately High Risk |

C1 |

|

High Risk |

C2 |

|

Very High Risk |

D |

BULGARIA - ECONOMIC OVERVIEW

Bulgaria, a former Communist

country that entered the EU on 1 January 2007, averaged more than 6% annual

growth from 2004 to 2008, driven by significant amounts of bank lending,

consumption, and foreign direct investment. Successive governments have

demonstrated a commitment to economic reforms and responsible fiscal planning,

but the global downturn sharply reduced domestic demand, exports, capital

inflows, and industrial production. GDP contracted by 5.5% in 2009, and has

been slow to recover in the years since. Despite having a favorable investment

regime, including low, flat corporate income taxes, significant challenges

remain. Corruption in public administration, a weak judiciary, and the presence

of organized crime continue to hamper the country's investment climate and

economic prospects

|

Source

: CIA |

COMPANY DETAILS

Local

name: HYUVEFARMA AD

International

name: HUVEPHARMA AD

Registered

address:

j.k.

Iztok, ul. Nikolay Haytov No.3A, et.5

1113 SOFIA

Bulgaria

Telephone: +359-2-8625331, +359-2-8682095

Fax: +359-2-8625334, +359-2-9713027

Internet: http://www.huvepharma.com, http://www.huvepharma.bg

ESTABLISHMENT

& REGISTRATION:

Established:

1999

Registered at Sofia Town Court

Court number 14043/ 1999

Bulstat/VAT number: 130128520

HISTORY:

Established

in 1999 as BULGARSKA FARMACEVTICHNA KOMPANIA AD.

In 2005 the company changed its name to HYUVEFARMA AD.

According to press-release 38,2% from the company were acquired by Citi Group

in December 2010 for the price of 75 million EUR. Obviously this was made

through a Luxembourg-registered company. According to the business press this

is a positive sign and shows that the market evaluation of the whole company

exceeds 200 MEUR.

LEGAL

FORM:

Joint Stock Company (AD)

REGISTERED

CAPITAL:

BGN 29 497 000.00

BANKERS:

Eurobank

EFG Bulgaria AD

Credit Agricole Bulgaria EAD

BNP Paribas

Banka Piraeus Bulgaria

UniCredit Bulbank AD

Sitybank AD

www.bulbank.bg

SHAREHOLDERS/MANAGEMENT

SHAREHOLDERS:

|

ADVANCE PROPERTIES OOD |

63.42% |

|

ID 131159471 |

|

|

Silverspot Investments S.a.r.l. (Luxembourg) |

36.58% |

|

|

|

MANAGEMENT:

|

KIRIL PETROV DOMUSCHIEV |

|

- Manager |

RELATED

COMPANIES:

|

Company

ID |

Company

Name |

|

825395495 |

"TARGOVSKI TSENTAR

""TRAKIYA""" |

|

813109356 |

MOTORINJENERING |

|

200864986 |

HYUVEFARMA SPORT |

|

175358560 |

KEY DJI MARITAYM SHIPING |

|

175110522 |

PORT REYL |

|

175015316 |

ESTE PROPARTIS |

|

131475747 |

PASIFIK 2000 |

|

131143773 |

KEY PI DJI PROPARTIS |

|

112591505 |

BIOVET FIYD |

|

112029879 |

BIOVET |

|

106623336 |

TURBOGEN |

|

103268937 |

MOTORINJENERING-INVEST |

|

103005039 |

VARNA-KOMERS |

BUSINESS ACTIVITY

BUSINESS

OPERATION:

NACE 1.1: 51.46 Wholesale of pharmaceutical

goods

Activity:

The

company is a major shareholder in BIOVET AD - a big Bulgarian producer of

veterinary medicines with turnover EUR 50 million.

Operation is connected with trade with BIOVET’s products.

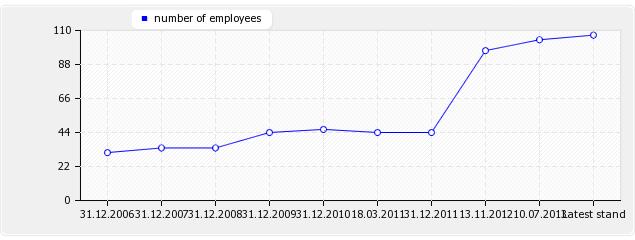

NUMBER

OF EMPLOYEES:

|

As

at date |

Value |

|

31.12.2006 |

31 |

|

31.12.2007 |

34 |

|

31.12.2008 |

34 |

|

31.12.2009 |

44 |

|

31.12.2010 |

46 |

|

18.03.2011 |

44 |

|

31.12.2011 |

44 |

|

13.11.2012 |

97 |

|

10.07.2013 |

104 |

|

Latest

stand |

107 |

EXPORT:

EU, Russia

IMPORT:

EU

REAL ESTATE:

Own offices.

FINANCIAL DATA

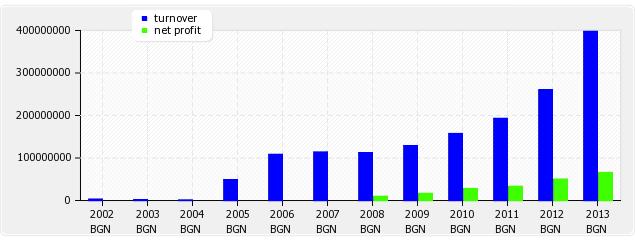

TURNOVER:

|

Year |

Currency |

Value |

|

2002 |

BGN |

3

085 000.00 |

|

2003 |

BGN |

1

433 000.00 |

|

2004 |

BGN |

910

000.00 |

|

2005 |

BGN |

48

661 000.00 |

|

2006 |

BGN |

108

438 000.00 |

|

2007 |

BGN |

113

906 000.00 |

|

2008 |

BGN |

112

404 000.00 |

|

2009 |

BGN |

128

737 000.00 |

|

2010 |

BGN |

157

427 000.00 |

|

2011 |

BGN |

193

112 000.00 |

|

2012 |

BGN |

260

185 000.00 |

|

2013 |

BGN |

397

789 000.00 |

MODES

OF PAYMENT:

Payments are made within agreed

terms.

DEBT

COLLECTION:

No debt collection cases are

registered against the company.

BANK

DISTRAINTS:

No shares of the company are

under bank distraint.

UNPAID

TAXES/ CONTRIBUTIONS TO GOVERNMENT:

There is no publication about

overdue unpaid taxes.

INVOLVEMENT

IN LEGAL DISPUTES:

There is no publication about

legal claims or disputes against the company.

OTHER

PAYMENT INFORMATION:

No adverse payment information

is available.

BRANCH

INDICATOR:

The company's payment behaviour

is average for the branch.

GENERAL

PAYMENT ASSESSMENT:

A

FINANCIAL

OPINION:

A

Exchange rate since 1998 is 1

BGN (denominated lev) = 0.51 EUR

|

Ratio |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

|

Debt ratio |

0.45 |

0.36 |

0.29 |

0.19 |

0.22 |

0.39 |

|

Quick ratio |

1.20 |

1.67 |

1.82 |

4.53 |

6.53 |

1.15 |

|

Current ratio |

1.39 |

1.72 |

2.00 |

4.89 |

7.07 |

2.12 |

|

Days purchase in payables |

96.42 |

85.65 |

84.94 |

34.71 |

28.43 |

87.02 |

|

Operating margin in % |

9.65 |

14.32 |

19.66 |

19.12 |

21.37 |

19.08 |

|

Cash ratio (acid ratio) |

0.01 |

0.12 |

0.28 |

0.54 |

0.45 |

0.27 |

|

Return on sales ROS in % |

8.67 |

12.89 |

17.66 |

17.21 |

19.23 |

16.53 |

|

Return on assets ROA in % |

7.92 |

12.63 |

17.73 |

18.51 |

20.39 |

13.74 |

|

Return on equity ROE in % |

14.36 |

19.75 |

24.98 |

22.88 |

26.16 |

22.37 |

|

Days supply in inventory |

18.65 |

2.66 |

13.59 |

10.92 |

14.18 |

82.68 |

|

Days sales in receivables |

113.94 |

132.87 |

130.70 |

138.45 |

173.09 |

77.04 |

|

BALANCE SHEET in BGN'000 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

|

Accounting

period: |

1.1.2008

- |

1.1.2009

- |

1.1.2010

- |

1.1.2011

- |

1.1.2012

- |

1.1.2013

- |

|

Fixed assets |

81179 |

78814 |

83190 |

88490 |

99999 |

274680 |

|

Tangible assets |

655 |

622 |

1059 |

1712 |

2135 |

135873 |

|

Intangible assets |

37556 |

35323 |

36982 |

39814 |

49421 |

138702 |

|

Long-term investments |

42838 |

42827 |

45113 |

46882 |

48345 |

36 |

|

Goodwill |

|

|

|

|

|

|

|

Prepaid expenses, deferred income, similar accounts |

130 |

42 |

36 |

82 |

98 |

69 |

|

Current assets |

41899 |

52597 |

74604 |

91016 |

145392 |

203866 |

|

Inventory |

5822 |

950 |

5979 |

5856 |

10252 |

91356 |

|

Short-term receivables |

35576 |

47514 |

57516 |

74270 |

125100 |

85124 |

|

Short-term investments |

|

|

|

903 |

886 |

|

|

Liquid assets |

441 |

3686 |

10540 |

9987 |

9154 |

25574 |

|

Prepaid expenses |

60 |

447 |

569 |

|

|

1812 |

|

Total Assets |

123078 |

131411 |

157794 |

179506 |

245391 |

478546 |

|

Equity capital |

67869 |

84021 |

111999 |

145227 |

191272 |

293949 |

|

Subscribed and paid capital |

26550 |

26550 |

29497 |

29497 |

29497 |

45823 |

|

Reserves |

11446 |

11736 |

54505 |

54505 |

54800 |

87186 |

|

Profit or loss carried forward |

29873 |

45735 |

20 |

61225 |

56930 |

160940 |

|

Profit of the year |

|

|

27977 |

|

50045 |

|

|

Loss of the year |

|

|

|

|

|

|

|

Long-term liabilities |

25102 |

16760 |

8416 |

15660 |

33568 |

88447 |

|

Short-term liabilities |

30107 |

30630 |

37379 |

18619 |

20551 |

96150 |

|

P&L ACCOUNT in BGN'000 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

|

Accounting

period: |

1.1.2008

- |

1.1.2009

- |

1.1.2010

- |

1.1.2011

- |

1.1.2012

- |

1.1.2013

- |

|

Total operating expenses |

97585 |

108486 |

125848 |

155241 |

204034 |

317785 |

|

Financial expenditures |

3975 |

1814 |

1440 |

1178 |

894 |

4194 |

|

Extraordinary expenses |

|

|

|

|

|

|

|

Profit before taxation |

10844 |

18437 |

31139 |

36928 |

55609 |

75907 |

|

Taxes |

1100 |

1844 |

3162 |

3700 |

5564 |

10163 |

|

Profit after taxation |

9744 |

16593 |

27977 |

33228 |

50045 |

65744 |

|

Total operating income |

112404 |

128737 |

158427 |

193112 |

260185 |

397789 |

|

Financial income |

|

|

|

235 |

352 |

97 |

|

Extraordinary income |

|

|

|

|

|

|

|

Loss after taxation |

|

|

|

|

|

|

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.58.86 |

|

|

1 |

Rs.98.82 |

|

Euro |

1 |

Rs.80.71 |

INFORMATION DETAILS

|

Analysis Done by

: |

KAR |

|

|

|

|

Report Prepared

by : |

PDT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

|

-- |

NB |

New Business |

-- |

|

This score serves as a reference to assess SC’s credit risk

and to set the amount of credit to be extended. It is calculated from a

composite of weighted scores obtained from each of the major sections of this

report. The assessed factors and their relative weights (as indicated through

%) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment record

(10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.