MIRA

INFORM REPORT

|

Report Date : |

06.09.2014 |

IDENTIFICATION DETAILS

|

Name : |

PASMATEX S.A |

|

|

|

|

Registered Office : |

Industrial Park ,Nea Raidestos, |

|

|

|

|

Country : |

|

|

|

|

|

Financials (as on) : |

31.12.2013 |

|

|

|

|

Date of Incorporation : |

1993 |

|

|

|

|

Com. Reg. No.: |

28192/062/Β/93/1 |

|

|

|

|

Legal Form : |

Societe Anonyme |

|

|

|

|

Line of Business : |

The subject is engaged with Imports and Wholesale Trade of Tailoring Supplies and Clothing Fabrics |

|

|

|

|

No of Employees : |

15 |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

Payment Behaviour : |

Slow but correct |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – June 01, 2014

|

Country Name |

Previous Rating (31.03.2014) |

Current Rating (01.06.2014) |

|

Greece |

B2 |

B2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low Risk |

A2 |

|

Moderate Low Risk |

B1 |

|

Moderate Risk |

B2 |

|

Moderate High Risk |

C1 |

|

High Risk |

C2 |

|

Very High Risk |

D |

GREECE - ECONOMIC OVERVIEW

Greece has a capitalist

economy with a public sector accounting for about 40% of GDP and with per

capita GDP about two-thirds that of the leading euro-zone economies. Tourism

provides 18% of GDP. Immigrants make up nearly one-fifth of the work force,

mainly in agricultural and unskilled jobs. Greece is a major beneficiary of EU

aid, equal to about 3.3% of annual GDP. The Greek economy averaged growth of

about 4% per year between 2003 and 2007, but the economy went into recession in

2009 as a result of the world financial crisis, tightening credit conditions,

and Athens' failure to address a growing budget deficit. By 2013 the economy

had contracted 26%, compared with the pre-crisis level of 2007. Greece met the

EU's Growth and Stability Pact budget deficit criterion of no more than 3% of

GDP in 2007-08, but violated it in 2009, with the deficit reaching 15% of GDP.

Austerity measures have reduced the deficit to about 4% in 2013, including

government debt payments. Deteriorating public finances, inaccurate and

misreported statistics, and consistent underperformance on reforms prompted

major credit rating agencies to downgrade Greece's international debt rating in

late 2009, and led the country into a financial crisis. Under intense pressure

from the EU and international market participants, the government adopted a

medium-term austerity program that includes cutting government spending,

decreasing tax evasion, overhauling the health-care and pension systems, and

reforming the labor and product markets. Athens, however, faces long-term

challenges to continue pushing through unpopular reforms in the face of

widespread unrest from the country's powerful labor unions and the general

public. In April 2010 a leading credit agency assigned Greek debt its lowest

possible credit rating; in May 2010, the International Monetary Fund and

Euro-Zone governments provided Greece emergency short- and medium-term loans

worth $147 billion so that the country could make debt repayments to creditors.

In exchange for the largest bailout ever assembled, the government announced

combined spending cuts and tax increases totaling $40 billion over three years,

on top of the tough austerity measures already taken. Greece, however,

struggled to meet 2010 targets set by the EU and the IMF, especially after

Eurostat - the EU's statistical office - revised upward Greece's deficit and

debt numbers for 2009 and 2010. European leaders and the IMF agreed in October

2011 to provide Athens a second bailout package of $169 billion. The second

deal however, called for holders of Greek government bonds to write down a

significant portion of their holdings. As Greek banks held a significant

portion of sovereign debt, the banking system was adversely affected by the

write down and €41 billion of the second bailout package was set aside to

ensure the banking system was adequately capitalized. In exchange for the

second loan Greece promised to introduce an additional $7.8 billion in

austerity measures during 2013-15. However, the massive austerity cuts have

prolonged Greece's economic recession and depressed tax revenues. Throughout

2013, Greece's lenders called on Athens to step up efforts to increase tax

collection, dismiss public servants, privatize public enterprises, and rein in

health spending. In June 2013 Prime Minister Antonis SAMARAS's efforts to meet

bailout conditions led to the departure of one party, the Democratic Left, from

the governing coalition when his government made the controversial decision to

shut down and restructure the state-owned television and radio company.

Subsequent reluctance to institute further cuts and delays in meeting public

sector reform targets prompted Greek lenders to withhold bailout fund

disbursements until December 2013. However, investor confidence began to show

signs of strengthening by the end of 2013 as leading macroeconomic indicators

suggested the economy’s freefall had been arrested.

|

Source

: CIA |

IDENTIFICATION DETAILS

Name: PASMATEX S.A

Address: Industrial

Park ,Nea Raidestos, P.O. Box 60613, Thermi 57001, Thessaloniki, Greece

Tel: 2310465102-3

Fax: 2310465290

Web: www.pasmatex.gr

Email: pasmatex@otenet.gr

LEGAL STATUS AND HISTORY

TAX ID: 094374359

REG. NO.: 28192/062/Β/93/1

G.E.MI.: 057631004000

YEAR STARTED: 1993

DURATION: 50 years

STATUS: Active

HISTORY:

Company was

established in 1993 having a legal seat at Thessaloniki. Company’s first legal

seat was at 34 Igilochou Str., and according to Gov.Gaz.No.:2615/94 was

transferred to the present one. In 2009 (Gov. Gaz. No.302/2009) subject

absorbed the firm PASMATZIDIS BROS & CO O.E.

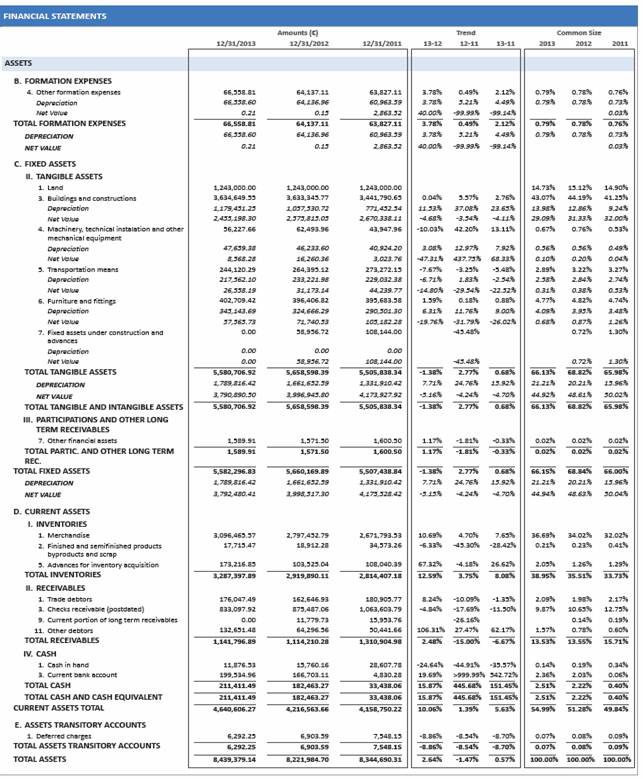

FINANCIALS

INITIAL CAPITAL:

6,500,000

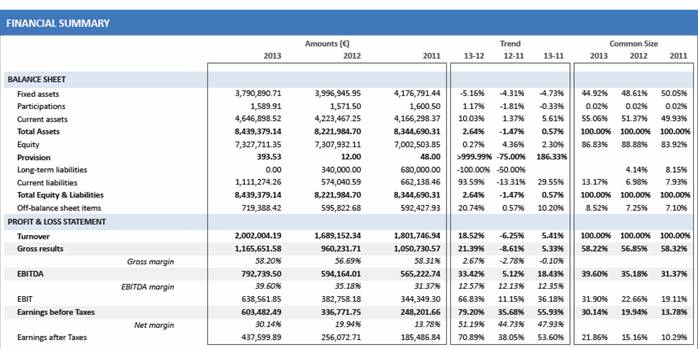

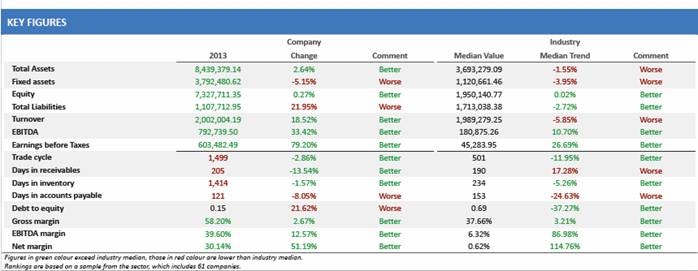

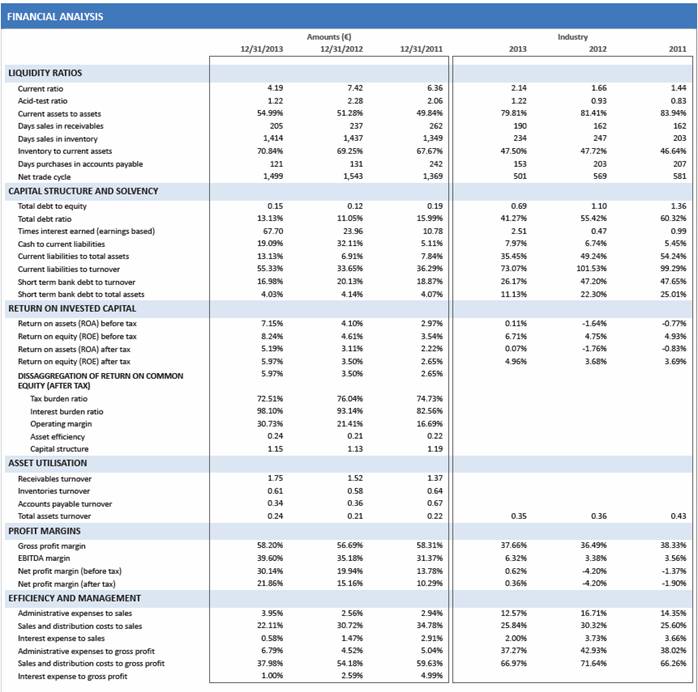

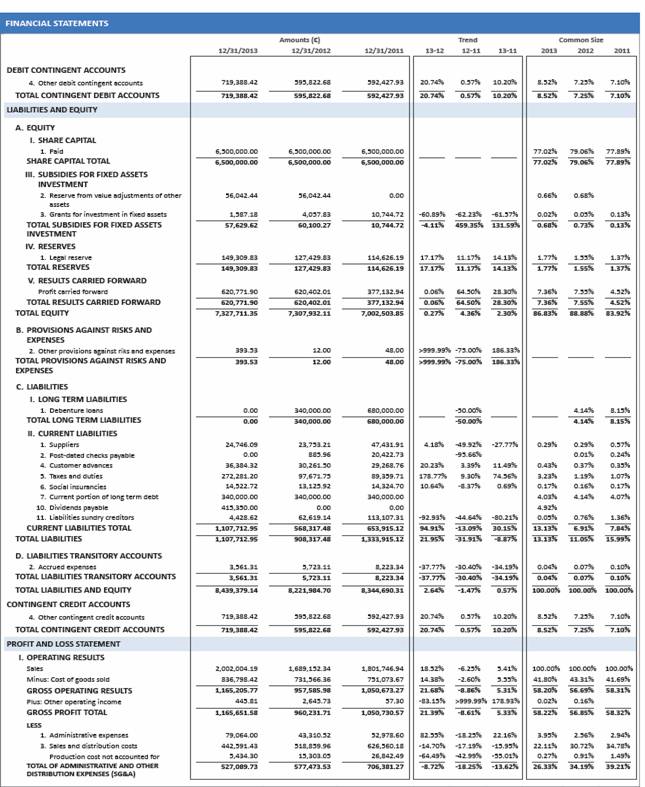

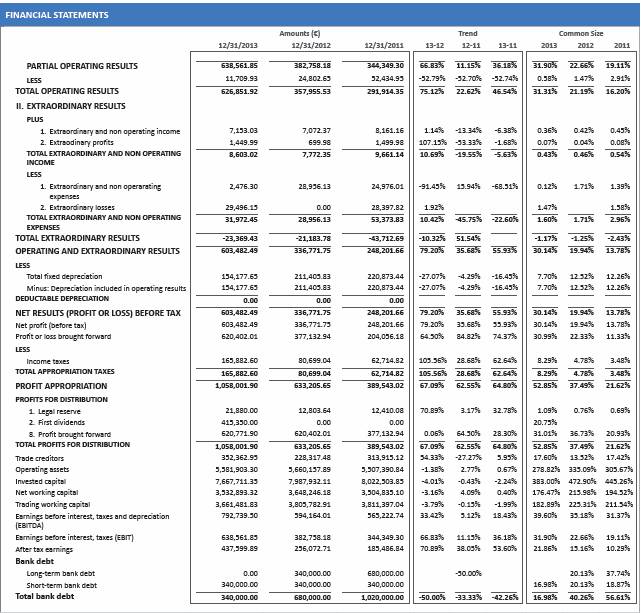

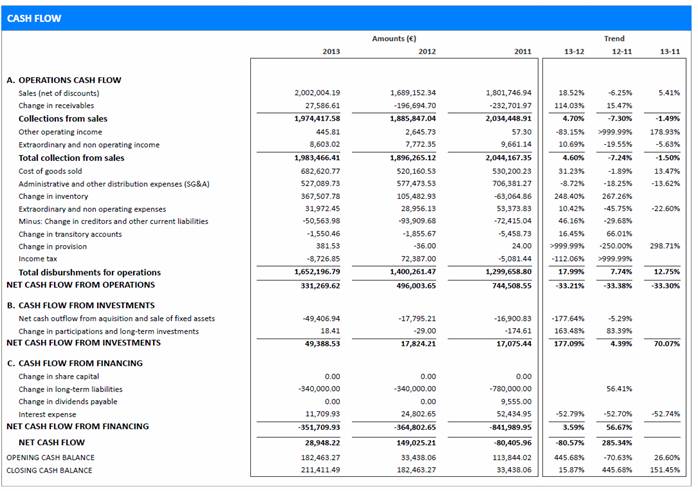

FINANCIAL BENCHMARKING ANALYSIS

Short term bank debt

decrease as percentage of total assets, at 4.03% , (4.14% in 2012) , whereas

the median ratio for the sector is estimated at 11.13% . As a percentage of

turnover it is estimated at low -and lower compared to 2012- levels, at 16.98%

, whereas the median ratio for the sector is estimated at 26.17% (short term

bank debt to sales).

Total liabilities

increase as percentage of total assets, at 13.13% , (11.05% in 2012) , whereas

the median ratio for the sector is estimated at 41.27% . Debt to equity ratio (leverage)

is estimated at very low -but increased compared to 2012- levels, at 0.15 to 1,

whereas the median ratio for the sector is estimated at 0.69 to 1. Interest

coverage by operating profit is estimated at rather high -and increased

compared to 2012- levels, at 67.70 times, whereas the median ratio for the

sector is estimated at 2.51 times.

Total current

assets grow as percentage of total assets, at 54.99% , (51.28% in 2012) ,

whereas the median ratio for the sector is estimated at 79.81% . In the same

time, current liabilities are relatevily low as a portion of total assets

(13.13%) driving the quick ratio to a very high level of 4.19 -but lower

compared to 2012- , whereas the median ratio for the sector is estimated at

2.14 . Inventory as percentage of total assets are 70.84% , (69.25% in 2012) ,

whereas the median ratio for the sector is estimated at 47.50% . In addition,

acid test ratio is at a moderate level at 1.22 -and lower compared to 2012- ,

whereas the median ratio for the sector is estimated at 1.22 .

Trade cycle is estimated at 1,499 days, (501

days the median ratio for the sector) while its duration shortens compared to

2012 by 44 days . Total assets turnover

improves at 0.24 times (0.21 in 2012), which

compared to the sector (0.35 times) is relatively low.

Gross profit margin slightly improves at

58.20% , (from 56.69% in 2012) , which is very high compared to the median

ratio in the sector (37.66% ). EBITDA margin improves at 39.60% , (from 35.18%

in 2012) , which is very high compared to the median ratio in the sector (6.32%

). Return on equity (RoE) improves at 8.24% , (from 4.61% in 2012) , which is

sufficiently high compared to the median ratio in the sector (6.71%).

ACTIVITIES

The subject is

engaged with Imports and wholesale trade of tailoring supplies and clothing

fabrics

SECTOR: White

linen and fabric

NACE INDUSTRY

51.41 Wholesale

of textiles

PRODUCTS

KIND RELATION

Garment fabrics Import,

Trade

Tailoring supplies

Import,

Trade

EXPORTS

The subject

exports to Bulgaria and FYROM

IMPORTS

The subject

imports from China, Korea, Taiwan, Province of China

EMPLOYEES

NO OF EMPLOYEES: 15

BANKERS

EMPORIKI BANK OF GREECE S.A.

Area: THERMI

Bank Number: 0120445

SENIOR COMPANY PERSONNEL

NAME TAX

ID ID NUMBER DOC DATE START

DATE

Theodoros Kyr.

Pasmatzidis 036639200 ΑΕ206401 6755-2011

Board Chairman,

Chief Executive Officer

Efimia Kyr.

Pasmatzidou Χ772516

6755-2011

Board Vice

Chairman

Dimitrios Pas.

Adamidis 045417102 Φ 154215 6755-2011

Board Member

Kyriakos The.

Pasmatzidis 002152630 Ζ287004

Legal

Representative

SHAREHOLDERS

FULL NAME PERCENT

TAX ID ID NUMBER

Theodoros

Pasmatzidis 38.00% 036639200 ΑΕ206401

Kyriakos

Pasmatzidis 30.00% 002152630

Ζ287004

Efimia Pasmatzidou

25.00%

Χ772516

Evangelia

Karatziki 7.00%

Κ405964

PROPERTIES

The subject owns

LAND m2: 14000 and BUILDINGS m2: 4000

WAREHOUSE

Industrial Area,

Thermi 57001, Thessaloniki

OWNERSHIP: Owned, BUILDINGS

m2: 5000

WAREHOUSE

Industrial Area,,

Thermi 57001, Thessaloniki

OWNERSHIP: Owned,

BUILDINGS m2: 1601

WAREHOUSE

Industrial Area,

Thermi 57001, Thessaloniki

OWNERSHIP: Owned,

BUILDINGS m2: 1000

PAYMENTS

Outstanding

trading behavior. The company depicts smooth transaction track record, without

any detrimentals affecting its business.

GENERAL COMMENTS

Please note that the information provided in the report was obtained from

official and available sources.

Further information was not available.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.60.44 |

|

|

1 |

Rs.98.64 |

|

Euro |

1 |

Rs.78.20 |

INFORMATION DETAILS

|

Analysis Done by

: |

DIV |

|

|

|

|

Report Prepared

by : |

TPT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General unfavourable

factors will not cause fatal effect. Satisfactory capability for payment of

interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to

overcome financial difficulties seems comparatively below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with full

security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess SC’s credit risk and

to set the amount of credit to be extended. It is calculated from a composite

of weighted scores obtained from each of the major sections of this report. The

assessed factors and their relative weights (as indicated through %) are as

follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend

(10%) Operational

size (10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.