MIRA INFORM REPORT

|

Report No. : |

338295 |

|

Report Date : |

28.08.2015 |

IDENTIFICATION DETAILS

|

Name : |

ROMEO TEXTILE LIMITED |

|

|

|

|

Registered Office : |

Complex

La Providence Royal Road Curepipe |

|

|

|

|

Country : |

Mauritius

|

|

|

|

|

Financials (as on) : |

30.06.2014 |

|

|

|

|

Date of Incorporation : |

07.05.2013 |

|

|

|

|

Com. Reg. No.: |

C116166 |

|

|

|

|

Legal Form : |

Limited Corporation |

|

|

|

|

Line of Business : |

Registered to operate

import and export. |

|

|

|

|

No. of Employees : |

10 |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

Payment Behaviour : |

No Complaints |

|

Litigation : |

Clear |

NOTES:

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31, 2015

|

Country Name |

Previous Rating (31.12.2014) |

Current Rating (31.03.2015) |

|

Mauritius |

A2 |

A2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

MAURITIUS - ECONOMIC OVERVIEW

Since independence in 1968, Mauritius has undergone a

remarkable economic transformation from a low-income, agriculturally based economy

to a diversified, upper middle-income economy with growing industrial,

financial, and tourist sectors. Mauritius has achieved steady growth over the

last several decades, resulting in more equitable income distribution,

increased life expectancy, lowered infant mortality, and a much-improved

infrastructure. The economy rests on sugar, tourism, textiles and apparel, and

financial services, and is expanding into fish processing, information and

communications technology, and hospitality and property development. Sugarcane

is grown on about 90% of the cultivated land area and accounts for 15% of

export earnings. The government's development strategy centers on creating

vertical and horizontal clusters of development in these sectors. Mauritius has

attracted more than 32,000 offshore entities, many aimed at commerce in India,

South Africa, and China. Investment in the banking sector alone has reached

over $1 billion. Mauritius’ textile sector has taken advantage of the Africa

Growth and Opportunity Act, with Mauritian exports to the US growing by 400%

from 2001-2012. Mauritius' sound economic policies and prudent banking

practices helped to mitigate negative effects of the global financial crisis in

2008-09. GDP grew in the 3-4% per year range in 2010-14, and the country

continues to expand its trade and investment outreach around the globe.

|

Source

: CIA |

Company

name

|

|

||

|

Registered Name: |

ROMEO TEXTILE

LIMITED |

||

|

Requested Name: |

ROMEO TEXTILE LIMITED |

||

|

Other Names: |

None |

||

|

|

|||

ADDRESS

AND TELECOMMUNICATION

|

|||

|

Physical Address: |

Complex

La Providence Royal Road Curepipe |

||

|

Country: |

Mauritius |

||

|

Phone: |

230-675289 |

||

|

Fax: |

230-675289 |

||

|

Email: |

None |

||

|

Website: |

None |

||

|

|

|||

CREDIT

OPINION

|

|

||

|

Financial Index as of

December 2014 shows subject firm with a medium risk of credit. However, bank

and credit information obtained reveal a history of prompt payments. |

|||

|

|

|||

LEGAL

|

|

||

|

Legal Form: |

Limited Corporation |

||

|

Date Incorporated: |

07-May-2013 |

||

|

Reg. Number: |

C116166 |

||

|

Nominal Capital |

MUR.

100,000 |

||

|

Subscribed Capital |

MUR.

100,000 |

||

|

Subscribed Capital is Subscribed in the following form: |

|||

|

|

Position |

Shares |

|

|

Li Ying Pin Ah Kee David |

Director |

100% |

|

|

Veerapen Coomarashinee |

Secretary |

|

|

|

|

|||

RELATED

COMPANIES

|

|||

|

None |

Parent company. |

||

|

None |

Subsidiary company. |

||

|

None |

Affiliated company. |

||

|

Li Ying Pin Ah Kee David |

Shareholder of subject

firm. |

||

|

None |

Branches of the firm |

||

|

|

|||

OPERATIONS

|

|||

|

Registered to operate

import and export |

|||

|

Imports: |

Asia |

||

|

Exports: |

Neighboring islands |

||

|

Trademarks: |

None |

||

|

Terms of sale: |

Cash (40%) and 25-90 days (60%), invoices. |

||

|

|

|

||

|

Main Customers: |

firms and organizations |

||

|

Employees: |

10 employees. |

||

|

Vehicles: |

Several motor vehicles. |

||

|

Territory of sales: |

Mauritius |

||

|

Location: |

Rented premises, 1,500 square feet, |

||

|

|

|||

AUDITORS

AND INSURANCE

|

|||

|

Auditors: |

Information not

available. |

||

|

Insurance Brokers: |

Information not

available. |

||

|

|

|

||

FINANCE

|

|

||

|

Currency Reported: |

Mauritius Rupee (MUR.) |

||

|

Approx. Ex. Rate: |

1 US Dollar = 35.04

Mauritius Rupee |

||

|

Fiscal Year End: |

December 31, 2014 |

||

|

Inflation: |

According to information given by independent sources, the inflation

at December 31st, 2014 was of 13%. |

||

|

|

|||

|

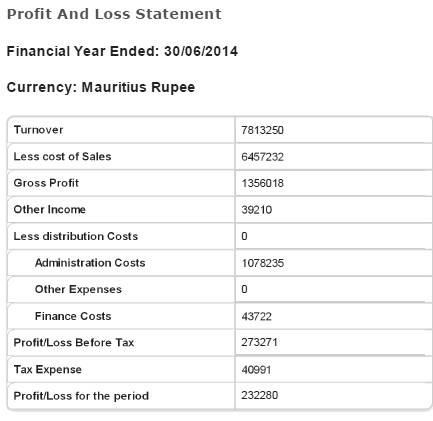

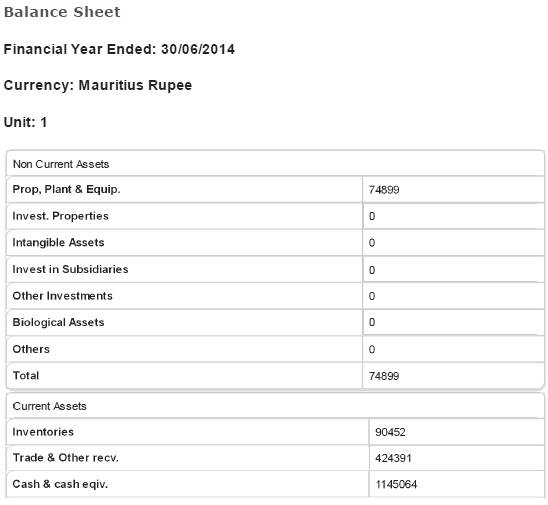

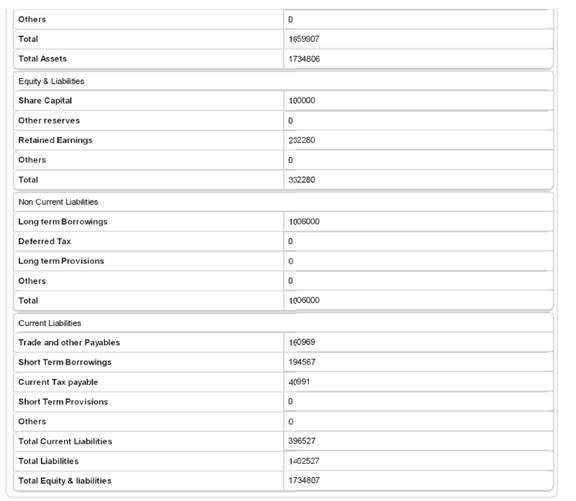

Financial Information

Submitted Below |

|

||

|

|

|

||

BANK

|

|

||

|

Bank Name: |

MCB

BANK |

||

|

Branch: |

Mauritius |

||

|

Comments: |

None |

||

|

|

|

||

TRADE REFERENCES

|

|||

|

Experiences: |

Good |

||

|

|

|

||

NOTARIAL BONDS

None |

|||

|

|

|||

COMMENTS

/ ADDITIONAL INFORMATION

|

|||

|

This information was obtained

from outside sources other than the subject company itself and confirmed the

above subject. |

|||

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.66.06 |

|

|

1 |

Rs.102.35 |

|

Euro |

1 |

Rs.74.97 |

INFORMATION DETAILS

|

Analysis Done by

: |

KAS |

|

|

|

|

Report Prepared

by : |

TPT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest capability

for timely payment of interest and principal sums |

Unlimited |

|

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

|

-- |

NB |

New Business |

-- |

|

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is

calculated from a composite of weighted scores obtained from each of the major sections

of this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.