MIRA INFORM REPORT

|

Report No. : |

304977 |

|

Report Date : |

02.02.2015 |

IDENTIFICATION DETAILS

|

Name : |

ECOBANK GABON SA |

|

|

|

|

Registered Office : |

214 Avenue Bouet, 9 Etarge Montangne, BP 12111 Libreville |

|

|

|

|

Country : |

Gabon |

|

|

|

|

Financials (as on) : |

31.12.2013 (Consolidated) |

|

|

|

|

Date of Incorporation : |

05.05.2009 |

|

|

|

|

Legal Form : |

Societe Anonyme |

|

|

|

|

Line of Business : |

Providers of Banking and

Related Financial Services. |

|

|

|

|

No. of Employees : |

70 Employees. |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

NOTES:

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – September 30, 2014

|

Country Name |

Previous Rating (30.06.2014) |

Current Rating (30.09.2014) |

|

Gabon |

B1 |

B1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

GABON - ECONOMIC

OVERVIEW

Gabon enjoys a per capita

income four times that of most sub-Saharan African nations, but because of high

income inequality, a large proportion of the population remains poor. Gabon

depended on timber and manganese until oil was discovered offshore in the early

1970s. The economy was reliant on oil for about 50% of its GDP, about 70% of

revenues, and 87% of goods exports for 2010, although some fields have passed

their peak production. A rebound of oil prices from 1999 to 2008 helped growth,

but declining production has hampered Gabon from fully realizing potential

gains. Gabon signed a 14-month Stand-By Arrangement with the IMF in May 2007,

and later that year issued a $1 billion sovereign bond to buy back a sizable

portion of its Paris Club debt. Gabon continues to face fluctuating prices for

its oil, timber, and manganese exports. Despite the abundance of natural

wealth, poor fiscal management has stifled the economy. However, President

BONGO ONDIMBA has made efforts to increase transparency and is taking steps to

make Gabon a more attractive investment destination to diversify the economy.

BONGO ONDIMBA has attempted to boost growth by increasing government investment

in human resources and infrastructure. GDP grew more than 6% per year over the

2010-13 period.

|

Source

: CIA |

SUBJECT'S

NAME

|

Registered Name: |

ECOBANK GABON SA |

|

Requested Name: |

ECOBANK GABON SA |

|

Other Names: |

None |

ADDRESS

AND TELECOMMUNICATION

|

Physical Address: |

214

Avenue Bouet, 9 Etarge Montangne |

|

Postal Address: |

BP

12111 |

|

|

Libreville |

|

Country: |

Gabon |

|

Phone: |

241-1-761270/71/73 |

|

Fax: |

241-1-761275 |

|

Email: |

|

|

Website: |

LEGAL

|

Legal Form: |

Societe Anonyme |

|

|

Date Incorporated: |

05-May-2009 |

|

|

Reg. Number: |

Gabon |

|

|

SWIFT: |

ECOCGALI |

|

|

Nominal Capital |

CFA.

10,000,000 |

|

|

Subscribed Capital |

CFA.

10,000,000 |

|

|

Subscribed Capital is Subscribed in the following form: |

||

|

|

Position |

Shares |

|

Mr. Owondault Berre

Joseph |

Chairman |

|

|

Mr. Jean-Baptiste Siate |

CEO/GM |

|

|

Mr. Guedon Désiré |

Ass.

GM |

|

|

Private Investors |

Shareholder |

25% |

|

Ecobank Transnational Inc. |

Holding

Co. |

75% |

RELATED

COMPANIES

|

Ecobank Transnational

Inc. |

Parent company. |

|

None |

Subsidiary company. |

|

Listed Below |

Affiliated companies. |

|

None |

Shareholder of subject

firm. |

|

None |

Branches of the firm |

OPERATIONS

|

Registered to operate as

providers of banking and related financial services |

|

|

Imports: |

Asia |

|

Exports: |

None |

|

Trademarks: |

None |

|

Terms of sale: |

Cash (20%) and 25-90 days (80%), invoices. |

|

|

|

|

Main Customers: |

General Public |

|

Employees: |

70 employees. |

|

Vehicles: |

Several motor vehicles. |

|

Territory of sales: |

Gabon |

|

Location: |

Leased premises, 100,000 square feet, |

AUDITORS

AND INSURANCE

|

Auditors: |

PRICE WATERHOUSE COOPERS |

|

Insurance Brokers: |

Information not

available. |

FINANCE

|

Currency Reported: |

West African Franc (CFA.) |

|

Approx. Ex. Rate: |

1 US Dollar = 579.72 West

African Franc |

|

Fiscal Year End: |

December 31, 2014 |

|

Inflation: |

According to information given by independent sources, the inflation

at December 31st, 2014 was of 13%. |

|

|

|

|

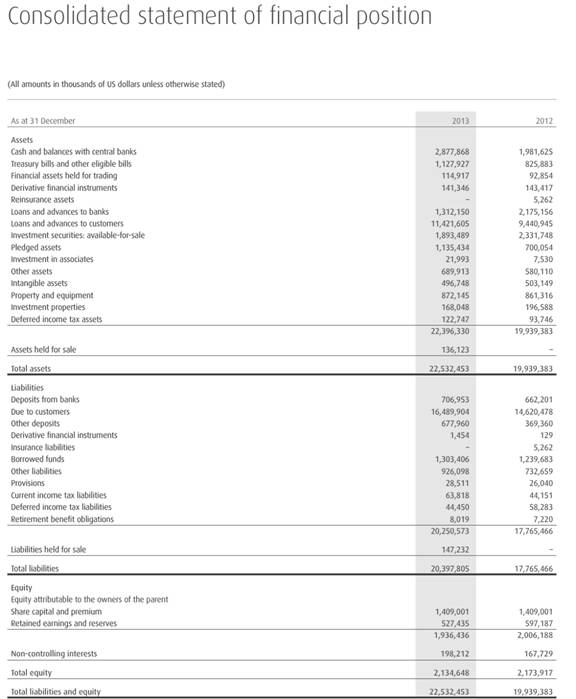

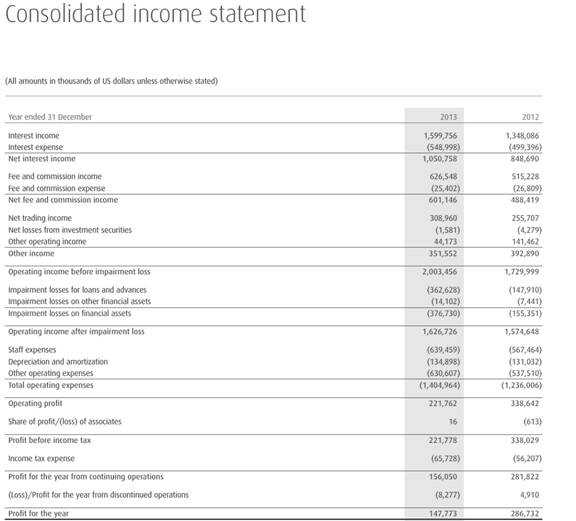

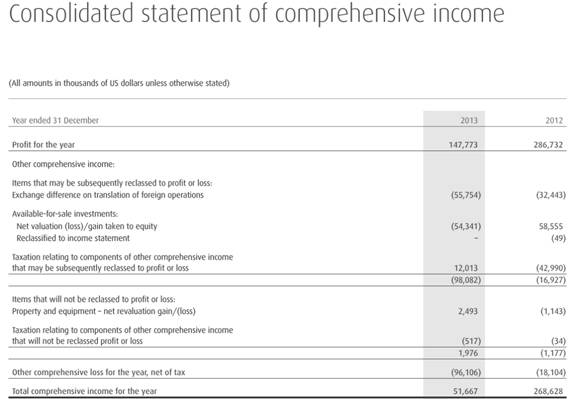

Group Financial

Information Submitted Below |

|

BANK

|

Bank Name: |

Self |

|

Branch: |

Gabon |

|

Comments: |

None |

TRADE REFERENCES

|

Experiences: |

Good |

NOTARIAL BONDS

None

COMMENTS

/ ADDITIONAL INFORMATION

|

This information was obtained

from outside sources other than the subject company itself and confirmed the

above subject. |

AFFILIATED

COMPANIES

|

ECOBANK SENEGAL |

|

ECOBANK SIERRA LEONE |

|

ECOBANK SOUTH AFRICA (REPRESENTATIVE OFFICE IN JOHANNESBURG) |

|

ECOBANK TANZANIA |

|

ECOBANK CAPE VERDE |

|

ECOBANK CENTRAL AFRICAN REPUBLIC |

|

ECOBANK CHAD |

|

ECOBANK CONGO BRAZZAVILLE |

|

ECOBANK CÔTE D'IVOIRE |

|

ECOBANK TOGO |

|

ECOBANK UGANDA |

|

ECOBANK ZAMBIA |

|

ECOBANK ZIMBABWE |

|

ECOBANK GUINEA |

|

ECOBANK GUINEA-BISSAU |

|

ECOBANK LIBERIA |

|

ECOBANK MALAWI |

|

ECOBANK MALI |

|

ECOBANK MOZAMBIQUE |

|

ECOBANK NIGER |

|

ECOBANK NIGERIA |

|

ECOBANK RWANDA |

|

ECOBANK SÃO TOMÉ AND PRÍNCIPE |

|

ECOBOANK ANGOLA |

|

ECOBANK BENIN |

|

ECOBANK BURKINA FASO |

|

ECOBANK BURUNDI |

|

ECOBANK CAMEROON |

|

ECOBANK DEMOCRATIC REPUBLIC OF THE CONGO |

|

ECOBANK ETHIOPIA |

|

ECOBANK EQUATORIAL GUINEA |

|

ECOBANK GAMBIA |

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.61.76 |

|

|

1 |

Rs.93.13 |

|

Euro |

1 |

Rs.70.03 |

INFORMATION DETAILS

|

Analysis Done by

: |

KAR |

|

|

|

|

Report Prepared

by : |

NIT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

|

-- |

NB |

New Business |

-- |

|

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is calculated

from a composite of weighted scores obtained from each of the major sections of

this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment record

(10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.