MIRA

INFORM REPORT

|

Report No. : |

301200 |

|

Report Date : |

05.01.2015 |

IDENTIFICATION DETAILS

|

Name : |

NEW ZEALAND WOOL SERVICES INTERNATIONAL

LIMITED |

|

|

|

|

Registered Office : |

First Floor, 30 Sir William Pickering Drive, Christchurch, Zip Code 8053 |

|

|

|

|

Country : |

New Zealand |

|

|

|

|

Financials (as on) : |

30.06.2013 (Consolidated) |

|

|

|

|

Date of Incorporation : |

13.12.1991 |

|

|

|

|

Com. Reg. No.: |

530665 |

|

|

|

|

Legal Form : |

Private Limited Liability Company |

|

|

|

|

Line of Business : |

Engaged as Producer and exporter

of Wool Scourer. |

|

|

|

|

No of Employees : |

100+ |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

|

With Financials |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

Payment Behaviour : |

No Complaints |

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – September 30, 2014

|

Country Name |

Previous Rating (30.06.2014) |

Current Rating (30.09.2014) |

|

New Zealand |

a1 |

a1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

New Zealand ECONOMIC OVERVIEW

Over the past 20 years the government has transformed

New Zealand from an agrarian economy dependent on concessionary British market

access to a more industrialized, free market economy that can compete globally.

This dynamic growth has boosted real incomes - but left behind some at the

bottom of the ladder - and broadened and deepened the technological

capabilities of the industrial sector. Per capita income rose for ten consecutive

years until 2007 in purchasing power parity terms, but fell in 2008-09.

Debt-driven consumer spending drove robust growth in the first half of the

decade, helping fuel a large balance of payments deficit that posed a challenge

for economic managers. Inflationary pressures caused the central bank to raise

its key rate steadily from January 2004 until it was among the highest in the

OECD in 2007-08; international capital inflows attracted to the high rates

further strengthened the currency and housing market, however, aggravating the

current account deficit. The economy fell into recession before the start of

the global financial crisis and contracted for five consecutive quarters in

2008-09. In line with global peers, the central bank cut interest rates aggressively

and the government developed fiscal stimulus measures. The economy pulled out

of recession late in 2009, and achieved 2-3% per year growth in 2010-13.

Nevertheless, key trade sectors remain vulnerable to weak external demand. The

government plans to raise productivity growth and develop infrastructure, while

reining in government spending.

|

Source : CIA |

IDENTIFICATION

|

|

|||

|

Subject name: |

|||

|

Address: |

Postal address: |

||

|

Town: |

Town: |

||

|

Zip/postal code: |

Zip/postal code: |

||

|

Country: |

|||

|

Telephone: |

|||

|

Fax: |

|||

|

Email: |

|||

|

Website: |

|||

|

|

|

||

|

|

|

||

EXECUTIVE SUMMARY

|

|||

|

|

|

||

|

Date registered: |

|||

|

Legal form: |

|||

|

Main activities: |

|||

|

Employees: |

|||

|

|

|

||

|

Strong financial

and operational base. Medium to large credits can be considered with high

confidence that commitments can be met under most circumstances. Normal

credit control policy applies. |

|

|

|

|

REGISTRY DATA |

|

|

Key Facts |

|

|

Date registered: |

|

|

Legal form: |

|

|

Registration no: |

|

|

Registry auth. |

|

|

Other reg.: |

|

|

Registry status: |

|

|

|

|

|

|

|

LEGAL FILINGS |

|

|

|

|

|

Bankruptcy filings: |

|

|

Court judgements: |

|

|

Tax liens: |

|

|

Other: |

|

|

|

|

|

|

|

MANAGEMENT & STAFF |

|

|

|

|

|

|

|

|

Name: |

Michael Dwyer |

|

Job title: |

Chief Executive Officer |

|

|

|

|

Name: |

Geoff Deakins |

|

Job title: |

Financial Controller |

|

|

|

|

Name: |

John Dawson |

|

Job title: |

General Manager |

|

|

|

|

Name: |

Paul Steel |

|

Job title: |

Marketing Manager |

|

|

|

|

Name: |

Malcolm Ching |

|

Job title: |

Purelana Manager |

|

|

|

|

Name: |

Jason Stewart |

|

Job title: |

Shipping Manager |

|

|

|

|

|

|

|

No of employees |

|

|

|

|

|

|

|

BOARD OF DIRECTORS / OTHER APPOINTMENTS |

|

|

|

|

|

Malvern, VIC

3144 Australia |

|

|

|

|

|

|

|

SHARE CAPITAL

|

|

|

Composition |

|

|

Number/type: |

|

|

Share value: |

|

|

Issued: |

|

|

Paid-up: |

|

|

|

|

|

|

|

Shareholders/Owners

|

|

|

|

|

|

|

|

|

|

|

|

Melbourne, VIC 3000 New Zealand |

|

|

|

|

|

|

|

CORPORATE AFFILIATIONS |

|

|

|

|

|

Melbourne, VIC 3000 New Zealand |

|

|

|

|

|

Name: |

KAPUTONE WOOL SCOUR (1994) LIMITED |

|

Affiliation

type: |

Wholly-owned Subsidiary |

|

Address: |

New Zealand |

|

|

|

|

Name: |

RAYMOND DALE WOOL MARKETING LIMITED |

|

Affiliation

type: |

Wholly-owned Subsidiary |

|

Address: |

New Zealand |

|

|

|

|

Name: |

WHAKATU WOOL SCOUR LIMITED |

|

Affiliation

type: |

Wholly-owned Subsidiary |

|

Address: |

New Zealand |

|

|

|

|

|

|

BANKING & FINANCING

|

|

|

|

|

|

|

|

|

Time of Registration: 19-Apr-2010 14:26 Debtor Name: NEW ZEALAND WOOL SERVICES INTERNATIONAL LIMITED Financing Statement Registration No: FC1RM214ED992342/C0003 Incorporation No: 530665 City/Town: Fendalton Christchurch Collateral Type: All Present And After Acquired Personal Property Time of Registration: 18-Oct-2011 12:57 Debtor Name: NEW ZEALAND WOOL SERVICES INTERNATIONAL LIMITED Financing Statement Registration No: F617ZF2NF2766227/C0001 Incorporation No: 530665 City/Town: Christchurch Collateral Type: Goods - Other Time of Registration: 23-Jun-2014 11:16 Debtor Name: NEW ZEALAND WOOL SERVICES INTERNATIONAL LIMITED Financing Statement Registration No: FM15XV2M9J245248 Incorporation No: 530665 City/Town: Christchurch Collateral Type: Goods - Other Time of Registration: 23-Jun-2014 11:35 Debtor Name: NEW ZEALAND WOOL SERVICES INTERNATIONAL LIMITED Financing Statement Registration No: F262XT41HB40749B Incorporation No: 530665 City/Town: Christchurch Collateral Type: Goods - Other |

|

|

|

|

|

It is generally not the policy of local

banks to provide credit status information to non-bona fide applications, and

interested parties would be advised to consult first with the Subject if

banker's references are required. |

|

|

|

|

|

|

|

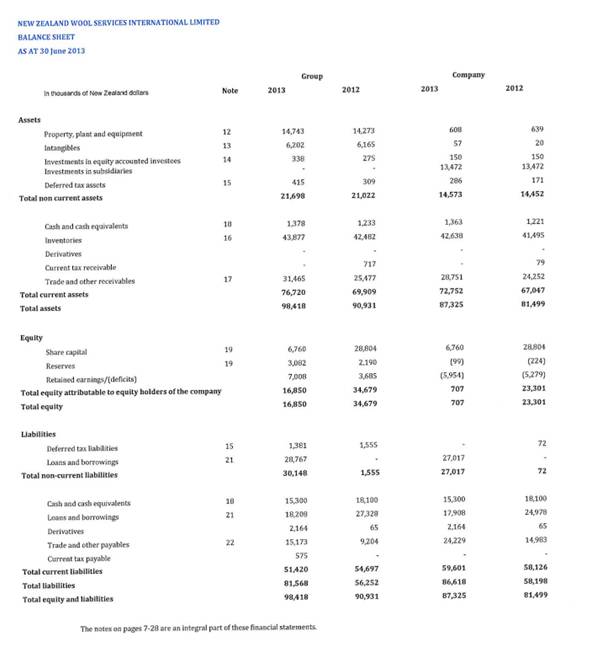

FINANCIAL ACCOUNTS |

|

|

|

|

|

Required to file: |

|

|

Source: |

|

|

Presentation: |

|

|

Date of

accounts: |

|

|

Type of

accounts: |

|

|

Currency: |

|

|

Exchange rate: |

|

|

|

|

Summarised

|

|

|||

|

|

|

|

|

|

|

|

||

|

|

|

||

OPERATIONS & HISTORY |

|||

|

|

|||

|

Full

description: |

The Subject is engaged as producer and

exporter of New Zealand wool scourer. |

||

|

Brands: |

GLACIAL RED BAND PURE TT |

||

|

|

|

||

|

|

|||

|

Export: |

|||

|

|

|

||

|

|

|||

PROPERTY & ASSETS

|

|||

|

|

|

||

|

The Subject

principally operates from premises located at the heading address, consisting

of administrative offices. |

|||

|

|

|

||

|

|

|||

PAYMENTS |

|||

|

|

|||

|

Local: |

Credits 14-30 days |

||

|

Imports: |

Credits 30 days

net |

||

|

|

|

||

|

|

|||

|

Local: |

Credits 14-30 days |

||

|

Exports: |

Credits 30 days

net |

||

|

|

|

||

|

|

|

||

|

|

|||

|

As trade references were not supplied, the

Subject's payment track record history CANNOT BE ACCURATELY DETERMINED, but

payments are believed to be PROMPT. |

|||

|

|

|||

|

|

|||

INVESTIGATIVE NOTES

|

|||

|

|

|

||

|

Sources: |

Interviews and material provided by the Subject Other official

and local business sources |

||

|

|

|

||

|

|

|

||

ATTACHMENTS

|

|||

|

|

|

||

|

Attachments: |

Financial ratios |

||

|

|

|

||

Financial Ratios |

|||

|

|

30-06-2013 |

30-06-2012 |

Trend |

|

PROFITABILITY

[%] |

|

|

|

|

Gross

Margin |

8.15% |

5.9% |

38.14% |

|

Gross Profit / Sales Turnover * 100 |

|

|

|

|

Operating

Margin |

N/A |

N/A |

N/A |

|

Operating Profit / Sales Turnover *

100 |

|

|

|

|

Net

Profit Margin |

1.8% |

1.11% |

62.16% |

|

Profit After Tax / Sales

Turnover * 100 |

|

|

|

|

Return

On Equity (ROE) |

19.72% |

6.45% |

205.74% |

|

Profit After Tax / Equity * 100 |

|

|

|

|

Return

On Assets (ROA) |

3.38% |

2.46% |

37.4% |

|

Profit After Tax / Total Assets *

100 |

|

|

|

|

Return

On Investment (ROI) |

26.87% |

9.14% |

193.98% |

|

Profit Before Tax / Equity *

100 |

|

|

|

|

EFFICIENCY

[%] |

|

|

|

|

Asset

Turnover |

187.78% |

222.11% |

-15.46% |

|

Sales Turnover / Total Assets * 100 |

|

|

|

|

Inventory

Turnover |

421.2% |

475.43% |

-11.41% |

|

Sales Turnover / Inventory * 100 |

|

|

|

|

LIQUIDITY

[%] |

|

|

|

|

Current

Ratio (CR) |

149.2% |

127.81% |

16.74% |

|

Current Assets / Current Liabilities * 100 |

|

|

|

|

Quick

Ratio (QR) |

63.87% |

50.14% |

27.38% |

|

(Current Assets – Inventory) /

Current Liabilities * 100 |

|

|

|

|

DEBT

[%] |

|

|

|

|

Debt

Ratio |

82.88% |

61.86% |

33.98% |

|

Total Liabilities / Total Assets *

100 |

|

|

|

|

Long-Term

Debt Ratio |

178.92% |

4.48% |

3893.75% |

|

Long-Term Liabilities / Equity *

100 |

|

|

|

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.63.29 |

|

UK Pound |

1 |

Rs.98.39 |

|

Euro |

1 |

Rs.76.31 |

INFORMATION DETAILS

|

Analysis Done by

: |

RAS |

|

|

|

|

Report Prepared

by : |

MNL |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is

calculated from a composite of weighted scores obtained from each of the major

sections of this report. The assessed factors and their relative weights (as

indicated through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment

record (10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.