MIRA INFORM REPORT

|

Report No. : |

322254 |

|

Report Date : |

21.05.2015 |

IDENTIFICATION DETAILS

|

Name : |

KELANI VALLEY PLANTATIONS PLC |

|

|

|

|

Registered Office : |

# 400, Deans Road, Colombo 10 |

|

|

|

|

Country : |

Sri Lanka |

|

|

|

|

Financials (as on) : |

31.12.2013 |

|

|

|

|

Date of Incorporation : |

18.06.1992 |

|

|

|

|

Com. Reg. No.: |

PQ 58 |

|

|

|

|

Legal Form : |

Public Limited Liability Company (in operation) listed with Colombo Stock Exchange |

|

|

|

|

Line of Business : |

Production & processing of tea & Rubber. |

|

|

|

|

No. of Employee : |

Approximately 13,000 |

RATING & COMMENTS

|

MIRA’s Rating : |

Ba |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

Status : |

Satisfactory |

|

|

|

|

Payment Behaviour : |

No complaints |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made on

e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – December 31, 2014

|

Country Name |

Previous Rating (30.09.2014) |

Current Rating (31.12.2014) |

|

Sri Lanka |

A2 |

A2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

SRI LANKA ECONOMIC OVERVIEW

Sri Lanka continues to experience strong economic growth following the end of the 26-year conflict with the Liberation Tigers of Tamil Eelam. The government has been pursuing large-scale reconstruction and development projects in its efforts to spur growth in war-torn and disadvantaged areas, develop small and medium enterprises and increase agricultural productivity. The government's high debt payments and bloated civil service have contributed to historically high budget deficits, but fiscal consolidation efforts and strong GDP growth in recent years have helped bring down the government's fiscal deficit. However, low tax revenues are a major concern. The 2008-09 global financial crisis and recession exposed Sri Lanka's economic vulnerabilities and nearly caused a balance of payments crisis. Agriculture slowed due to a drought and weak global demand affected exports and trade. In early 2012, Sri Lanka floated the rupee, resulting in a sharp depreciation, and took steps to curb imports. A large trade deficit remains a concern, but strong remittances from Sri Lankan workers abroad help offset the trade deficit. Government debt of about 80% of GDP remains among the highest in emerging markets.

|

Source

: CIA |

GENERAL

- Basic information at a glance

|

a. |

Name of Subject of Inquiry |

: |

KELANI VALLEY PLANTATIONS PLC |

|

b. |

Legal Form & Status |

: |

Public Limited

Liability Company (in operation) listed with Colombo Stock Exchange |

|

c. |

Chairman |

: |

A.M. Pandithage |

|

d. |

Primary Line of Business |

: |

Production &

processing of tea & Rubber |

|

e. |

Head Office |

: |

# 400, Deans Road, Colombo 10, Sri Lanka. Tel. No: (00 94

11) 262 7700, 268 6274-5 Fax No: (00 94 11) 269 4216 E Mail: postmaster@kvpl.com |

|

f. |

No. of Employees |

: |

Approximately 13,000 |

COMPANY

DETAILS

- Registration and Shareholder Details

|

a. |

Registration No |

: |

N(PBS/CGB) 127 |

|

|

Date of Registration |

: |

18th June 1992 |

||

|

b. |

Re-registration No |

: |

PQ 58 |

|

|

c. |

Registered Office |

: |

# 400, Deans Road, Colombo 10 |

|

|

d. |

Board of Directors As At 31st March 2015 |

: |

A.M. Pandithage |

Chairman |

|

W.G.R Rajadurai |

Managing Director |

|||

|

F. Mohideen |

Director |

|||

|

S. Siriwardana |

Director |

|||

|

S.C. Ganegoda |

Director |

|||

|

L.T.

Samarawickrama |

Director |

|||

|

Dr. K.I.M.

Ranasoma |

Director |

|||

|

C.V. Cabraal |

Director |

|||

|

L.N. De. S.

Wijeyeratne |

Director |

|||

Registration and Shareholder Details

|

Issued Share Capital |

: |

Rs. 340,000,000.00 |

||

|

Number of Shares |

: |

34,000,000 |

||

|

f. |

Nominal Value of Share |

: |

Not

applicable/declared vide Companies Act #7 of 2007 |

|

|

h. |

Major Share Holders As At 31st December 2013 (Total Number of Share Holders – 14,279) |

|

Major Share Holders |

No. of Shares |

|

DPL Plantations

(Pvt) Ltd |

24,200,000 |

|||

|

Waldock

Mackenzie Ltd./Mr. L P Hapangama Mr. L P

Hapangama |

2,819,213 400 |

|||

|

Bank of Ceylon

A/c Ceybank Unit Trust |

1,992,642 |

|||

|

Mabroc Holdings

(Pvt) Ltd |

512,746 |

|||

|

Bank of Ceylon

A/c Ceybank Century Growth Fund |

459,984 |

|||

|

AIA Insurance

Lanka PLC - A/C No. 7 AIA Insurance

Lanka PLC - A/C No. 6 |

379,172 30,100 |

|||

|

T T T Al-Nakib |

344,122 |

|||

|

H A A H

Algharabally |

150,000 |

|||

|

i. |

Auditors |

: |

Messrs. Ernst

& Young |

|

|

j. |

Company Secretaries |

: |

Hayleys Group

Services (Private) Limited 400, Deans Road,

Colombo 10 |

|

|

k. |

Bankers |

: |

Bank of Ceylon NDB Bank Sampath Bank Seylan Bank Hatton National

Bank DFCC Bank Citibank People’s Bank |

|

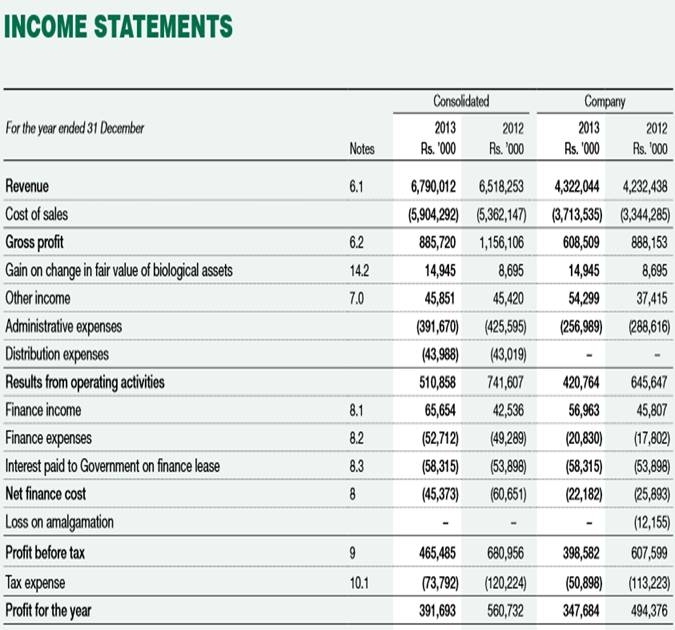

FINANCIAL

DETAILS

-

Most recent available Financial Information

FINANCIAL DETAILS - Most recent available

Financial Information (Cont/d…)

CURRENT

INVESTIGATION

Company Logo

- History.

The Subject Company KELANI VALLEY PLANTATIONS PLC is a Public

Limited Liability Company listed with Colombo Stock Exchange incorporated on 18th

June 1992 under registration number N(PBS/CGB) 127 and then the

company was re-registered under the registration number PQ 58 in terms of Companies Act #7 of 2007.

Kelani Valley Plantations PLC (KVPL) is a Subsidiary of Dipped Products

PLC (DPL).

Kelani Valley Plantations PLC subsidiary companies as follow;

Kalupahana Power Company (Private) Limited

Kelani Valley Instant Tea (Private) Limited

Mabroc Teas (Private) Limited

Hayleys Global Beverages (Private) Limited

- Location.

The Subject Company’s located at the client # 400, Deans Road, Colombo 10.

- Operations

Details.

General

The subject company’s primary line of business is a Production & processing of tea & Rubber.

The subject Company comprises of 26 estates covering over 13,000

hectares in total with almost equal Extents of Tea and Rubber, spanning three

distinctive agro-climatic regions.

The subject company has earned certified by HACCP (Sri Lanka), ISO 22000: 2005 (Switzerland) accreditations

Products

Tea & Rubber

Export

Countries

Egypt, Syria, Ukraine, Russia, Middle East

No

of Employees

Approximately 13,000

- Trade

references

The subject company did not provide any trade

reference referrals

- Credit Recommendations

No computerised data bases exist to make checks

whether the partners or the company has any legal action or lawsuit initiated

against any of them but informal (but not in-depth) checks do not indicate any

such cases in the public knowledge.

Information

denied by

|

Name : |

Mr. Ajith Nissanke |

|

Designation : |

DGM Finance |

|

Contact No.: |

(009411) 2627700 |

|

Date : |

20.05.2015 |

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.63.86 |

|

|

1 |

Rs.98.89 |

|

Euro |

1 |

Rs.70.73 |

INFORMATION DETAILS

|

Analysis Done by

: |

RAS |

|

|

|

|

Report Prepared

by : |

ANK |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest capability

for timely payment of interest and principal sums |

Unlimited |

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

-- |

NB |

New Business |

-- |

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is calculated

from a composite of weighted scores obtained from each of the major sections of

this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment record

(10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.