MIRA INFORM REPORT

|

Report No. : |

342076 |

|

Report Date : |

21.09.2015 |

IDENTIFICATION DETAILS

|

Name : |

MANUFACTURAS ARTISTICAS DEL CUERO SOCIEDAD LIMITADA |

|

|

|

|

Registered Office : |

C/ Alemania, Parc.82-85 Elda (Alicante) |

|

|

|

|

Country : |

Spain |

|

|

|

|

Financials (as on) : |

31.12.2014 |

|

|

|

|

Date of Incorporation : |

01.01.1990 |

|

|

|

|

Legal Form : |

Private Company |

|

|

|

|

LINE OF BUSINESS : |

WHOLESALE OF HIDES, SKINS AND

LEATHER |

|

|

|

|

No. of Employees : |

7 (2014) |

RATING & COMMENTS

|

MIRA’s Rating : |

B |

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively

below average. |

Small |

|

Status : |

Moderate |

|

|

|

|

Payment Behaviour : |

No Complaints |

|

|

|

|

Litigation : |

Clear |

NOTES:

Any query related to this report can be made

on e-mail: infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List – March 31, 2015

|

Country Name |

Previous Rating (31.12.2014) |

Current Rating (31.03.2015) |

|

Spain |

A1 |

A1 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low |

A2 |

|

Moderate |

B1 |

|

High |

B2 |

|

Very High |

C1 |

|

Restricted |

C2 |

|

Off-credit |

D |

SPAIN - ECONOMIC OVERVIEW

After experiencing a prolonged recession in the wake of the global financial crisis that began in 2008, in 2014 Spain marked the first full year of positive economic growth in seven years, largely due to increased private consumption. At the onset of the global financial crisis Spain's GDP contracted by 3.7% in 2009, ending a 16-year growth trend, and continued contracting through most of 2013. In 2013 the government successfully shored up struggling banks - exposed to the collapse of Spain's depressed real estate and construction sectors - and in January 2014 completed an EU-funded restructuring and recapitalization program.

Until 2014, credit contraction in the private sector, fiscal austerity, and high unemployment weighed on domestic consumption and investment. The unemployment rate rose from a low of about 8% in 2007 to more than 26% in 2013, but labor reforms prompted a modest reduction to 23.7% in 2014. High unemployment strained Spain's public finances, as spending on social benefits increased while tax revenues fell. Spain’s budget deficit peaked at 11.4% of GDP in 2010, but Spain gradually reduced the deficit to just under 7% of GDP in 2013-14, slightly above the 6.5% target negotiated between Spain and the EU. Public debt has increased substantially – from 60.1% of GDP in 2010 to more than 97% in 2014.

Exports were resilient throughout the economic downturn and helped to bring Spain's current account into surplus in 2013 for the first time since 1986, where it remained in 2014. Rising labor productivity and an internal devaluation resulting from moderating labor costs and lower inflation have helped to improve foreign investor interest in the economy and positive FDI flows have been restored.

The government's efforts to implement labor, pension, health, tax, and education reforms - aimed at supporting investor sentiment - have become overshadowed by political activity in 2015 in anticipation of the national parliamentary elections in November. Spain’s 2015 budget, published in September 2014, rolls back some recently imposed taxes in advance of the elections and leaves untouched the country’s value-added tax (VAT) regime, which continues to generate significantly lower revenue than the EU average. Spain’s borrowing costs are dramatically lower since their peak in mid-2012, and despite the recent uptic in economic activity, inflation has dropped sharply, from 1.5% in 2013 to nearly flat in 2014.

|

Source

: CIA |

EXECUTIVE

SUMMARY

MANUFACTURAS ARTISTICAS DEL CUERO SOCIEDAD LIMITADA

|

Cif: |

B03433091 |

|

Registry Data: |

Register ALICANTE, Section 8, Sheet 9894 |

|

Incorporation Date: |

01/01/1990 |

|

Last Publication in BORME: |

17/12/2013 (Increase of Capital) |

|

Last Published Account Deposit: |

2014 (Submitted in July of 2015) |

|

Share Capital |

3606.00 € |

Localization: C/

ALEMANIA, PARC.82-85 ELDA (ALICANTE)

|

Telephone: |

965381639 |

|

e-Mail: |

macsl@iname.com |

|

Web: |

macsl.webjump.com |

Activity

|

NACE: |

4624 / Wholesale of hides, skins and leather |

|

Size: |

SMALL |

ACTIVITY

|

NACE: |

4624 / Wholesale of hides, skins and leather |

|

Main Activity: |

Wholesale of hides, skins and leather |

|

CNAE Source: |

ANNUAL ACCOUNTS |

|

Company size: |

Microenterprise |

Staff

|

Financial Year |

Permanent Employees |

Temporary Employees |

|

|

2014 |

7 |

0 |

|

|

2013 |

8 |

0 |

|

|

2012 |

6 |

0 |

|

|

2011 |

6 |

1 |

|

|

2010 |

5 |

0 |

|

|

2009 |

6 |

0 |

|

|

2008 |

7 |

0 |

|

|

2007 |

7 |

1 |

|

|

2006 |

8 |

1 |

|

|

2005 |

8 |

1 |

|

|

2004 |

9 |

1 |

|

|

2003 |

10 |

0 |

|

|

2002 |

11 |

0 |

|

|

2001 |

11 |

0 |

|

|

2000 |

10 |

0 |

|

Basis for scoring

|

Positive Factors |

|

|

Most relevant data

|

More than adequate capacity to meet its financial obligations. However, this capacity has a higher probability to deteriorate in the mid-long term than in higher categories. |

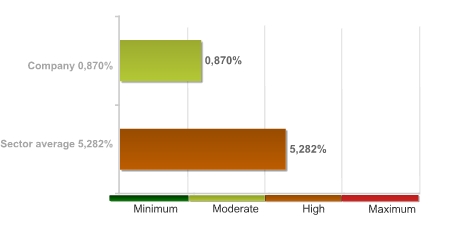

ESTIMATED

PROBABILITY OF DEFAULT

Section showing the probability that

the company queried will not be able to meet the business obligations it takes

on over the next 12 months, as well as a comparison against the average

probability within the sector.

The Estimated Probability of

Default should be interpreted as the number of companies (with similar profiles

to that of the company queried) whose loans have turned non-performing or

delinquent, as a percentage of the total number of companies..

Estimated Probability of Default

(next 12 months): 0.870 %

|

Sector in which comparison is

carried out : 462 Wholesale

of agricultural raw materials and live animals |

|

|

Relative Position:

|

Most relevant data

|

The company's comparative

analysis with the rest of the companies that comprise the sector, shows the

company holds a better position with regard to the probability of non-compliance. The 96.00% of the companies of

the sector MANUFACTURAS ARTISTICAS DEL CUERO SOCIEDAD LIMITADA belongs to

show a higher probability of non-compliance. |

|

The probability of the company's

non-compliance with its payment obligations within deadlines estimated by our

qualifications models is 0.870%. In the event they fail to comply

with the payment, the seriousness of the loss will depend on factors such as

the promptness of the commencement of the charging management, the existence

of executive documents which match the credit or the existence of guarantees

and free debt assets under the name of the debtor. Therefore, the probability

of non-compliance should not be solely interpreted as the total loss of the

owed amount. |

DEFAULTS,

LEGAL CLAIMS AND INSOLVENCY PROCEEDINGS

Section enabling assessment of the degree of compliance of the company queried with its payment obligations. It provides information on the existence and nature of all stages of Insolvency and Legal Proceedings published with reference to the Company in the country's various Official Bulletins and national newspapers, as well Defaults Registered in the main national credit bureaus (ASNEF Empresas and RAI).

Summary

|

There are no of outstanding debts with Public Administration bodies or resulting from claims filed by individuals before Courts of the different jurisdictions. |

|

No defaults are registered with the main local credit bureaus (ASNEF Empresas). |

Chronological Summary

|

Proceedings and Stages |

Number of Publications |

Amount |

Start date |

End date |

|

Insolvency Proceedings, Bankruptcy and Suspension of Payments |

Unpublished |

- |

- |

- |

|

Request/Declaration |

0 |

- |

|

- |

|

Proceedings |

0 |

- |

|

- |

|

Resolution |

0 |

- |

|

- |

|

Defaults on debt with Financial Institutions and Large Companies |

None |

- |

|

|

|

Status: Friendly |

|

- |

|

|

|

Status: Pre-Litigation |

|

- |

|

|

|

Status: Litigation |

|

- |

|

|

|

Status: Non-performing |

|

- |

|

|

|

Status: insolvency proceedings, bankruptcy and suspension of payments |

|

- |

|

|

|

Other status |

|

- |

|

|

|

Legal and Administrative Proceedings |

Unpublished |

0 |

|

|

|

Notices of defaults and enforcement |

0 |

0 |

|

|

|

Seizures |

0 |

0 |

|

|

|

Auctions |

0 |

0 |

|

|

|

Declarations of insolvency and bad debt |

0 |

0 |

|

|

|

Proceedings heard by the Civil Court |

Unpublished |

0 € |

|

|

|

Proceedings heard by the Labour Court |

Unpublished |

- |

|

|

DETAILS.

DEFAULTS WITH FINANCIAL INSTITUTIONS AND LARGE COMPANIES Bank and Commercial Delinquency

|

No defaults are registered with the main local credit bureaus (ASNEF Empresas). |

|

Product |

Number of Defaults |

|

MORTGAGE LOAN, PERSONAL LOAN |

- |

|

OVERDRAFT IN CURRENT ACCOUNT, CREDIT CARD, PRIVATE LABEL CARD OR DEBIT CARD |

- |

|

CREDIT POLICY, BUSINESS DISCOUNT |

- |

|

INSURANCE, RENTAL |

- |

|

LEASING, FACTORING, RENTING, CONFIRMING |

- |

|

TELECOMMUNICATIONS |

- |

|

AUTOMOBILE FINANCING, CAPITAL EQUIPMENT OR CONSUMER GOODS |

- |

|

COLLATERAL and GUARANTEES |

- |

|

Miscellaneous |

- |

Legal Notice:

This data has been obtained from consultation of the ASNEF Empresas register. It may only be used for the purposes of awarding credit, monitoring credit and managing loans. This data may not be reused or included in any database, and may not be ceded.

ACCOUNTS

DEPOSITED

|

Financial Year |

Type of Annual Accounts |

|

|

2014 |

Normal |

July 2015 |

|

2013 |

Normal |

September 2014 |

|

2012 |

Normal |

July 2013 |

|

2011 |

Normal |

September 2012 |

|

2010 |

Normal |

August 2011 |

|

2009 |

Normal |

November 2010 |

|

2008 |

Normal |

August 2009 |

|

2007 |

Normal |

September 2008 |

|

2006 |

Normal |

September 2007 |

|

2005 |

Normal |

August 2006 |

|

2004 |

Normal |

September 2005 |

|

2003 |

Normal |

September 2004 |

|

2002 |

Normal |

September 2003 |

|

2001 |

Normal |

August 2002 |

|

2000 |

Normal |

August 2001 |

|

1999 |

Normal |

July 2000 |

|

1998 |

Normal |

August 1999 |

|

1997 |

Normal |

July 1998 |

|

1996 |

Normal |

August 1997 |

|

1995 |

Normal |

August 1996 |

|

1994 |

Normal |

July 1995 |

|

1993 |

Normal |

August 1994 |

|

1992 |

Normal |

July 1993 |

|

1991 |

Normal |

July 1992 |

|

1990 |

Normal |

July 1991 |

|

1989 |

Normal |

July 1990 |

ABSTRACT

OF ANNUAL ACCOUNTS

Source of data:

Information corresponding to the

fiscal years designated as ORIGINAL 2008.

Information corresponding to the

fiscal years designated as EQUIVALENCE, has been calculated based on the

criteria established by the transitory provisions of the new General Accounting

Plan.

For cases where relevant

provisions do not establish equivalence criteria

Abstract of annual accounts

pursuant to new General Accounting Plan 2007

|

ASSETS |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Non-current Assets |

219.666 |

191.742 |

217.933 |

|

|

Current Assets |

609.526 |

592.589 |

610.921 |

|

|

Total Assets |

829.192 |

784.332 |

828.854 |

|

|

NET ASSETS AND LIABILITIES |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Net Worth |

492.676 |

469.453 |

464.425 |

|

|

Non-current Liabilities |

142.418 |

114.970 |

34.512 |

|

|

Current Liabilities |

194.098 |

199.909 |

329.917 |

|

|

Total Net Assets and Liabilities |

829.192 |

784.332 |

828.854 |

|

|

RESULT'S ACCOUNT |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Net total sales |

962.940 |

657.024 |

615.485 |

|

|

Other Operating Income |

2.752 |

2.338 |

1.460 |

|

|

Consumption, Amortization and Other

Operating Expenses |

-938.688 |

-651.951 |

-608.699 |

|

|

Operating Result |

27.005 |

7.411 |

8.246 |

|

|

Financial Results |

317 |

-1.223 |

-1.694 |

|

|

Discontinued Operations Result |

0 |

0 |

0 |

|

|

Financial Year Result |

23.223 |

5.028 |

5.324 |

|

ECONOMIC-FINANCIAL

RATIOS ESSENTIAL TO AWARDING CREDIT

Data used in the following ratios

and indicators is taken from the Annual Accounts submitted by the company to

the TRADE REGISTER

|

Economic-Financial

Indicators |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Net Turnover Amount |

962.940 |

657.024 |

615.485 |

|

|

Financial Year Result |

23.223 |

5.028 |

5.324 |

|

|

Average payment term |

90 |

114 |

278 |

|

|

Number of Employees |

8 |

8 |

6 |

|

|

Income Return Ratios |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Operating economic profitability |

3,25 % |

0,95 % |

0,80 % |

|

|

Total economic profitability |

3,39 % |

0,95 % |

1,02 % |

|

|

Margin |

2,79 % |

1,12 % |

1,07 % |

|

|

Solvency Ratios |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Liquidity |

0,15 |

0,05 |

0,02 |

|

|

Acid Test |

1,51 |

0,93 |

0,77 |

|

|

Working Capital / Investment |

0,50 |

0,50 |

0,34 |

|

|

Solvency |

3,14 |

2,96 |

1,85 |

|

|

Ratios de Endeudamiento |

2014 31/12/2014 |

2013 31/12/2013 |

2012 31/12/2012 |

|

|

Indebtedness level |

0,68 |

0,67 |

0,78 |

|

|

Borrowing Composition |

0,73 |

0,58 |

0,10 |

|

|

Repayment Ability |

17,80 |

86,70 |

-216,62 |

|

|

Warranty |

2,46 |

2,49 |

2,27 |

|

REGISTRY

DATA

|

Mercantile Registry: |

ALICANTE |

|

Register Data: |

8 Hoja Registral: 9894 |

|

Date of formation: |

01/01/1990 |

CHRONOLOGICAL

SUMMARY

Note:

![]() Important

Important ![]() Very Important

Very Important

|

1990 |

Accounts deposit (year 1989) Appointments/ Re-elections (2) Cessations/ Resignations/ Reversals

(1) |

|

1991 |

Accounts deposit (year 1990) |

|

1992 |

Accounts deposit (year 1991)

Appointments/ Re-elections (1) Cessations/ Resignations/

Reversals (1) |

|

1993 |

Accounts deposit (year 1992) |

|

1994 |

Accounts deposit (year 1993) |

|

1995 |

Accounts deposit (year 1994) |

|

1996 |

Accounts deposit (year 1995) |

|

1997 |

Accounts deposit (year 1996) |

|

1998 |

Accounts deposit (year 1997)

Appointments/ Re-elections (1) Cessations/ Resignations/

Reversals (1) |

|

1999 |

Accounts deposit (year 1998) |

|

2000 |

Accounts deposit (year 1999) |

|

2001 |

Accounts deposit (year 2000) |

|

2002 |

Accounts deposit (year 2001) |

|

2003 |

Accounts deposit (year 2002) |

|

2004 |

Accounts deposit (year 2003) |

|

2005 |

Accounts deposit (year 2004) |

|

2006 |

Accounts deposit (year 2005) |

|

2007 |

Accounts deposit (year 2006) Appointments/ Re-elections (2) Cessations/ Resignations/

Reversals (1) |

|

2008 |

Accounts deposit (year 2007) |

|

2009 |

Accounts deposit (year 2008) |

|

2010 |

Accounts deposit (year 2009) Appointments/ Re-elections (1) Cessations/ Resignations/

Reversals (1) |

|

2011 |

Accounts deposit (year 2010) |

|

2012 |

Accounts deposit (year 2011) |

|

2013 |

Accounts deposit (year 2012)

Cessations/ Resignations/

Reversals (1)

|

|

2014 |

Accounts deposit (year 2013) |

|

2015 |

Accounts deposit (year 2014) |

BREAKDOWN

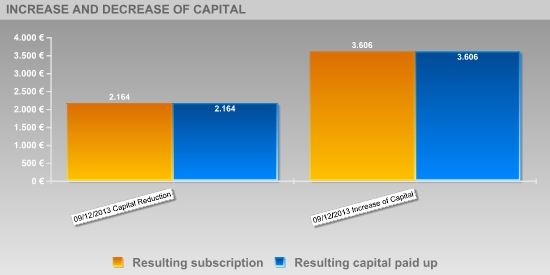

OF OWNERS EQUITY

|

Current Notarised Capital: |

3.606 EUROS |

|

Current Paid-up Capital: |

3.606 EUROS |

UPDATED EVOLUTION OF THE SUBSCRIBED AND PAID-IN CAPITAL

|

Inscription date |

Type of Registration |

Capital Subscribed |

Paid up capital |

Underwritten result |

Disbursed Result |

|

09/12/2013 |

Increase of Capital |

1.442,4€ |

1.442,4€ |

3.606€ |

3.606€ |

|

09/12/2013 |

Capital Reduction |

-1.442,4€ |

-1.442,4€ |

2.163,6€ |

2.163,6€ |

ACTIVE

SOCIAL BODIES

|

Published Post |

Social Body Name |

Registration Date |

|

SINGLE ADMINISTRATOR |

MAS ESTEVE JOAQUIN |

09/04/2010 |

|

JOINT ATTORNEY |

MAS ESTEVE JOAQUIN |

20/04/1998 |

|

PROXY |

ESTEVE ORGILES VICENTE |

29/01/1990 |

|

PROXY |

ESTEVE SANCHEZ MARIA DE LOS

ANGELES |

25/07/2007 |

|

PROXY |

MAS RAMON TOMAS |

29/01/1990 |

HISTORICAL SOCIAL BODIES

Formerly Active Governing Bodies -

Total: 5

|

Social Body's Name |

Post published |

End Date |

Other Positions in this Company |

|

FRANCISCO CAPEL SEBASTIAN |

SINGLE ADMINISTRATOR |

09/04/2010 |

2 |

|

|

JOINT ATTORNEY |

17/10/2013 |

|

|

MARIA ANGELES ESTEVE SACHEZ |

SINGLE ADMINISTRATOR |

20/04/1998 |

2 |

|

|

GENERAL MANAGER |

15/06/1992 |

|

|

MARIA ANGELES ESTEVE SANCHEZ |

SINGLE ADMINISTRATOR |

23/07/2007 |

2 |

|

MARIA CARMEN ESTEVE SANCHEZ |

JOINT ATTORNEY |

17/10/2013 |

1 |

|

VICENTE MANUEL ESTEVE SANCHEZ |

MANAGING DIRECTOR |

04/12/1990 |

1 |

SECTORS OF INTEREST THAT HAVE CONSULTED THIS ENTERPRISE

|

Sector |

2004 (3) |

2005 (6) |

2006 (3) |

2007 (3) |

2008 (9) |

2009 (2) |

2010 (6) |

2011 (4) |

2012 (1) |

2013 (16) |

2014 (4) |

2015 (7) |

|

INSURANCE AND FINANCIAL SERVICES |

|

3 |

|

3 |

6 |

|

4 |

2 |

|

4 |

2 |

4 |

|

AUDITORS, ECONOMISTS AND

CONSULTANTS |

|

|

|

|

|

|

2 |

2 |

|

6 |

2 |

2 |

|

ENERGY |

3 |

3 |

|

|

|

|

|

|

|

|

|

|

|

PUBLIC ADMINISTRATION |

|

|

|

|

2 |

2 |

|

|

|

|

|

|

|

WHOLESALERS AND MIDDLEMEN |

|

|

3 |

|

|

|

|

|

|

|

|

|

|

MISCELLANEOUS SECTORS |

|

|

|

|

|

|

|

|

|

2 |

|

1 |

|

LAWYERS |

|

|

|

|

|

|

|

|

|

2 |

|

|

|

INDIVIDUALS |

|

|

|

|

|

|

|

|

|

2 |

|

|

|

TRADE REPORTS |

|

|

|

|

1 |

|

|

|

|

|

|

|

|

MANUFACTURE, REPAIR AND RENT OF

CONSUMER GOODS |

|

|

|

|

|

|

|

|

1 |

|

|

|

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

Rs.66.93 |

|

UK Pound |

1 |

Rs.102.75 |

|

Euro |

1 |

Rs.75.13 |

INFORMATION DETAILS

|

Analysis Done by

: |

RAS |

|

|

|

|

Report Prepared

by : |

VNT |

RATING EXPLANATIONS

|

RATING |

STATUS |

PROPOSED CREDIT LINE |

|

|

|

>86 |

Aaa |

Possesses an extremely sound financial base with the strongest

capability for timely payment of interest and principal sums |

Unlimited |

|

|

71-85 |

Aa |

Possesses adequate working capital. No caution needed for credit

transaction. It has above average (strong) capability for payment of interest

and principal sums |

Large |

|

|

56-70 |

A |

Financial & operational base are regarded healthy. General

unfavourable factors will not cause fatal effect. Satisfactory capability for

payment of interest and principal sums |

Fairly Large |

|

|

41-55 |

Ba |

Overall operation is considered normal. Capable to meet normal

commitments. |

Satisfactory |

|

|

26-40 |

B |

Capability to overcome financial difficulties seems comparatively below

average. |

Small |

|

|

11-25 |

Ca |

Adverse factors are apparent. Repayment of interest and principal sums

in default or expected to be in default upon maturity |

Limited with

full security |

|

|

<10 |

C |

Absolute credit risk exists. Caution needed to be exercised |

Credit not

recommended |

|

|

-- |

NB |

New Business |

-- |

|

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is calculated

from a composite of weighted scores obtained from each of the major sections of

this report. The assessed factors and their relative weights (as indicated

through %) are as follows:

Financial

condition (40%) Ownership

background (20%) Payment record

(10%)

Credit history

(10%) Market trend (10%) Operational size

(10%)

This report is issued at your request without any

risk and responsibility on the part of MIRA INFORM PRIVATE LIMITED (MIPL)

or its officials.