|

|

|

MIRA INFORM REPORT

|

Report No. : |

507224 |

|

Report Date : |

08.05.2018 |

IDENTIFICATION DETAILS

|

Name : |

|

|

|

|

|

Registered Office : |

No.

1, 4th Land In The West Of The 3rd Industrial Park,

Xiabai, Luocun, Shishan Town, Nanhai District, Foshan, Guangdong Province,

528000 |

|

|

|

|

Country : |

China |

|

|

|

|

Date of Incorporation : |

28.07.2014 |

|

|

|

|

Credibility code: |

91440605304087918E |

|

|

|

|

Legal Form : |

Sole Proprietorship Enterprise |

|

|

|

|

Line of Business : |

Subject registered business

scope includes processing, manufacturing and selling electronics, home

appliances, plastics, computer consumables, hardware appliance and hardware

products. |

|

|

|

|

No. of Employees : |

Not Available |

RATING & COMMENTS

(Mira Inform has adopted New Rating mechanism w.e.f. 23rd

January 2017)

|

MIRA’s Rating : |

B |

|

Credit Rating |

Explanation |

Rating Comments |

|

B |

Medium Risk |

Business dealings permissible on a regular

monitoring basis |

|

Status : |

Moderate |

|

|

|

|

Payment Behaviour : |

Unknown |

|

|

|

|

Litigation : |

Clear |

NOTES :

Any query related to this report can be made

on e-mail : infodept@mirainform.com

while quoting report number, name and date.

ECGC Country Risk Classification List

|

Country Name |

Previous Rating (30.09.2017) |

Current Rating (31.12.2017) |

|

China |

A2 |

A2 |

|

Risk Category |

ECGC

Classification |

|

Insignificant |

A1 |

|

Low Risk |

A2 |

|

Moderately Low Risk |

B1 |

|

Moderate Risk |

B2 |

|

Moderately High Risk |

C1 |

|

High Risk |

C2 |

|

Very High Risk |

D |

CHINA - ECONOMIC OVERVIEW

Since the late 1970s, China has moved from a closed, centrally planned system to a more market-oriented one that plays a major global role. China has implemented reforms in a gradualist fashion, resulting in efficiency gains that have contributed to a more than tenfold increase in GDP since 1978. Reforms began with the phaseout of collectivized agriculture, and expanded to include the gradual liberalization of prices, fiscal decentralization, increased autonomy for state enterprises, growth of the private sector, development of stock markets and a modern banking system, and opening to foreign trade and investment. China continues to pursue an industrial policy, state support of key sectors, and a restrictive investment regime. Measured on a purchasing power parity (PPP) basis that adjusts for price differences, China in 2016 stood as the largest economy in the world, surpassing the US in 2014 for the first time in modern history. China became the world's largest exporter in 2010, and the largest trading nation in 2013. Still, China's per capita income is below the world average.

After keeping its currency tightly linked to the US dollar for years, China in July 2005 moved to an exchange rate system that references a basket of currencies. From mid-2005 to late 2008, the renminbi appreciated more than 20% against the US dollar, but the exchange rate remained virtually pegged to the dollar from the onset of the global financial crisis until June 2010, when Beijing announced it would allow a resumption of gradual liberalization. From 2013 until early 2015, the renminbi (RMB) appreciated roughly 2% against the dollar, but the exchange rate fell 13% from mid-2015 until end-2016 amid strong capital outflows in part stemming from the August 2015 official devaluation; in 2017 the RMB resumed appreciating against the dollar – roughly 7% from end-of-2016 to end-of-2017. From 2013 to 2017, China had one of the fastest growing economies in the world, averaging slightly more than 7% real growth per year. In 2015, the People’s Bank of China announced it would continue to carefully push for full convertibility of the renminbi, after the currency was accepted as part of the IMF’s special drawing rights basket. However, since late 2015 the Chinese Government has strengthened capital controls and oversight of overseas investments to better manage the exchange rate and maintain financial stability.

The Chinese Government faces numerous economic challenges including: (a) reducing its high domestic savings rate and correspondingly low domestic household consumption; (b) managing its high corporate debt burden to maintain financial stability; (c) controlling off-balance sheet local government debt used to finance infrastructure stimulus; (d) facilitating higher-wage job opportunities for the aspiring middle class, including rural migrants and college graduates, while maintaining competitiveness; (e) dampening speculative investment in the real estate sector without sharply slowing the economy; (f) reducing industrial overcapacity; and (g) raising productivity growth rates through the more efficient allocation of capital and state-support for innovation. Economic development has progressed further in coastal provinces than in the interior, and by 2016 more than 169.3 million migrant workers and their dependents had relocated to urban areas to find work. One consequence of China’s population control policy known as the “one-child policy” - which was relaxed in 2016 to permit all families to have two children - is that China is now one of the most rapidly aging countries in the world. Deterioration in the environment - notably air pollution, soil erosion, and the steady fall of the water table, especially in the North - is another long-term problem. China continues to lose arable land because of erosion and urbanization. The Chinese Government is seeking to add energy production capacity from sources other than coal and oil, focusing on natural gas, nuclear, and clean energy development. In 2016, China ratified the Paris Agreement, a multilateral agreement to combat climate change, and committed to peak its carbon dioxide emissions between 2025 and 2030.

The government's 13th Five-Year Plan, unveiled in March 2016, emphasizes the need to increase innovation and boost domestic consumption to make the economy less dependent on government investment, exports, and heavy industry. However, China has made more progress on subsidizing innovation than rebalancing the economy. Beijing has committed to giving the market a more decisive role in allocating resources, but the Chinese Government’s policies continue to favor state-owned enterprises and emphasize stability. Chinese leaders in 2010 pledged to double China’s GDP by 2020, and the 13th Five Year Plan includes annual economic growth targets of at least 6.5% through 2020 to achieve that goal. In recent years, China has renewed its support for state-owned enterprises in sectors considered important to "economic security," explicitly looking to foster globally competitive industries. Chinese leaders also have undermined some market-oriented reforms by reaffirming the “dominant” role of the state in the economy, a stance that threatens to discourage private initiative and make the economy less efficient over time. The slight acceleration in economic growth in 2017—the first such uptick since 2010—gives Beijing more latitude to pursue its economic reforms, focusing on financial sector deleveraging and its Supply-Side Structural Reform agenda, first announced in late 2015.

|

Source

: CIA |

Company

name and address

FOSHAN RAYSWA ELECTRONICS FACTORY

No. 1,

4th Land in The West of The 3rd Industrial Park, XiaBAI,

Luocun,

Shishan Town, Nanhai District, FOSHAN,

GUANGDONG

PROVINCE, 528000 PR CHINA

TEL: 86

(0) 757-82282676 FAX: N/A

EXECUTIVE

SUMMARY

INCORPORATION DATE : jULY 28, 2014

CREDIBILITY CODE : 91440605304087918E

REGISTERED LEGAL FORM :

sole proprietorship enterprise

STAFF STRENGTH : N/A

REGISTERED CAPITAL : CNY 500,000

BUSINESS LINE : PROCESSING and trading

TURNOVER : n/a

EQUITIES : n/a

PAYMENT : UNKNOWN

MARKET CONDITION : AVERAGE

FINANCIAL CONDITION : n/a

OPERATIONAL TREND : FAIRLY STEADY

GENERAL REPUTATION : AVERAGE

Adopted

abbreviations:

ANS -

amount not stated NS - not stated SC - subject company (the company inquired

by you)

NA - not available CNY - China Yuan Renminbi

![]()

SC was registered as a Sole Proprietorship enterprise at

local Administration for Industry & Commerce (AIC - The official body of

issuing and renewing business license) on July 28, 2014.

Company Status: Sole Proprietorship enterprise This form of business in PR

China is a private enterprise formed by an individual, which does not have

the legal person or limited liability status. The co. is solely operated by

the sole investor who is responsible for all risks & liabilities of the

co.

SC’s

registered business scope includes processing, manufacturing and selling

electronics, home appliances, plastics, computer consumables, hardware

appliance and hardware products.

SC is

mainly engaged in processing and selling Bluetooth headset.

Li

Xiaohua is the principal of SC at

present.

SC’s

management declined to disclose its staff strength.

SC is currently operating at the above stated address, and this

address houses its operating office and factory in Foshan. The detailed premise

information is unspecific.

![]()

http://www.rayswa.cn/

The design is professional and the content is well organized. At present it is

in English version.

E-mail: alice@rayswa.cn

![]()

No significant events or changes were found during our

checks with local AIC.

![]()

For the past two years there is no record of litigation.

![]()

MAIN SHAREHOLDER:

Name %

of Shareholding

Li Xiaohua 100

![]()

l Principal:

Li Xiaohua is currently responsible for the overall

management of SC.

Working Experience(s):

At present Working in SC as principal.

![]()

SC is

mainly engaged in processing and selling Bluetooth headset.

SC’s products mainly include: ear headset, headphones, sport

earphone, etc.

Trademarks & patents

No record

SC sources its materials from both domestic market and

overseas market. SC sells its products in overseas market.

The buying terms of SC include Check, T/T, L/C and Credit of

30-60 days. The payment terms of SC include Check, T/T, L/C and Credit of 30-60

days.

Note: SC refused to release its major suppliers and clients.

Industry code: 3952

Industry name: Electronic audio manufacturing

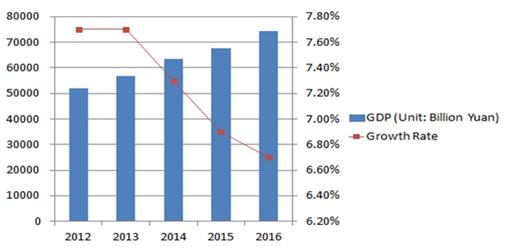

The gross domestic product of

China in 2016 which is 74412.72 billion that is increased 6.7% than previous

year.

Chinese electronic audio

industry development, the white paper" (2016) data show that in 2015 China

electronic audio industry remain stable growth, and total outputs are 280.83 billion

Yuan in 2015, which is increased 1.2% than previous year. Total amount of

export is $30.11 billion in 2015, which is raised 0.9% than previous year.

Total import amount is $6.01 billion in 2015 that is decreased 11.7% than

previous year.

![]()

SC is not known to have any subsidiary at present.

![]()

Overall payment appraisal:

( ) Excellent (

) Good (X) Average (

) Fair ( ) Poor

( ) Not yet determined

The appraisal serves as a reference to reveal SC's payments

habits and ability to pay. It is based

on the 3 weighed factors: Trade payment

experience (through current enquiry with SC's suppliers), our delinquent

payment records and our debt collection record concerning SC.

Trade payment experience: SC did not provide any name of

trade/service suppliers and we have no other sources to conduct the enquiry at

present.

Delinquent payment record: None

in our database.

Debt collection record: No overdue amount owed by SC was

placed to us for collection within the last 6 years.

![]()

SC

declined to release its banking details.

![]()

As a

sole proprietorship enterprise, there is no legal requirement according to

local corporate law for public disclosure of detailed financials.

![]()

SC was established in 2014, taking into consideration of SC’s

general performance, reputation as well as market conditions we would rate SC

as an above average credit risk company. Due to lack of financial status, we

are unable to recommend accurate credit limit for SC.

FOREIGN EXCHANGE RATES

|

Currency |

Unit

|

Indian Rupees |

|

US Dollar |

1 |

INR 66.77 |

|

|

1 |

INR 90.58 |

|

Euro |

1 |

INR 79.97 |

|

CNY |

1 |

INR 10.53 |

Note :

Above are approximate rates obtained from sources believed to be correct

INFORMATION DETAILS

|

Analysis Done by

: |

DIV |

|

|

|

|

Report Prepared

by : |

KET |

RATING EXPLANATIONS

|

Credit Rating |

Explanation |

Rating Comments |

|

A++ |

Minimum Risk |

Business dealings permissible with minimum

risk of default |

|

A+ |

Low Risk |

Business dealings permissible with low

risk of default |

|

A |

Acceptable Risk |

Business dealings permissible with

moderate risk of default |

|

B |

Medium Risk |

Business dealings permissible on a regular

monitoring basis |

|

C |

Medium High Risk |

Business dealings permissible preferably

on secured basis |

|

D |

High Risk |

Business dealing not recommended or on

secured terms only |

|

NB |

New Business |

No recommendation can be done due to

business in infancy stage |

|

NT |

No Trace |

No recommendation can be done as the

business is not traceable |

NB is stated where there is insufficient information to facilitate rating. However, it is not to be considered as unfavourable.

This score serves as a reference to assess

SC’s credit risk and to set the amount of credit to be extended. It is

calculated from a composite of weighted scores obtained from each of the major

sections of this report. The assessed factors are as follows:

·

Financial

condition covering various ratios

·

Company

background and operations size

·

Promoters

/ Management background

·

Payment

record

·

Litigation

against the subject

·

Industry

scenario / competitor analysis

·

Supplier

/ Customer / Banker review (wherever available)

This report is issued at

your request without any risk and responsibility on the part of MIRA INFORM

PRIVATE LIMITED (MIPL) or its officials.